Recent Trading Activity

- Closed the 2465/2475 Call side of the June SPX Unbalanced Iron Condor for a small $180 gain on Monday. As planned over the weekend, this was a spread that needed to be closed simply due to risk concentration in the portfolio. It proved to be the right move.

- Closed the 2465/2475 Call side of the June SPX Unbalanced Iron Condor for a small $180 gain on Monday. As planned over the weekend, this was a spread that needed to be closed simply due to risk concentration in the portfolio. It proved to be the right move.

Market Conditions

(Click on image to enlarge)

McClellan: +82 (Neutral. Up from +41 last week)

Stocks above their 20 DMA: 62% (Neutral. Up from 47% last week)

No man's land.

It's a bit frustrating that in the last few years the market has been mostly in straight up mode and volatility low most of the time, making the options selling business that much harder. I'll be the first to admit it. As I've argued many times before, this is the hardest environment for the Options seller. 2010-2012, when I started trading, was glorious, and the +40% +50% +60% annual returns were easy to come by out there. At one point it even seemed normal. On the other hand, earlier this century the index spent 13 years going nowhere. Following it was certainly frustrating for passive investors. But, enough with the lamentations. Let's just focus on the card we've been dealt for now.

There is still upside room, suggested by both McClellan and the % of Stocks above their 20 DMA, what many people call "Breadth". Technically speaking, there is also room left between price and the upper end of the long term uptrend channel. Finally, the price of the index is 2.6% higher than its 50-day average. We have seen this number peak between 3.5% - 4% in the past for SPX (RUT is a different animal in this regard). If SPX were to reach that extreme distance above its 50-day moving average before it takes a breaks and "rests", we'd be looking at SPX 2,460 - 2,472 in the short term. We have a July Unbalanced Iron Condor with 2,490 as its short Call component, and we'll be looking at possible defenses.

At the end of the week we will be 6 weeks away from July expiration and therefore I'll be looking to initiate a July RUT Elephant position.

...and speaking of Russell 2000:

(Click on image to enlarge)

Current Portfolio

JUN SPX 2240/2250 Credit Put spread hedged with SPY 228 long Put

Net credit: $1042. This is the remainder of an Unbalanced Iron Condor. Looking like an almost sure winner now very far out of the money at only 1 delta. I plan to hold it until expiration.

JUL SPX 2250/2260/2490/2500 Unbalanced Iron Condor

$2150 credit. 7 weeks to expiration. Put side looking good at 8 deltas. Call side taking some heat at 21 deltas.

Adjustment point to the downside: 2,330.

Regarding the upside, we have several alternatives:

- If you are truly afraid of more market upside, closing the 2490/2500 Credit Call spread now is an option. At 1.85 debit, minus the original credit received 0.95, it is a 0.90 loss per spread ($900 bucks in 10 spreads). That loss can be eventually covered by the $1200 credit obtained from the 2260/2250 Credit Put spread side, resulting in a net winner, albeit small. I won't do this, as I think it is giving up too soon on this position with short strike at 2490.

- We can adjust the 2490/2500 Credit Call spread as usual once it reaches 30 deltas. This spread would be reaching 30 deltas with SPX hitting 2,455 or so this week (you can also set an automatic alert directly based on the Deltas. Instructions here). To estimate the loss, let's look at the current Credit Call spread at 30 deltas (2475/2485). Its mid price is 2.85. So, presumably, this would be the debit we would have to pay in order to close our "threatened Call spread" when it reaches 30 deltas. Let's not be too optimistic and assume that instead of 2.85 debit, we will need to pay 2.90. Well 2.90 minus 0.95 original credit = 1.95 net loss = $1,950 for 10 spreads. This loss would be mitigated by the $1,200 credit from the Put side resulting in a final $750 loss, or less than 1% of the portfolio. At this point the more conservative trader can just forget about it and not deploy a new Call spread. Or, alternatively, we can deploy at the new 10-delta mark which will be approximately SPX 2530/2540. With the new credit the position can still be a winner in the end. This is the good thing about the Unbalanced IC: you can still end up with an overall profitable position after a first adjustment on the Call side, even without increasing the size of your bet.

