Recent Trading Activity

- Initiated a small Dec29 RUT 1590/1600 Credit Call spread for 0.90 credit ($450) on Tuesday.

- Closed Dec29 RUT 1330/1320 Credit Put spreads for a small $225 gain on Tuesday. Initiated a 1420/1410 Credit Put spread ($335) credit. So, basically I just rolled the old Put spread up, locking some gains in the process. The Dec29 RUT position is now a balanced 1410/1420/1590/1600 Iron Condor. It is a small position made up of only 5 vertical spreads on each side. So, one quarter the usual size.

- Initiated the first position of 2018: a January SPX 2440/2450/2685/2690 Unbalanced Iron Condor. Four to one ratio of Puts to Call and a net credit of $1700.

- It was not possible to close the December SPX 2635/2640 Credit call spreads for the 0.30 debit I wanted to lock in a small winner and forget about it.

- Initiated a small Dec29 RUT 1590/1600 Credit Call spread for 0.90 credit ($450) on Tuesday.

- Closed Dec29 RUT 1330/1320 Credit Put spreads for a small $225 gain on Tuesday. Initiated a 1420/1410 Credit Put spread ($335) credit. So, basically I just rolled the old Put spread up, locking some gains in the process. The Dec29 RUT position is now a balanced 1410/1420/1590/1600 Iron Condor. It is a small position made up of only 5 vertical spreads on each side. So, one quarter the usual size.

- Initiated the first position of 2018: a January SPX 2440/2450/2685/2690 Unbalanced Iron Condor. Four to one ratio of Puts to Call and a net credit of $1700.

- It was not possible to close the December SPX 2635/2640 Credit call spreads for the 0.30 debit I wanted to lock in a small winner and forget about it.

Market Conditions

(Click on image to enlarge)

McClellan: +78 (Neutral. Up from -22 last week)

Stocks above their 20 DMA: 64% (Neutral. Up from 49% last week)

No man's land.

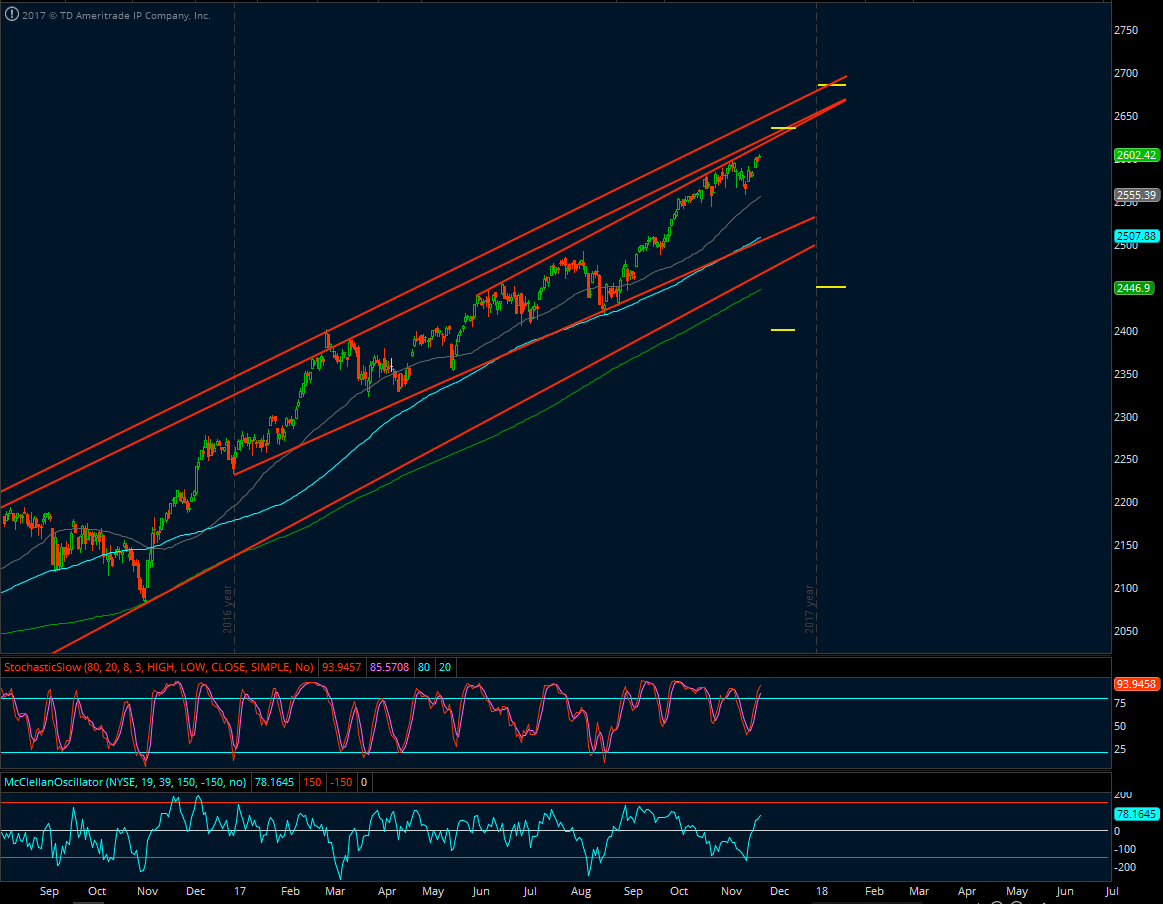

The overbought territory obviously much closer than the oversold one. The % of stocks above their 20 DMA is getting close to the 70% threshold. The index is getting closer to the upper end (resistance) of the long-term uptrend channel. There is still some little room there (2,620-2,625 max this upcoming week). Unfortunately our 2635/2640 Credit Call spread is pretty close to the projected trend-line at expiration and it hasn't caught a break. We'll deal with it in a few minutes. The index is 1.8% higher than its average, effectively leaving some more upside room.

