Trade Details:

4 May RUT 1400/1390 Credit Put spread @0.60 credit each

2 May RUT 1650/1660 Credit Call spread @1.10 credit each

3 May IWM 166 Long Calls @0.24 debit each

Net Credit: $388

Max Risk: $3,612

Risk Profile

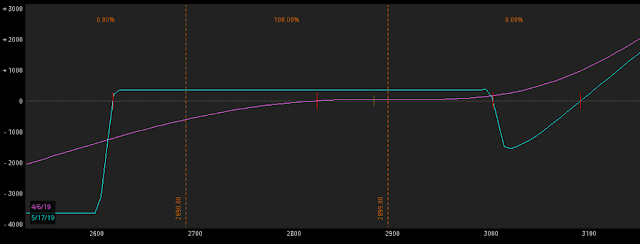

RUT Chart for future reference:

Trade Update - April 9, 2019

Added one more IWM May 166 Call to flatten the T+0 line to the upside a bit more.

Debit invested 0.28

Now four IWM 166 Calls in total, $100 total debit paid for them. Avg Call option price is therefore 0.25

Trade Update - April 23, 2019

Closed the whole position:

4 May RUT 1400/1390 Credit Put spread @0.10 debit each

Original Credit: 0.60

Net Profit: 0.50 ($0.50 * 100 * 4 = $200)

2 May RUT 1650/1660 Credit Call spread @0.50 debit each

Original Credit: 1.10

Net Profit: 0.60 ($0.60 * 100 * 2 = $120)

4 May IWM 166 Long Calls @0.08 credit each

Original Debit: 0.25

Net loss: 0.17 ($0.17 * 4 * 100 = $68)

The total net result is +200 + 120 - 68 = $252

On a Max Risk of $3,612 this is a +7.0% Return on Risk.

We are out of the position 24 days before expiration, in order to redeploy this capital in the June cycle.

4 May RUT 1400/1390 Credit Put spread @0.60 credit each

2 May RUT 1650/1660 Credit Call spread @1.10 credit each

3 May IWM 166 Long Calls @0.24 debit each

Net Credit: $388

Max Risk: $3,612

Risk Profile

RUT Chart for future reference:

Trade Update - April 9, 2019

Added one more IWM May 166 Call to flatten the T+0 line to the upside a bit more.

Debit invested 0.28

Now four IWM 166 Calls in total, $100 total debit paid for them. Avg Call option price is therefore 0.25

Trade Update - April 23, 2019

Closed the whole position:

4 May RUT 1400/1390 Credit Put spread @0.10 debit each

Original Credit: 0.60

Net Profit: 0.50 ($0.50 * 100 * 4 = $200)

2 May RUT 1650/1660 Credit Call spread @0.50 debit each

Original Credit: 1.10

Net Profit: 0.60 ($0.60 * 100 * 2 = $120)

4 May IWM 166 Long Calls @0.08 credit each

Original Debit: 0.25

Net loss: 0.17 ($0.17 * 4 * 100 = $68)

The total net result is +200 + 120 - 68 = $252

On a Max Risk of $3,612 this is a +7.0% Return on Risk.

We are out of the position 24 days before expiration, in order to redeploy this capital in the June cycle.

Go to the bottom of this page in order to see the Legal Stuff

No comments:

Post a Comment