Recent Trading Activity

- The remainder of the September RUT Elephant reached expiration on Friday for a net $840 gain.

- The remainder of the September RUT Elephant reached expiration on Friday for a net $840 gain.

Market Conditions

(Click on image to enlarge)

McClellan: +113 (Neutral. Up from +39 last week)

Stocks above their 20 DMA: 73% (Overbought. Up from 60% last week)

No man's land but close to an Overbought extreme

Well, the debt ceiling was extended and there wasn't as much drama as in the past. Resistance clearly broken and after Monday that SPX 2,500 level just seemed like a magnet. We're close to overbought, but in this bull market, especially this year, extreme overbought readings have been very scarce and the market has stayed in this, "almost overbought" condition endlessly at times, going up little by little. The world is bullish right now. Hard not to be. But the upside, I feel is a little limited to around SPX 2,520 for this week.

The only hope left for a little downside is "seasonality". We're entering the second half of September which is traditionally the weakest period of the year, especially the fourth week. Other than that, nothing seems to stop the music. Not even nuclear threats by a lunatic in Asia, or two powerful hurricanes affecting two important states of the Union.

Putting fundamentals aside, we'll just lay out a plan and look at price action as usual to determine when to adjust our positions, preserve our capital and when to attack.

The Russell 2000:

(Click on image to enlarge)

Current Portfolio

OCT SPX 2250/2260/2540/2545 Unbalanced Iron Condor

Net Credit of $1,500 and Five weeks to expiration. Put side looking good at 4 deltas. Call side starting to take some heat at 19 deltas. Overall, the position is making money at the moment.

(Click on image to enlarge)

Defense lines: 2,320 to the downside and 2,535 to the upside (you can wait until 45-48 deltas given the low risk exposure on the Call side).

Defense lines: 2,320 to the downside and 2,535 to the upside (you can wait until 45-48 deltas given the low risk exposure on the Call side).

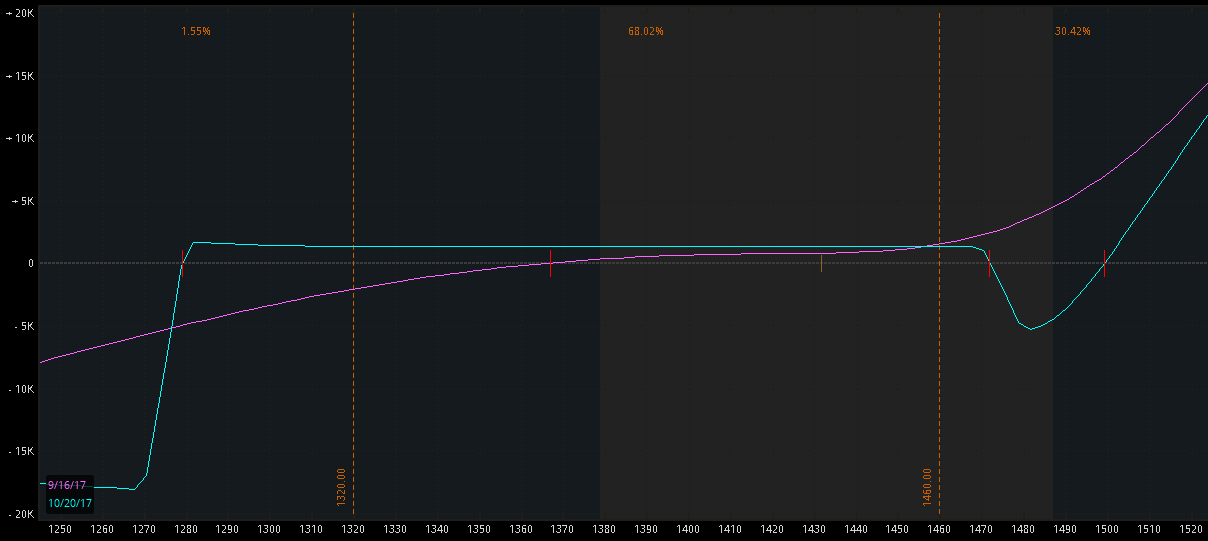

OCT RUT-IWM 1270/1280/1470/1480/130/148 Unbalanced Elephant

Net Credit of $1,317, Five weeks to expiration. Making decent money (pink line) despite RUT's recent rally.

