As tweeted before market close today, I rolled up the SPX 1520/1525 February Call Credit Spread. The position had been initially entered back in January 4.

BUY TO CLOSE 5 February 1520 CALL @ 5.30 (Initially sold for 3.75)

SELL TO CLOSE 5 February 1525 CALL @4.00 (Initially bought for 3.10)

A 1.30 debit to close this position. As it had initially been opened for 0.65 credit, the balance here is a 0.65 debit loss. In 5 contracts per leg, that's a $325 loss.

Many Credit Spread sellers don't report a loss like this one. As I am rolling up the position, they consider all the trade adjustments as one single trade whose final balance is reported at the end, when the new position is liquidated. At that point they report the overall balance between the initial credit spread that loss money and the result of the rolled up one. I personally prefer to reflect it right on the spot. Thus avoiding confusion, rather than reporting a whole conglomerate of trades at the end. But in the end is the same thing.

I rolled up 10 points on SPX as follows:

SELL 5 February 1530 CALL @2.85

BUY 5 February 1535CALL @2.15

Credit: $0.70 (0.70 * 100 * 5 = $350)

Margin: $4.30 (4.30 * 100 * 5 = $2150)

Break-even point: 1529.30 (Around 1502 when I entered the trade)

Probability of success: 72.92%

Days to expiration: 20

Max return on margin: 16.28%

Commissions: $15.00 (Assuming a very unfavorable $1.50 per contract)

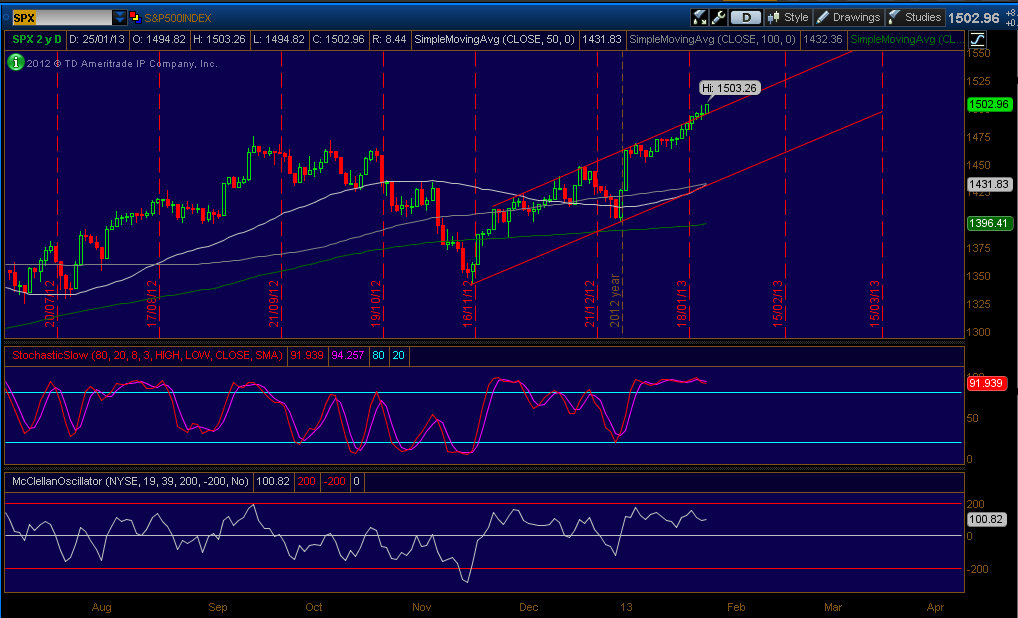

A chart of the SPX at market close on Friday, January 25, 2013 for future reference.

(Click on image to enlarge)

With this trade I swallowed a loss, that's true. It is also true that the market is overbought. But, it is strong and you can't deny price action. I swallowed a 0.65 loss on the spread I closed but received 0.70 credit on the new one. I also opened a Put side 1445/1450 early in the day for 0.50 to mitigate this loss. So, in total now I have an Iron Condor 1445/1450/1530/1535 for 1.20 Credit. If it achieves full profit in 20 days, that credit will more than make up for the 0.65 loss I assumed by closing the 1520/1525 Call Credit Spread. And I positioned my self farther away from curent price action. It all feels more comfortable now.

The final Iron Condor looks like this.

(Click on image to enlarge)

Check out Track Record for 2013

Related Articles:

Weekend Portfolio Analysis

Managing RUT Options positions

Weekend Portfolio Analysis (02-02-2013)

Weekend Portfolio Analysis (02-09-2013)

February SPX Call Credit Spread closed

BUY TO CLOSE 5 February 1520 CALL @ 5.30 (Initially sold for 3.75)

SELL TO CLOSE 5 February 1525 CALL @4.00 (Initially bought for 3.10)

A 1.30 debit to close this position. As it had initially been opened for 0.65 credit, the balance here is a 0.65 debit loss. In 5 contracts per leg, that's a $325 loss.

Many Credit Spread sellers don't report a loss like this one. As I am rolling up the position, they consider all the trade adjustments as one single trade whose final balance is reported at the end, when the new position is liquidated. At that point they report the overall balance between the initial credit spread that loss money and the result of the rolled up one. I personally prefer to reflect it right on the spot. Thus avoiding confusion, rather than reporting a whole conglomerate of trades at the end. But in the end is the same thing.

I rolled up 10 points on SPX as follows:

SELL 5 February 1530 CALL @2.85

BUY 5 February 1535CALL @2.15

Credit: $0.70 (0.70 * 100 * 5 = $350)

Margin: $4.30 (4.30 * 100 * 5 = $2150)

Break-even point: 1529.30 (Around 1502 when I entered the trade)

Probability of success: 72.92%

Days to expiration: 20

Max return on margin: 16.28%

Commissions: $15.00 (Assuming a very unfavorable $1.50 per contract)

A chart of the SPX at market close on Friday, January 25, 2013 for future reference.

(Click on image to enlarge)

With this trade I swallowed a loss, that's true. It is also true that the market is overbought. But, it is strong and you can't deny price action. I swallowed a 0.65 loss on the spread I closed but received 0.70 credit on the new one. I also opened a Put side 1445/1450 early in the day for 0.50 to mitigate this loss. So, in total now I have an Iron Condor 1445/1450/1530/1535 for 1.20 Credit. If it achieves full profit in 20 days, that credit will more than make up for the 0.65 loss I assumed by closing the 1520/1525 Call Credit Spread. And I positioned my self farther away from curent price action. It all feels more comfortable now.

The final Iron Condor looks like this.

(Click on image to enlarge)

Check out Track Record for 2013

Related Articles:

Weekend Portfolio Analysis

Managing RUT Options positions

Weekend Portfolio Analysis (02-02-2013)

Weekend Portfolio Analysis (02-09-2013)

February SPX Call Credit Spread closed

Go to the bottom of this page in order to see the Legal Stuff

No comments:

Post a Comment