Important Note: Some modifications have been made to the 2018 Options Trading Plan. The changes are focused on efficiency and simplicity when defending Credit Call spreads. Log in to LTOptions.com and consult the 2018 Options Trading Plan ebook.

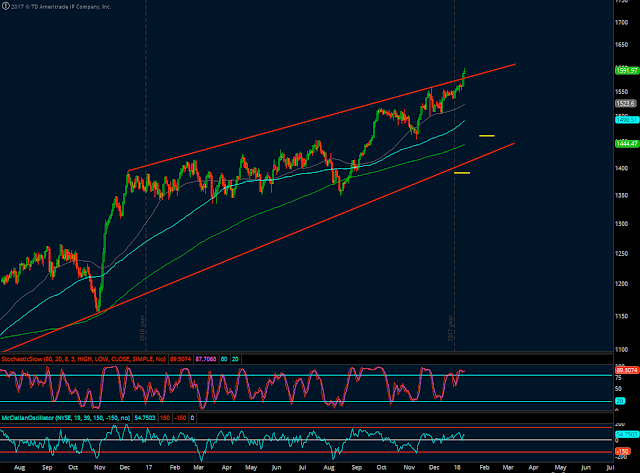

Market Conditions

(Click on image to enlarge)

Stochastics: 95 (Overbough. Same as last week)

Stochastics: 95 (Overbough. Same as last week)

McClellan: +54 (Neutral. Down from +80 last week)

Stocks above their 20 DMA: 74% (Overbought. Up from 68% last week)

Still No man's land!

The index is 5.2% higher than its 50-day average. Ever since I started trading, I had never seen a number like this one on the SPX. +3.5% used to be extreme and perhaps once, I saw the index 4% higher than its 50-day average. But that was it. This is extreme price action and a reminder that anything can happen at any time. The market is up 4.2% for the year in just two weeks. At this pace it will be up more than 200% by the end of the year. Clearly this price action is not sustainable.

There is no question about the over valuation of the American markets. Currently a PE Ratio of 26 for the S&P500 and forward PE Ratio of 19. Based on historical norms, the market looks overvalued by 15%-20%, which is something. There is however too much euphoria at the moment to even think a correction is imminent. Bull markets die hard.

In the 2018 trading plan I mentioned the idea of using a cash portion of a portfolio for buying ZIV shares. This would act as a hedge against low volatility rallies that affect our Iron Condors on the Call side. I did this myself in my own account, but I will keep that part out of the track record since I never officially announced that position. ZIV shares are up 5.89% for the year. Another extra weapon would be a small leveraged portfolio as the one I started implementing this year, made up of Triple leveraged SPY (UPRO 30% holdings) + ZIV (30%) + TMF (40%) Triple leveraged bonds. These are good alternatives to make some serious money in low volatility and euphoric markets. There's no need to be a one trick pony hero.

The losses suffered this week sure hurt. They always do. But it is good to remember that no single strategy can perform well indefinitely. So, it is a good idea to have several of them at your disposal.

Being simply long SPY has been great in recent years. That can't be denied. At the same time however, I vividly remember back in the day when I started to actively trade, the hordes of frustrated investors showing no returns for an entire decade (read The Lost decade from Investopedia). Back then there was a decent number of people killing it with credit spreads. So, some strategies will fall out of favor from time to time. Some will come back. It's just the nature of the business. The portfolio is in a draw-down, but if anything, that forces me to be more disciplined and focused now. We'll get out of the hole.

The Russell:

(Click on image to enlarge)

RUT also shooting up past long-term resistance. No concerns here though as there is no more upside exposure and all we have is the Put side of what originally used to be Elephants.

RUT also shooting up past long-term resistance. No concerns here though as there is no more upside exposure and all we have is the Put side of what originally used to be Elephants.

Action Plan for the Week

- Let the Jan SPX Credit Put spreads expire for max.

- Let the Jan RUT Credit Put spreads expire for max.

- I'll be looking at SPX prices and the Feb 2825/2830 Credit Call spreads. Anything between 2,815 and 2,820 will make me close at a loss. I'd also be closing the SPY Long 282 Calls for gains and deploying a new Credit Call spread in April expiration around SPX 2,960.

- Finally, I'll enter the first position of the March expiration cycle on Friday. It will be an Unbalanced Iron Condor (4:1). SPX is usually my go to instrument. However, there is now a March SPX Credit Call spread, and we also need to consider a chance for an April SPX Credit Call spread as the defensive move explained in the previous item. Adding more call exposure in SPX is not wise, even if it is on a 4:1 position. On the RUT index however, there is no Call exposure. So, I will go with RUT this time around. My candidate: 1440/1450 on the PUT side and 1690/1700 on the Call side. Again, a 4:1 ratio of Puts to Calls. These strike prices may change from here until Friday, depending on how far market moves one way or the other.

