I have discussed several Forex trading strategies on this blog in the past. Most of the time just exposing trash, scams and over curve-fitted junk, especially during the early life stages of this site. After a while, I realized the amount of garbage was insanely beyond my reach and it didn't make much sense to keep exposing charlatans and endlessly picking fights. I decided to, instead, focus on valuable content showcasing for instance, robust Forex trading strategies with long profitable track records and great likelihood of being profitable in the future under unknown market conditions.

So far I have shared four mechanical trading strategies that meet this criteria but I've never gone back to those articles to provide some sort of follow up, some sort of accountability. This planet doesn't need anymore gurus going around the world talking about supposedly "profitable trading systems" without ever going back to them and showing live forward testing results.

In this post I will share with you the results of these 4 trading strategies during the entire 2014 using the Metatrader platform and price feed provided by the now defunct AlpariUK broker.

EURUSD Donchian breakout strategy with time based exit

This strategy enters on a 70 day Donchian Channel breakout, sets a Stop Loss 2 ATRs away and a Target Profit 3.2 ATRs away. If neither Stop Loss nor Profit Target is achieved in 6 days, the system will simply automatically exit the position as it assumes the initial momentum after the break out may be fading. 3% capital allocation per trade on this test.

(Click on images to enlarge)

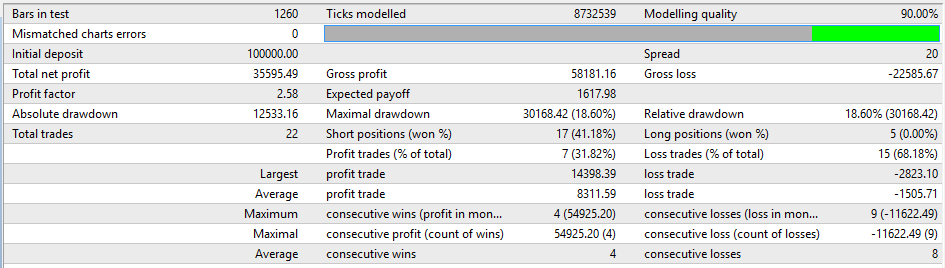

Solid year with a +16.79% return. Metatrader as usual overestimating the draw-down as I have discussed before. This is because it assumes highest account balance with floating profits of open trades included. The reality is, the Max draw-down when considering only closed trades was 16.84%, which is pretty good for the final return achieved. 48 trades in total, 31 winners vs 17 losers.

Solid year with a +16.79% return. Metatrader as usual overestimating the draw-down as I have discussed before. This is because it assumes highest account balance with floating profits of open trades included. The reality is, the Max draw-down when considering only closed trades was 16.84%, which is pretty good for the final return achieved. 48 trades in total, 31 winners vs 17 losers.

50 Day Breakout system with 50 SMA - 100 SMA crossover confirmation

This strategy was kindly shared by Pavel Kařízek, portfolio manager and follower of this site, who trades this mechanical system on several currencies and futures. For simplicity I'll just show the results on the EURUSD in 2014 or else this article would take forever.

Because it is trading on so many instruments at the same time, Pavel trades each one with very low risk settings.

(Click on images to enlarge)

A +3.86% return with a very small 0.37% maximum draw-down (closed positions only) experienced at the beginning of the year. Although this is a small return, take into account the insignificant draw-down and also the fact that this strategy is traded in a portfolio with many other instruments. Still, the return for EURUSD alone beat the 3.31% reported on the Barclay Currency Traders Index last year for Professional Audited Forex traders.

A +3.86% return with a very small 0.37% maximum draw-down (closed positions only) experienced at the beginning of the year. Although this is a small return, take into account the insignificant draw-down and also the fact that this strategy is traded in a portfolio with many other instruments. Still, the return for EURUSD alone beat the 3.31% reported on the Barclay Currency Traders Index last year for Professional Audited Forex traders.

The Turtles Trading System (Method 2)

The legendary Turtles Trading system doesn't need an introduction. This beauty has been killing it since introduced back in the 80's. For more details, click on the link above and enjoy.

How was 2014 for the Turtles Trading system applied to the EURUSD currency pair?

One word: Epic.

(Click on images to enlarge)

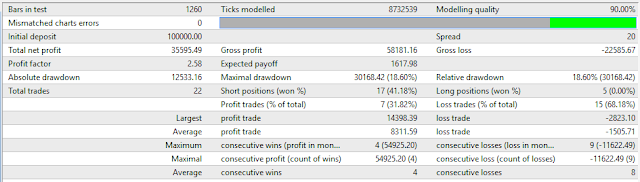

+35.60% return. Some positions still open on December 31 which have to be abruptly closed by the Back-tester). Maximum draw-down of only 11.62% on the equity curve when considering only closed positions. Only 7 winning trades out of 22 but that's just the nature of the Turtle. % of winners is irrelevant.