The Russell:

(Click on image to enlarge)

Current Portfolio

DEC SPX 2390/2400/2635/2640 Unbalanced Iron Condor

Net credit: $1,555. Three weeks to expiration. Put side looking great at 3 deltas. The Call side is again causing some minor headaches. 21 Deltas, up from 11 last week.

(Click on image to enlarge)

Defense lines: 2,450 to the downside (adjust Put side) and 2,630 to the upside (adjust Call side). We can delay the Call side adjustment given the conservative 4 to 1 ratio of Puts/Calls played in this position. The position is still a winner at this point if you were to take it off the table entirely. A bigger winner than that if you take off just the Call side at a loss and let the Put side expire for max gains.

Defense lines: 2,450 to the downside (adjust Put side) and 2,630 to the upside (adjust Call side). We can delay the Call side adjustment given the conservative 4 to 1 ratio of Puts/Calls played in this position. The position is still a winner at this point if you were to take it off the table entirely. A bigger winner than that if you take off just the Call side at a loss and let the Put side expire for max gains.

DEC RUT 1370/1380/1570/1580 Unbalanced Iron Condor

Net credit: $1,555. Three weeks to expiration. 4 deltas on the PUT side and 14 deltas on the Call side (up from just 7 last week).

(Click on image to enlarge)

Defense lines: 1,420 to the downside (adjust Put side) and 1,565 to the upside (adjust Call side).

Defense lines: 1,420 to the downside (adjust Put side) and 1,565 to the upside (adjust Call side).

DEC29 RUT 1410/1420 Credit Put spread

A small $785 credit and five weeks to expiration. Not a concern for now.

(Click on image to enlarge)

Defense line: 1,425 (adjust Put side) and 1585 (adjust Call side)

Defense line: 1,425 (adjust Put side) and 1585 (adjust Call side)

Because of the small position size we can delay the adjustments on both sides.

The downside adjustment point here is just 5 points higher than the previous RUT position. So, clearly some risk concentration here. This one however, is a very small position. So, I'm not too worried with this risk concentration.

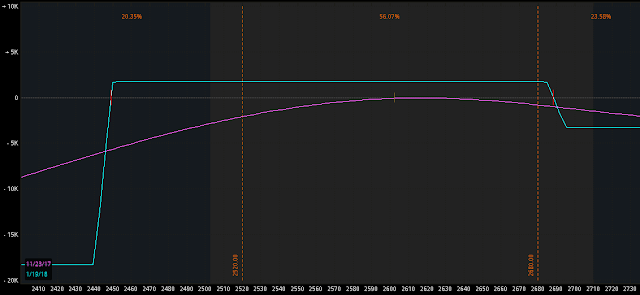

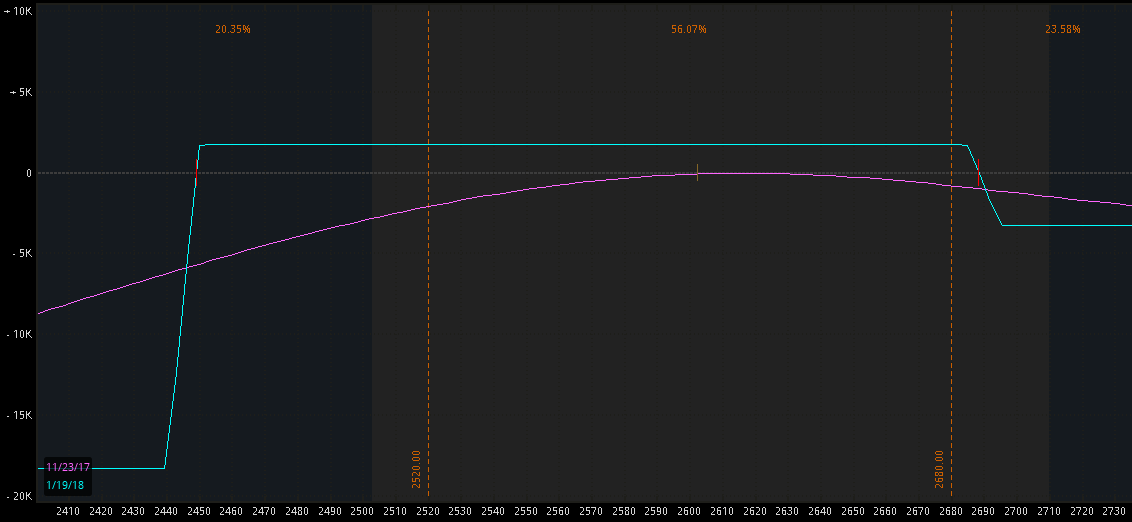

Jan. SPX 2440/2450/2685/2695 Unbalanced Iron Condor

The first 2018 position. Too young to be in danger. Lots of baby-sitting ahead.