Economic Calendar

Monday: Market closed (Martin Luther King Jr. Day)

Wednesday: Europe CPI. China's GDP and Industrial Production.

Thursday: US Building Permits. Philly Fed Index.

Friday: Michigan Consumer Sentiment and Expectations.

Good luck this week my friends.

LT

If you are interested in a responsible and sustainable way of trading options for consistent income with solid risk management, consider acquiring LTOptions, my options trading system to the last detail.

Check out 2018 Track Record

Recent Trading Activity

- Closed Jan. RUT Elephant Call side for a small $103 gain on Monday. This was, as planned, to reduced risk concentration on Call side of Elephants. It was the right decision.

- Closed 2780/2785 Call side of Feb. SPX Iron Condor at $2,300 loss on Monday. Deployed 2825/2830 Call spread ($900 credit), 2625/2620 Put spread ($300 credit). Later in the week (Friday), added SPY Long Calls, strike price 282.

- Closed Call side of Feb. RUT Elephant on Thursday at a $632 loss. The Put side is still in play and it is almost a sure winner by now. With its net $1,060 credit it can turn the Elephant into a winner.

- Closed Jan. SPX 2785/2790 Credit Call spread on Friday at a $1,620 loss. Immediately deployed a March 2900/2905 Credit Call spread right after for $600 credit to eventually mitigate the loss. With this adjustment, the January Iron Condor has been defended three times. This is extreme. Never in the past have I needed to adjust four times. The defense game on the Call side is a challenging one and at times a really frustrating one. Consequently, I have modified the 2018 Trading Plan with new go to moves when the Call side of our Iron Condors is threatened. I think we will be better off in the long run with these changes. Check them out over at LTOptions.com.

- Closed Jan. RUT Elephant Call side for a small $103 gain on Monday. This was, as planned, to reduced risk concentration on Call side of Elephants. It was the right decision.

- Closed 2780/2785 Call side of Feb. SPX Iron Condor at $2,300 loss on Monday. Deployed 2825/2830 Call spread ($900 credit), 2625/2620 Put spread ($300 credit). Later in the week (Friday), added SPY Long Calls, strike price 282.

- Closed Call side of Feb. RUT Elephant on Thursday at a $632 loss. The Put side is still in play and it is almost a sure winner by now. With its net $1,060 credit it can turn the Elephant into a winner.

- Closed Jan. SPX 2785/2790 Credit Call spread on Friday at a $1,620 loss. Immediately deployed a March 2900/2905 Credit Call spread right after for $600 credit to eventually mitigate the loss. With this adjustment, the January Iron Condor has been defended three times. This is extreme. Never in the past have I needed to adjust four times. The defense game on the Call side is a challenging one and at times a really frustrating one. Consequently, I have modified the 2018 Trading Plan with new go to moves when the Call side of our Iron Condors is threatened. I think we will be better off in the long run with these changes. Check them out over at LTOptions.com.

Market Conditions

(Click on image to enlarge)

McClellan: +54 (Neutral. Down from +80 last week)

Stocks above their 20 DMA: 74% (Overbought. Up from 68% last week)

Still No man's land!

The index is 5.2% higher than its 50-day average. Ever since I started trading, I had never seen a number like this one on the SPX. +3.5% used to be extreme and perhaps once, I saw the index 4% higher than its 50-day average. But that was it. This is extreme price action and a reminder that anything can happen at any time. The market is up 4.2% for the year in just two weeks. At this pace it will be up more than 200% by the end of the year. Clearly this price action is not sustainable.

There is no question about the over valuation of the American markets. Currently a PE Ratio of 26 for the S&P500 and forward PE Ratio of 19. Based on historical norms, the market looks overvalued by 15%-20%, which is something. There is however too much euphoria at the moment to even think a correction is imminent. Bull markets die hard.

In the 2018 trading plan I mentioned the idea of using a cash portion of a portfolio for buying ZIV shares. This would act as a hedge against low volatility rallies that affect our Iron Condors on the Call side. I did this myself in my own account, but I will keep that part out of the track record since I never officially announced that position. ZIV shares are up 5.89% for the year. Another extra weapon would be a small leveraged portfolio as the one I started implementing this year, made up of Triple leveraged SPY (UPRO 30% holdings) + ZIV (30%) + TMF (40%) Triple leveraged bonds. These are good alternatives to make some serious money in low volatility and euphoric markets. There's no need to be a one trick pony hero.

The losses suffered this week sure hurt. They always do. But it is good to remember that no single strategy can perform well indefinitely. So, it is a good idea to have several of them at your disposal.