LT Trend Sniper

Finally, from yours truly, the LT Trend Sniper system: my premium strategy designed for following 2 - 3 month long trends on currencies such as the Euro (EURUSD), the Sterling pound (GBPUSD) and the Australian dollar (AUDUSD).

(Click on images to enlarge)

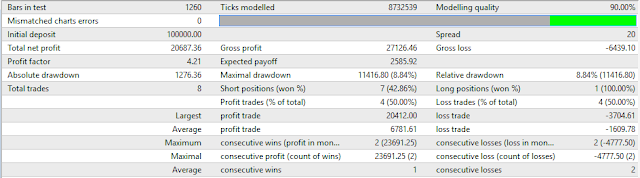

Solid +20.69% return for the year with a real maximum draw-down of only 3.87% which took place from October 9 to December 31. Only 4 winners out of 8 trades. This is the nature of the beast.

When combined in the EURUSD + GBPUSD + AUDUSD portfolio the return was +31.25% with a maximum draw-down of only 10.05% in 2014.

Many traders are entirely opposed to 100% automated trading systems. They say "they don't work". The funny thing is those same traders complain about the fact that the markets today are "dominated" by "algos".

If you believe you have an edge, if you have a trading system with concrete objective rules top to bottom without subjectivity, then it is automatable and saying automated systems don't work will immediately enter in total contradiction with the fact that you have a trading system which you believe has an edge and is profitable.

Profitable automated trading is possible. It has been done. It is happening every day in the markets and it will continue to happen. Just be careful. There is an extraordinary amount of useless garbage out there. Especially in the world of retail Forex trading where automation is more prevalent.

Thanks for reading folks. Stick with the Lazy one.

So far I have shared four mechanical trading strategies that meet this criteria but I've never gone back to those articles to provide some sort of follow up, some sort of accountability. This planet doesn't need anymore gurus going around the world talking about supposedly "profitable trading systems" without ever going back to them and showing live forward testing results.

In this post I will share with you the results of these 4 trading strategies during the entire 2014 using the Metatrader platform and price feed provided by the now defunct AlpariUK broker.

EURUSD Donchian breakout strategy with time based exit

This strategy enters on a 70 day Donchian Channel breakout, sets a Stop Loss 2 ATRs away and a Target Profit 3.2 ATRs away. If neither Stop Loss nor Profit Target is achieved in 6 days, the system will simply automatically exit the position as it assumes the initial momentum after the break out may be fading. 3% capital allocation per trade on this test.

(Click on images to enlarge)

50 Day Breakout system with 50 SMA - 100 SMA crossover confirmation

This strategy was kindly shared by Pavel Kařízek, portfolio manager and follower of this site, who trades this mechanical system on several currencies and futures. For simplicity I'll just show the results on the EURUSD in 2014 or else this article would take forever.

Because it is trading on so many instruments at the same time, Pavel trades each one with very low risk settings.

(Click on images to enlarge)

The Turtles Trading System (Method 2)

The legendary Turtles Trading system doesn't need an introduction. This beauty has been killing it since introduced back in the 80's. For more details, click on the link above and enjoy.

How was 2014 for the Turtles Trading system applied to the EURUSD currency pair?

One word: Epic.

(Click on images to enlarge)

+35.60% return. Some positions still open on December 31 which have to be abruptly closed by the Back-tester). Maximum draw-down of only 11.62% on the equity curve when considering only closed positions. Only 7 winning trades out of 22 but that's just the nature of the Turtle. % of winners is irrelevant.

LT Trend Sniper

Finally, from yours truly, the LT Trend Sniper system: my premium strategy designed for following 2 - 3 month long trends on currencies such as the Euro (EURUSD), the Sterling pound (GBPUSD) and the Australian dollar (AUDUSD).

(Click on images to enlarge)

Solid +20.69% return for the year with a real maximum draw-down of only 3.87% which took place from October 9 to December 31. Only 4 winners out of 8 trades. This is the nature of the beast.

When combined in the EURUSD + GBPUSD + AUDUSD portfolio the return was +31.25% with a maximum draw-down of only 10.05% in 2014.

Many traders are entirely opposed to 100% automated trading systems. They say "they don't work". The funny thing is those same traders complain about the fact that the markets today are "dominated" by "algos".