$1,700 credit, eight weeks to expiration. A four to one ratio of Puts to Calls also being played here.

(Click on image to enlarge)

Defense lines: 2,520 (adjust Put side) and 2,680 (adjust Call side). Shouldn't give us any trouble for the time being.

Defense lines: 2,520 (adjust Put side) and 2,680 (adjust Call side). Shouldn't give us any trouble for the time being.

DEC SPX 2390/2400/2635/2640 Unbalanced Iron Condor

Net credit: $1,555. Three weeks to expiration. Put side looking great at 3 deltas. The Call side is again causing some minor headaches. 21 Deltas, up from 11 last week.

(Click on image to enlarge)

DEC RUT 1370/1380/1570/1580 Unbalanced Iron Condor

Net credit: $1,555. Three weeks to expiration. 4 deltas on the PUT side and 14 deltas on the Call side (up from just 7 last week).

(Click on image to enlarge)

DEC29 RUT 1410/1420 Credit Put spread

A small $785 credit and five weeks to expiration. Not a concern for now.

(Click on image to enlarge)

Because of the small position size we can delay the adjustments on both sides.

The downside adjustment point here is just 5 points higher than the previous RUT position. So, clearly some risk concentration here. This one however, is a very small position. So, I'm not too worried with this risk concentration.

Jan. SPX 2440/2450/2685/2695 Unbalanced Iron Condor

The first 2018 position. Too young to be in danger. Lots of baby-sitting ahead.

$1,700 credit, eight weeks to expiration. A four to one ratio of Puts to Calls also being played here.

(Click on image to enlarge)

Action Plan for the Week

Well, evidently the boat is pretty loaded folks. Four positions on, all of them with Call side exposure which is the true killer in this market. The positions don't look terrible thanks to the fact that Call side risk is considerably smaller in three of them. The only one where the Iron Condor is fully balanced is a small position consisting of only one fourth the typical capital investment. However, despite this, I don't want to be adjusting a Credit Call spread two days before expiration or anything like that. So, here are my personal ideas for this week.

- I'll take the DEC SPX 2635/2640 Credit Call spreads off the table on Monday at a loss. The current debit to pay is 0.85. This would represent a 0.35 loss (0.50 credit received originally). In 10 spreads that would be a $350 loss. If the market opens lower, it will be possible to exit with a smaller loss than this (even at no loss at some tiny 10 points). This idea may not sit well with more aggressive traders out there. In any case you can indeed wait until SPX 2630 to make an adjustment, effectively giving you more time to be right. I am just tired of this Credit Call spread and adjustments the week of expiration rub me the wrong way. But granted, there is still sometime until then. Once I take the loss on the 2635/2640 Call spread, I will somehow mitigate it by selling a small Credit Put spread. I'll go with the same DEC15 Expiration, and the spread will be around 2525. If that strike price feels too close to you, you can go to Dec29 and trade around SPX 2,480 for similar credits. The goal with the Put spread is to obtain a similar credit to whatever is lost closing the 2635/2640 Call side. Because this new Put spread will be small, I will not think about adjusting it unless the market gets really close to it, like SPX 2,530 or something like that. If after taking the 2635/2640 side off the market rallies 15 or 20 points I will seriously consider a small Call spread around 2,670.

- Regarding the DEC RUT 1370/1380/1570/1580 Unbalanced Iron Condor

Call side at 14 deltas, and adjustment condition at 1,565. Still far. But I'm going to do something here for my own comfort in this stubborn 2016 market. I'll buy IWM 157 Calls, using half the credit ($230) that was obtained from the 1570/1580 Credit Call spread. At the same time, I will try to collect that same amount from selling a Put spread around 1,450. Obviously, I'm adopting a pretty bullish stance into year end. Something others may not be too comfortable with. If so, just wait until RUT 1,565 to adjust, giving yourself more time to be right without adding more capital (risk into the equation). Anyways, the 4 to 1 ratios have helped us a lot this year. I will not make the addition to the position if suddenly the markets open weak on Monday right off the gate.

That's it. With four positions on, it is time to think 'Defense' and forget about deploying new income plays for now.

Economic Calendar

Monday: US New Home Sales.

Tuesday: US CB Consumer Confidence.

Wednesday: US GDP. China's Manufacturing and Non-Manufacturing PMI.

Thursday: Europe's CPI

Friday: US ISM Manufacturing Employment and PMI

Good luck this week my friends!

LT

If you are interested in a responsible and sustainable way of trading options for consistent income with solid risk management, consider acquiring LTOptions, my options trading system to the last detail.

Check out 2017 Track Record

Go to the bottom of this page in order to see the Legal Stuff

No comments:

Post a Comment