(Click on image to enlarge)

Defense lines: 1,320 (adjust Put side) and 1,460 (close Call side at a loss and continue riding the Put side, whose net credit is greater than the Call side loss at RUT 1,460)

Defense lines: 1,320 (adjust Put side) and 1,460 (close Call side at a loss and continue riding the Put side, whose net credit is greater than the Call side loss at RUT 1,460)

DEC SPY 253 Calls

Small bullish speculative play from August 18th. Three contracts at 1.50 debit each.

Current value of these contracts is 2.95. Still used as upside hedge for any Credit Call spreads that may be threatened in the portfolio.

OCT SPX 2250/2260/2540/2545 Unbalanced Iron Condor

Net Credit of $1,500 and Five weeks to expiration. Put side looking good at 4 deltas. Call side starting to take some heat at 19 deltas. Overall, the position is making money at the moment.

(Click on image to enlarge)

OCT RUT-IWM 1270/1280/1470/1480/130/148 Unbalanced Elephant

Net Credit of $1,317, Five weeks to expiration. Making decent money (pink line) despite RUT's recent rally.

(Click on image to enlarge)

DEC SPY 253 Calls

Small bullish speculative play from August 18th. Three contracts at 1.50 debit each.

Current value of these contracts is 2.95. Still used as upside hedge for any Credit Call spreads that may be threatened in the portfolio.

Action Plan for the Week

The Put sides of both October positions are virtual winners by now. Only the Call sides can inflict some pain and if it happens it will be well under control given how small we've played them. Still, we'll plan our moves assuming the markets will move where it hurts us the most: UP.

- October SPX Unbalanced Iron Condor: I'm closing the Call side at a loss and I'll neutralize this loss by taking gains on the December SPY 253 strike Calls. The SPY Calls are worth 2.95 (give or take on Monday). That's a 1.45 gain per contract ($435 for three contracts in dollar terms). On the other hand, the 2540/2545 Call spread side of the October SPX Unbalanced Iron Condor was initiated for a 0.50 credit and they are currently worth 0.90. That's a 0.40 loss, which represents $320 in 8 spreads. So, we will be making more money via the Dec SPY long Calls than what we lose by closing the SPX 2540/2545 Credit Call spreads. More aggressive traders can wait until the proposed 2535 adjustment point and apply this same operation if that scenario ever takes place. However, at that point, the gains from the SPY Calls will not be enough to eclipse the loss on the SPX Credit Call spreads. I will personally close it all early in the week, except if something drastic happens and suddenly the indexes gap down pre-market on Monday, taking the Delta of the October SPX 2540 Calls below 15.

- After taking the SPX 2540/2545 off the table (along with the December SPY long Calls) I may redeploy a Credit Call spread side if the market rallies to about 2,520. I would like to sell the 2575/2580 for 0.50 credit using a very small position so that I can delay any potential adjustment up to SPX 2,570 which I believe to be a very unlikely price before October expiration.

- Regarding the October RUT Elephant, I'll just keep riding it. The Put side is far from its adjustment condition. The Call side will be closed at a small loss with RUT reaching 1,460. In that event, I will just keep riding the PUT side, whose gain will more than cover the Call side loss.

- Initiate a November SPX Unbalanced Iron Condor late in the week. The current candidate will have its Put side around 2,300 and its Call side around 2,580. It will be hard to obtain the usual credits (0.60 for ten-point wide Put spread. 0.95- 1.00 for a ten-point wide Call spread) due to the extremely low volatility. I'll be happy with 0.50-0.55 on the Put side and 0.85-0.90 on the Call side. I'll probably play this with a 4 to 1 ratio of Put to Call spreads again. More aggressive traders can go 2 to 1.

Forex

The LT Trend Sniper system closed its long Gold (XAUUSD) position at 1,331. The position was held for 13 days and resulted in a +1.98% gain for the FX Account. The Long EURUSD play failed with a 2.47% loss for the Portfolio. With these results the FX Account is now up only +3% for the year.

More details about the LT Trend Sniper automated trading system can be read here.

Forex results are tracked here.

Economic Calendar

We have the Fed Minutes this week, so Wednesday may be a little shaky. I'm planning to enter the November SPX Iron Condor past this meeting. Either on Thursday or Friday.

Tuesday: Housing Starts.

Wednesday: Existing Home Sales. Crude Oil Inventories. Federal Reserve Meeting.

Take it easy folks.

LT

If you are interested in a responsible and sustainable way of trading options for consistent income with solid risk management, consider acquiring LTOptions, my options trading system to the last detail.

Check out 2017 Track Record

Go to the bottom of this page in order to see the Legal Stuff

No comments:

Post a Comment