Recent Trading Activity

- Initiated an SPX 2250/2240 Credit Call spread in the May expiration cycle on Friday. Credit received $1,200.

- Initiated an SPX 2250/2240 Credit Call spread in the May expiration cycle on Friday. Credit received $1,200.

Market Conditions

(Click on image to enlarge)

McClellan: -195 (Neutral. Down from +53)

Stocks above their 20 DMA: 23% (Oversold. Down from 64%)

Oversold environment

Or 'Short-term Extreme pessimism' I like to call it too.

The best time for Credit Put spreads. Only accentuated with the VIX near 25.

For example, using May options, the 2240/2230 Credit Put spread can be sold for 0.60 credit. That's 13% below current price 22% below the all-time highs.

Markets retraced almost 6% this week. That's significant for a week. Even though, in my view, corporate America is healthy. The 200-Day average may be a magnet now, and it has been a long time since we last saw a closing price below it. I will take advantage of it to establish some long-term stock positions or add to existing ones. But that's beyond the scope of this Options trading oriented article.

The Russell Index:

(Click on image to enlarge)

Current Portfolio:

The SPY Calls and SVXY Calls expire in December and January of next year. All bullish bets on a market rebound.

The SPY Calls and SVXY Calls expire in December and January of next year. All bullish bets on a market rebound.

Let's now look at the income plays.

Apr. SPX/SPY 2440/2450/2890/2900 - 290 Elephant

Net Credit: $1,608 and four weeks to expiration.

(Click on image to enlarge)

Defense line: 2,535 (adjust the Put side). In reality, it is whenever the 2450 Calls reach 30 deltas. 2,535 is just a price estimate. If the adjustment condition is triggered. I'll adjust using the same April options.

Defense line: 2,535 (adjust the Put side). In reality, it is whenever the 2450 Calls reach 30 deltas. 2,535 is just a price estimate. If the adjustment condition is triggered. I'll adjust using the same April options.

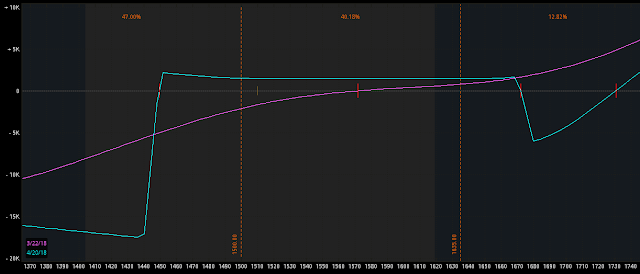

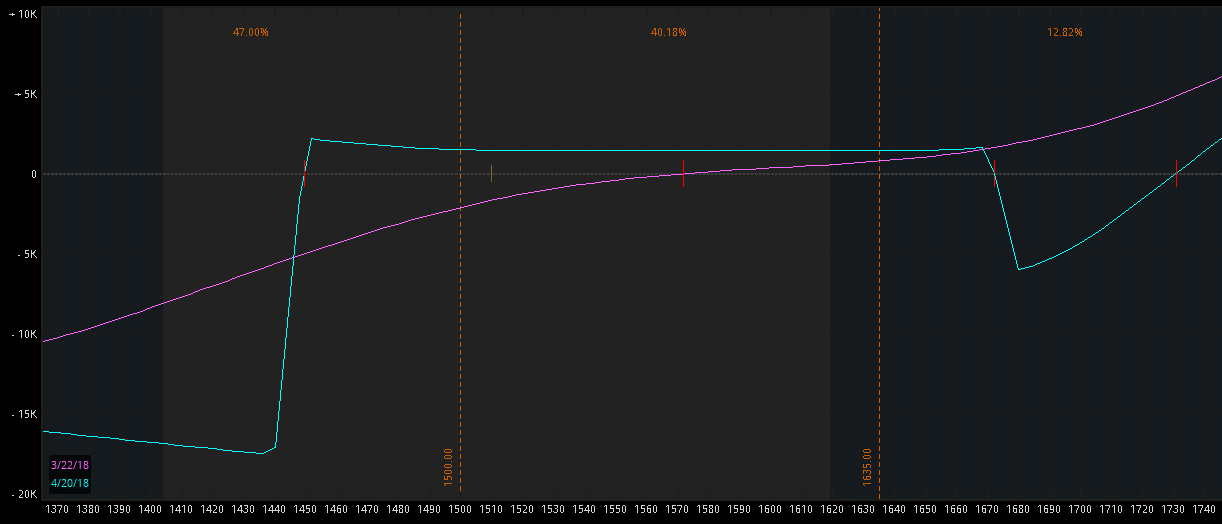

Apr. RUT/IWM 1450/1460/1670/1680 - 148/168 Elephant

Net Credit: $1,445 and four weeks to expiration

(Click on image to enlarge)

Defense

line: 1,500 (adjust the Put side). Again this is just a price estimate. The real trigger is when the 1460 Puts reach 30 deltas. If it happens, I'll adjust using April options.

Defense

line: 1,500 (adjust the Put side). Again this is just a price estimate. The real trigger is when the 1460 Puts reach 30 deltas. If it happens, I'll adjust using April options.

May SPX 2250/2240 Credit Put spread

Net Credit: $1,200. Eight weeks to expiration.

Brand new position established just a few hours ago. Well Out of the Money. Lots of baby-sitting ahead.

(Click on image to enlarge)

Let's now look at the income plays.

Apr. SPX/SPY 2440/2450/2890/2900 - 290 Elephant

Net Credit: $1,608 and four weeks to expiration.

(Click on image to enlarge)

Apr. RUT/IWM 1450/1460/1670/1680 - 148/168 Elephant

Net Credit: $1,445 and four weeks to expiration

(Click on image to enlarge)

May SPX 2250/2240 Credit Put spread

Net Credit: $1,200. Eight weeks to expiration.

Brand new position established just a few hours ago. Well Out of the Money. Lots of baby-sitting ahead.

(Click on image to enlarge)

Action Plan for the Week

- I'll just be baby-sitting positions for possible adjustments of the RUT and SPX April Elephants. Adjustments will be made using April options.

Economic Calendar

Tuesday: CB Consumer Confidence.

Wednesday: US GDP and Pending Home Sales.

Friday: China's Manufacturing PMI.

Good luck this week folks,

LT

If you are interested in a responsible and sustainable way of trading options for consistent income with solid risk management, consider acquiring LTOptions, my options trading system to the last detail.

Check out 2018 Track Record

Go to the bottom of this page in order to see the Legal Stuff

No comments:

Post a Comment