Recent Trading Activity

- Closed 2745/2450 Call side of January SPX Unbalanced Iron Condor at a $1920 loss on Friday. Immediately deployed a 2785/2790 Credit Call spread for a $480 credit. I'm a little frustrated. Losses are part of the game, but basically this position should have been closed two weeks ago simply due to risk concentration around SPX 2740 along with the February position. It's a rule. I never thought these levels would be tested. I became overconfident and didn't follow the basic tenet of the system that urges to avoid concentration of risk on the spectrum of prices of the index. Iron Condors were my best performing strategy in 2017. No need to abandon them. The rule is in place, the situation could have been avoided. I chose to ignore it, taking more risk, expecting greater returns.

- Initiated the February RUT Elephant position on Friday for a total credit of $1,456.

- Closed 2745/2450 Call side of January SPX Unbalanced Iron Condor at a $1920 loss on Friday. Immediately deployed a 2785/2790 Credit Call spread for a $480 credit. I'm a little frustrated. Losses are part of the game, but basically this position should have been closed two weeks ago simply due to risk concentration around SPX 2740 along with the February position. It's a rule. I never thought these levels would be tested. I became overconfident and didn't follow the basic tenet of the system that urges to avoid concentration of risk on the spectrum of prices of the index. Iron Condors were my best performing strategy in 2017. No need to abandon them. The rule is in place, the situation could have been avoided. I chose to ignore it, taking more risk, expecting greater returns.

- Initiated the February RUT Elephant position on Friday for a total credit of $1,456.

Market Conditions

(Click on image to enlarge)

McClellan: +80 (Neutral. Up from +21 last week)

Stocks above their 20 DMA: 68% (Neutral. Up from 53% last week)

No man's land.

It's amazing that after this incredible rally, two of the oscillators are yet to reach overbought territory. Especially McClellan, so far from it.

Breadth indicators are a funny thing to interpret. On the one hand some argue that when they are too high, there is broad participation from all the stocks and sectors and therefore there is "strength" in the move "supported by breadth". Interpreted as healthy for the rally and forecasting continuation. However, when most stocks have already joined the party, not many more can join to keep fueling the rally and therefore the "end" gets closer. So, two opposing views.

Then there is the case of a rally not accompanied by the corresponding spike in breadth indicators. The first group says "Oh, it's a weak rally, not supported by broad participation" (forecasting that it shouldn't last too long). However, on the other hand one could argue "well, if there is a rally that is happening without broad participation, imagine how much strength it will gather if all the other stocks join the party!".

Because I sell Credit Spreads, I tend to adopt the fatalistic view, which represents the worst case scenarios for my positions. In the present rally the SPX is 4.3% higher than its 50-day average, true. Yet, incredibly, the market is not in an overbought stage according to our definition. My thinking is automatically: "There is more upside room, I need to be careful". Granted, the breadth indicators are signaling that there is still some little room left, but at 4.3% higher than its 50-day average the index is very close to a temporary overbought extreme that must be alleviated, at least via some sideways action for a few days.

Bull markets die hard and shorting Euphoria tends to truly payoff only once or twice per decade. Too many lunatics out there right now. The loss suffered this week surely hurts, but there is an entire year ahead to recover. We've been through this before. To combat these rallies and take advantage of the historical upside bias of the American market, it is not a bad idea to keep a small part of the capital of the portfolio permanently invested in UPRO (triple leveraged SPX) or ZIV (short mid-term volatility). That way, when you suffer losses on the Call side (the most frequently tested one) they are constantly neutralized by this part of the portfolio that would otherwise be in cash producing nothing.

The Russell:

(Click on image to enlarge)

Current Portfolio

Jan. SPX 2440/2450/2785/2790 Unbalanced Iron Condor

with additional 2480/2475 Credit Put spreads

Net credit: $2,080. Two weeks to expiration.

(Click on image to enlarge)

Defense lines: 2,505 (adjust 2450/2440 Put spread). Then comes 2,485 (adjust the small 2480/2475 Put spread). On the upside I'll wait until 2,780 to adjust the Call side.

Defense lines: 2,505 (adjust 2450/2440 Put spread). Then comes 2,485 (adjust the small 2480/2475 Put spread). On the upside I'll wait until 2,780 to adjust the Call side.

Jan. RUT/IWM 1380/1390/1605/1610/161 Unbalanced Elephant

Net credit: $1,448. Two weeks to expiration.

(Click on image to enlarge)

Defense lines: 1,420 (adjust Put side) and 1,585 (close the Call side at a small loss, keep riding the Put side, whose gains will more than cover the hypothetical Calls' losses).

Defense lines: 1,420 (adjust Put side) and 1,585 (close the Call side at a small loss, keep riding the Put side, whose gains will more than cover the hypothetical Calls' losses).

Feb. SPX 2520/2525/2780/2785 Unbalanced Iron Condor

Net credit: $1,900. Seven weeks to expiration.