Being simply long SPY has been great in recent years. That can't be denied. At the same time however, I vividly remember back in the day when I started to actively trade, the hordes of frustrated investors showing no returns for an entire decade (read The Lost decade from Investopedia). Back then there was a decent number of people killing it with credit spreads. So, some strategies will fall out of favor from time to time. Some will come back. It's just the nature of the business. The portfolio is in a draw-down, but if anything, that forces me to be more disciplined and focused now. We'll get out of the hole.

The Russell:

(Click on image to enlarge)

Current Portfolio

Jan. SPX 2440/2450 Credit Put spread

combined with additional 2480/2475 Credit Put spread

Net credit: $1,600. Should expire for max this Friday.

(Click on image to enlarge)

Defense line: 2,485 which looks like a very remote possibility.

Defense line: 2,485 which looks like a very remote possibility.

Jan. RUT/IWM 1380/1390 Elephant Put side

Net credit: $1,100. Should expire without hassle on Friday.

(Click on image to enlarge)

Defense lines: 1,400 which also looks like a very remote possibility.

Defense lines: 1,400 which also looks like a very remote possibility.

Feb. SPX 2520/2525/2825/2830 Unbalanced Iron Condor

with additional 2625/2630 Credit Put spread plus Long SPY 282 Calls.

Net credit: $1,200. Five weeks to expiration.

(Click on image to enlarge)

Defense

lines: 2,630 (adjust the small 2625/2620 Credit Put spread. 2,595 (adjust 2525/2520 Put spread) and 2,820 time adjust

the 2825/2830 Call side while booking gains from the SPY 282 Long Call contracts.

Defense

lines: 2,630 (adjust the small 2625/2620 Credit Put spread. 2,595 (adjust 2525/2520 Put spread) and 2,820 time adjust

the 2825/2830 Call side while booking gains from the SPY 282 Long Call contracts.

Feb. RUT/IWM - 1455/1460 - 147 Elephant Put side

Net Credit: $1,456. Six weeks to expiration.

(Click on image to enlarge)

Defense lines: 1,500 (adjust Put side).

Defense lines: 1,500 (adjust Put side).

Mar. SPX 2900/2905 Credit Call spread

Net Credit: $600

(Click on image to enlarge)

This is the adjustment to the January Unbalanced Iron Condor. I went really far out with this one and intend to ride it for a while. No concerns for now. Defense line at 2,895.

This is the adjustment to the January Unbalanced Iron Condor. I went really far out with this one and intend to ride it for a while. No concerns for now. Defense line at 2,895.

Jan. SPX 2440/2450 Credit Put spread

combined with additional 2480/2475 Credit Put spread

Net credit: $1,600. Should expire for max this Friday.

(Click on image to enlarge)

Jan. RUT/IWM 1380/1390 Elephant Put side

Net credit: $1,100. Should expire without hassle on Friday.

(Click on image to enlarge)

Feb. SPX 2520/2525/2825/2830 Unbalanced Iron Condor

with additional 2625/2630 Credit Put spread plus Long SPY 282 Calls.

Net credit: $1,200. Five weeks to expiration.

(Click on image to enlarge)

Feb. RUT/IWM - 1455/1460 - 147 Elephant Put side

Net Credit: $1,456. Six weeks to expiration.

(Click on image to enlarge)

Mar. SPX 2900/2905 Credit Call spread

Net Credit: $600

(Click on image to enlarge)

Action Plan for the Week

- Let the Jan SPX Credit Put spreads expire for max.

- Let the Jan RUT Credit Put spreads expire for max.

- I'll be looking at SPX prices and the Feb 2825/2830 Credit Call spreads. Anything between 2,815 and 2,820 will make me close at a loss. I'd also be closing the SPY Long 282 Calls for gains and deploying a new Credit Call spread in April expiration around SPX 2,960.

- Finally, I'll enter the first position of the March expiration cycle on Friday. It will be an Unbalanced Iron Condor (4:1). SPX is usually my go to instrument. However, there is now a March SPX Credit Call spread, and we also need to consider a chance for an April SPX Credit Call spread as the defensive move explained in the previous item. Adding more call exposure in SPX is not wise, even if it is on a 4:1 position. On the RUT index however, there is no Call exposure. So, I will go with RUT this time around. My candidate: 1440/1450 on the PUT side and 1690/1700 on the Call side. Again, a 4:1 ratio of Puts to Calls. These strike prices may change from here until Friday, depending on how far market moves one way or the other.

Economic Calendar

Monday: Market closed (Martin Luther King Jr. Day)

Wednesday: Europe CPI. China's GDP and Industrial Production.

Thursday: US Building Permits. Philly Fed Index.

Friday: Michigan Consumer Sentiment and Expectations.

Good luck this week my friends.

LT

If you are interested in a responsible and sustainable way of trading options for consistent income with solid risk management, consider acquiring LTOptions, my options trading system to the last detail.

Check out 2018 Track Record

Go to the bottom of this page in order to see the Legal Stuff

No comments:

Post a Comment