Trade Details:

3 March SPX 2985/2975 Credit Put spread @0.70 credit each

1 March SPX 3450/3460 Credit Call spread @1.20 credit

I went with a 3x1 ratio instead of the usual 4x1. Totally at my discretion. I feel it is not the right time to be overly exposed on the downside.

Net Credit: $330

Max Risk: $2,670

56 days to Exp.

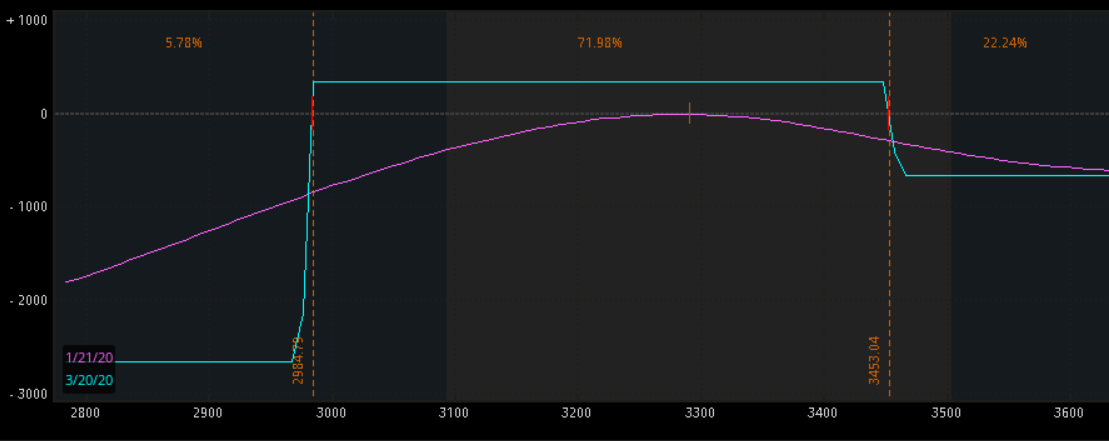

Profit/Risk Profile

SPX Chart for future reference:

3 March SPX 2985/2975 Credit Put spread @0.70 credit each

1 March SPX 3450/3460 Credit Call spread @1.20 credit

I went with a 3x1 ratio instead of the usual 4x1. Totally at my discretion. I feel it is not the right time to be overly exposed on the downside.

Net Credit: $330

Max Risk: $2,670

56 days to Exp.

Profit/Risk Profile

SPX Chart for future reference:

Trade Update - February 11, 2020

Closed Call side:

1 March SPX 3450/3460 Credit Call spread @2.60 debit

Original credit: 1.20

Net loss: $140

The Put side 2985/2975 (credit of $210) will remain.

Trade Update - February 19, 2020

Closed the Put side:

3 March SPX 2985/2975 Credit Put spread @0.15 debit each

Original credit: 0.70

Net gain: 0.55 x 3 = $165

Combining this profit with the earlier loss on the Call side we have a net +$25 winner (165 - 140)

Tiny winner, basically a scratch.

On a max risk of $2,670 this represents a +0.9% Return on Risk.

The entire position is now closed.

There were only 0.15 more to make in this position. $45 for 3 Credit Put spreads. With 29 days to expiration this means about $1.55 per day. However, I can now deploy an April position 8 weeks out, collecting about $350 which represents more than $6/day of potential profits. So, at this point it was better to close the March position and move on.

Check out Track Record

Closed Call side:

1 March SPX 3450/3460 Credit Call spread @2.60 debit

Original credit: 1.20

Net loss: $140

The Put side 2985/2975 (credit of $210) will remain.

Trade Update - February 19, 2020

Closed the Put side:

3 March SPX 2985/2975 Credit Put spread @0.15 debit each

Original credit: 0.70

Net gain: 0.55 x 3 = $165

Combining this profit with the earlier loss on the Call side we have a net +$25 winner (165 - 140)

Tiny winner, basically a scratch.

On a max risk of $2,670 this represents a +0.9% Return on Risk.

The entire position is now closed.

There were only 0.15 more to make in this position. $45 for 3 Credit Put spreads. With 29 days to expiration this means about $1.55 per day. However, I can now deploy an April position 8 weeks out, collecting about $350 which represents more than $6/day of potential profits. So, at this point it was better to close the March position and move on.

Check out Track Record

Go to the bottom of this page in order to see the Legal Stuff

No comments:

Post a Comment