If you believe you have an edge, if you have a trading system with concrete objective rules top to bottom without subjectivity, then it is automatable and saying automated systems don't work will immediately enter in total contradiction with the fact that you have a trading system which you believe has an edge and is profitable.

Profitable automated trading is possible. It has been done. It is happening every day in the markets and it will continue to happen. Just be careful. There is an extraordinary amount of useless garbage out there. Especially in the world of retail Forex trading where automation is more prevalent.

Thanks for reading folks. Stick with the Lazy one.

Go to the bottom of this page in order to see the Legal Stuff

Hello Henrik,

ReplyDeleteAside from the live "LT Trend Sniper" account shown in MyFxBook, why there's nothing else regarding your other 3 automated systems? Do you have any actual data showing they are still properly performing through 2014-2015?

Regards,

Víctor

Hello Victor,

DeleteThanks for your comments, as they may be the same concern of many other readers.

The answer to your questions. The other 3 automated systems have appeared over time and it is not my intention to trade every single system live. In fact, although I have published four on this site, I receive ideas, links and comments about robots and automated systems almost on a weekly basis. It would be impractical to show-case hundreds of systems here or to just go ahead and trade them all myself on separate accounts to isolate their performance.

These are not really "my systems" so it is not my intention to take the credit and pretend they are by taking more ownership than just explaining them on the site. Actually the Turtles Trading system in particular is not "mine", nor is the 50 Day break out with Moving average confirmation either. But, unlike black boxes from unscrupulous vendors that pollute the internet, there is no secrecy with these ones. All the rules are there. The fact that the trading rules of both are publicly available makes it unnecessary to consume space and add clutter to the site with more accounts showing results updated every x minutes. You typically do that to convince people of how good your black box system is and sell it to them. So, as a matter of, let's say principles, I showcase the returns of the Sniper live as I believe it is my best creation and also because the rules are not public and it is the one I trade with real money. The one I most trust.

The returns of all these systems will of course be updated. I just have to buy high quality data from a reputable provider and I am waiting until the end of the year in order to have the full 12 months. But yes, count on it I will definitely talk about the performance of all these systems for better or worse, but again I just want to purchase the data once, instead of now, and then again at the end of the year. My intention is to do the same thing every year going forward.

As for performance in 2014-2015. Well the results for 2014 are the ones published on this article. As for 2015, the systems are performing decently well thanks to the fact that the Euro experienced nice trends in the first half of the year. They are all between +5% to +20% growth but of course these numbers are bound to change during what is left of the year. All the numbers will be available in a few weeks.

Thanks again for dropping by Victor and leaving your questions. I really appreciate it.

Best,

LT

Henrik,

DeleteThanks a lot for your quick, lengthy and super detailed reply. I also really appreciate it :)

I totally comprehend what you said.

After analyzing a little more about how your published EA systems work (not all of their rules are yours, but IT IS the coding and kind sharing), I have noticed that the "LT Trend Sniper", "Donchian Breakout Strategy (50Day-Breakout)" and "Turtles Trading System 2", equally relay on the same basic breakout principles. Hence, I would like to ask you, if you think it could be a good idea to include another configurable Input parameter to the "LT Trend Sniper" and "Turtles Trading System 2" EAs, which only the "50Day-Breakout" system has: the customized ATR Period... I strongly believe it would be a very useful addition, in order to be able to further customize and optimize them according to different market conditions with constantly varying volatility.

Best regards,

Víctor

This comment has been removed by the author.

ReplyDeleteThey do work based on the similar principle of Donchian break out. The difference is in how positions are managed, how exits are decided. But, because they rely on the same entry principle, that is why they are correlated strategies and I don't advice using them all on the same account at the same time, except with low risk settings for each as draw-downs can coincide in the portfolio.

DeleteYour idea about the ATR setting can be considered. I don't think it will change things a lot as entries will still be the same (Donchian channel is unrelated to ATR). Usually the parameters used for ATR are either 14 or 20, so I didn't see much variability and potential in this. But it is a good idea to let the user specify. I will look into it.

LT

Hey Henrik,

DeleteYes. I meant the ATR Period (in days) used to calculate Stop Loss "distance"... Wouldn't that influence the process significantly enough to alter the outcome?

Yes it does alter it. But the default values were the best as far as I remember. Of course if you use something like ATR(1), ATR(5), ATR(3) of course things could drastically change.

DeleteLT

Of course, haha... But varying it between ATR(15) and ATR(100), may show a valid statistical edge, making worthwhile ;-)... I'll be gladly looking into if in the case you finally decide to implement it!

DeleteVíctor