(Click on image to enlarge)

Defense

lines: 2,590 (adjust 2525/2520 Put spread) and 2,743 - time adjust

the 2780/2785 Call side. At this point the Credit Call spread is at 31 deltas and 29% probability of expiring in the money. So, it's the time to adjust it. Details in the action plan for the week.

Defense

lines: 2,590 (adjust 2525/2520 Put spread) and 2,743 - time adjust

the 2780/2785 Call side. At this point the Credit Call spread is at 31 deltas and 29% probability of expiring in the money. So, it's the time to adjust it. Details in the action plan for the week.

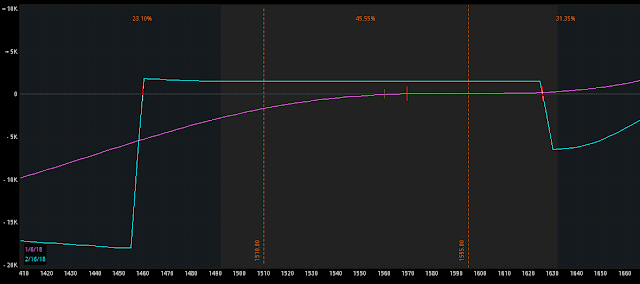

RUT/IWM - 1455/1460/1625/1630 - 147/163 Elephant

Net Credit: $1,456. Six weeks to expiration.

(Click on image to enlarge)

Defense lines: 1,510 (adjust Put side) and 1,585 (close the Call side at

a small loss, keep riding the Put side, whose gains will more than

cover the hypothetical Calls' losses).

Defense lines: 1,510 (adjust Put side) and 1,585 (close the Call side at

a small loss, keep riding the Put side, whose gains will more than

cover the hypothetical Calls' losses).

Well, now the concentration of risk is on RUT 1585; a point where both Elephants would be taking a loss on the Call side. An Elephant taking a loss on the Call side is not a big deal (it ends up as a net winner thanks to the Put side. But a smaller winner). However, two of them getting hurt on the Call side and both becoming smaller winners because of it, is no joke. So, I'll make it a priority to close the Call side of one them this upcoming week.

Jan. SPX 2440/2450/2785/2790 Unbalanced Iron Condor

with additional 2480/2475 Credit Put spreads

Net credit: $2,080. Two weeks to expiration.

(Click on image to enlarge)

Jan. RUT/IWM 1380/1390/1605/1610/161 Unbalanced Elephant

Net credit: $1,448. Two weeks to expiration.

(Click on image to enlarge)

Feb. SPX 2520/2525/2780/2785 Unbalanced Iron Condor

Net credit: $1,900. Seven weeks to expiration.

(Click on image to enlarge)

RUT/IWM - 1455/1460/1625/1630 - 147/163 Elephant

Net Credit: $1,456. Six weeks to expiration.

(Click on image to enlarge)

Well, now the concentration of risk is on RUT 1585; a point where both Elephants would be taking a loss on the Call side. An Elephant taking a loss on the Call side is not a big deal (it ends up as a net winner thanks to the Put side. But a smaller winner). However, two of them getting hurt on the Call side and both becoming smaller winners because of it, is no joke. So, I'll make it a priority to close the Call side of one them this upcoming week.

Action Plan for the Week

Defense mode.

- For the 2785/2790 Call side of the SPX January Iron Condor. I'll adjust if SPX reaches 2780. The adjustment will be done using March options around the 2900 strike prices. I'll increase the number of contracts if this happens.

- I'll close the Call side of the RUT January Elephant on Monday. This will eliminate risk concentration around RUT 1,585. This should be a tiny gain or break-even if nothing crazy takes place during pre-market action.

- In the case of the SPX February Iron Condor, I'll take a loss on the 2780/2785 Credit Call spread on Monday as it reached 30 deltas and it is a 2:1 ratio position. I will deploy a new Credit Call spread around 2825 (same Feb option expiration). Additionally, I'll sell a small credit Put spread position around 2,610 (about a quarter the size of the existing Put spread in terms of capital at risk). This extra credit will come in handy and given that it is a very small position, it is one of those that I don't adjust until price gets super close to it; instead of the 30 delta rule. If after doing this, the new Call spread around 2825 reaches 20 deltas, I'll be buying Long SPY Calls as an upside hedge sacrificing part of the profitability of that Credit Call spread.

Two valuable lessons this week:

. Always eliminate risk concentration. Always without letting bias cloud your judgement.

. Once again, be very conservative on the Call side. I will rarely trade 2:1 ratio Iron Condors anymore and will be more focused on 4:1s.

Economic Calendar

Wednesday: ECB Meeting. US PPI and Federal Budget Balance.

Friday: CPI and Retail Sales.

Trade with confidence my friends.

LT

If you are interested in a responsible and sustainable way of trading options for consistent income with solid risk management, consider acquiring LTOptions, my options trading system to the last detail.

Check out 2018 Track Record

Go to the bottom of this page in order to see the Legal Stuff

No comments:

Post a Comment