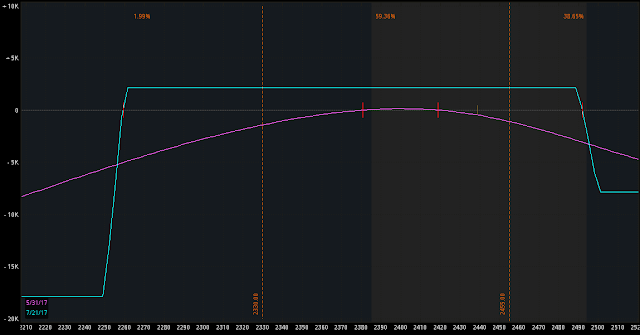

- Another approach is to not give up with SPX hitting 2,455, which still seems a little far from or short Call strike at 2,490. For this, we turn the Unbalanced Iron Condor into an Unbalanced Elephant and flatten out the T+0 line. We can buy one of the 2,500 strike price Call options. We can buy a 2,490 strike Call, a little more expensive but offers a bit more protection. Or alternatively we can buy 10 or 12 SPY 249 strike Calls, for an easier fill given the better liquidity, and smaller total debit despite the greater commissions. This is how the position looks with the theoretical addition of 12 SPY 249 strike Calls:

T+0 line (pink line) now much smoother to the upside. With this addition I would be waiting until SPX 2,475 to think about adjustments again. The downside is that the debit invested would be decreasing the overall profitability of our original Iron Condor. So, we reduce potential profit in exchange for more peace of mind. If SPX reaches 2,475 then the adjustment can be deployed higher at around SPX 2,550. We have used this approach in the past. For more details read An Alternative way to defend Credit Call spread positions. This is the strategy I will be using, but either one of the other two is fine as well.

T+0 line (pink line) now much smoother to the upside. With this addition I would be waiting until SPX 2,475 to think about adjustments again. The downside is that the debit invested would be decreasing the overall profitability of our original Iron Condor. So, we reduce potential profit in exchange for more peace of mind. If SPX reaches 2,475 then the adjustment can be deployed higher at around SPX 2,550. We have used this approach in the past. For more details read An Alternative way to defend Credit Call spread positions. This is the strategy I will be using, but either one of the other two is fine as well.

JUN SPX 2240/2250 Credit Put spread hedged with SPY 228 long Put

Net credit: $1042. This is the remainder of an Unbalanced Iron Condor. Looking like an almost sure winner now very far out of the money at only 1 delta. I plan to hold it until expiration.

JUL SPX 2250/2260/2490/2500 Unbalanced Iron Condor

$2150 credit. 7 weeks to expiration. Put side looking good at 8 deltas. Call side taking some heat at 21 deltas.

Adjustment point to the downside: 2,330.

Regarding the upside, we have several alternatives:

- If you are truly afraid of more market upside, closing the 2490/2500 Credit Call spread now is an option. At 1.85 debit, minus the original credit received 0.95, it is a 0.90 loss per spread ($900 bucks in 10 spreads). That loss can be eventually covered by the $1200 credit obtained from the 2260/2250 Credit Put spread side, resulting in a net winner, albeit small. I won't do this, as I think it is giving up too soon on this position with short strike at 2490.

- We can adjust the 2490/2500 Credit Call spread as usual once it reaches 30 deltas. This spread would be reaching 30 deltas with SPX hitting 2,455 or so this week (you can also set an automatic alert directly based on the Deltas. Instructions here). To estimate the loss, let's look at the current Credit Call spread at 30 deltas (2475/2485). Its mid price is 2.85. So, presumably, this would be the debit we would have to pay in order to close our "threatened Call spread" when it reaches 30 deltas. Let's not be too optimistic and assume that instead of 2.85 debit, we will need to pay 2.90. Well 2.90 minus 0.95 original credit = 1.95 net loss = $1,950 for 10 spreads. This loss would be mitigated by the $1,200 credit from the Put side resulting in a final $750 loss, or less than 1% of the portfolio. At this point the more conservative trader can just forget about it and not deploy a new Call spread. Or, alternatively, we can deploy at the new 10-delta mark which will be approximately SPX 2530/2540. With the new credit the position can still be a winner in the end. This is the good thing about the Unbalanced IC: you can still end up with an overall profitable position after a first adjustment on the Call side, even without increasing the size of your bet.

- Another approach is to not give up with SPX hitting 2,455, which still seems a little far from or short Call strike at 2,490. For this, we turn the Unbalanced Iron Condor into an Unbalanced Elephant and flatten out the T+0 line. We can buy one of the 2,500 strike price Call options. We can buy a 2,490 strike Call, a little more expensive but offers a bit more protection. Or alternatively we can buy 10 or 12 SPY 249 strike Calls, for an easier fill given the better liquidity, and smaller total debit despite the greater commissions. This is how the position looks with the theoretical addition of 12 SPY 249 strike Calls:

Action Plan for the Week

- I'll purchase 10 or 12 SPY Call options, strike price 249, July expiration as an upside hedge to the 2250/2260/2490/2500 Unbalanced Iron Condor.

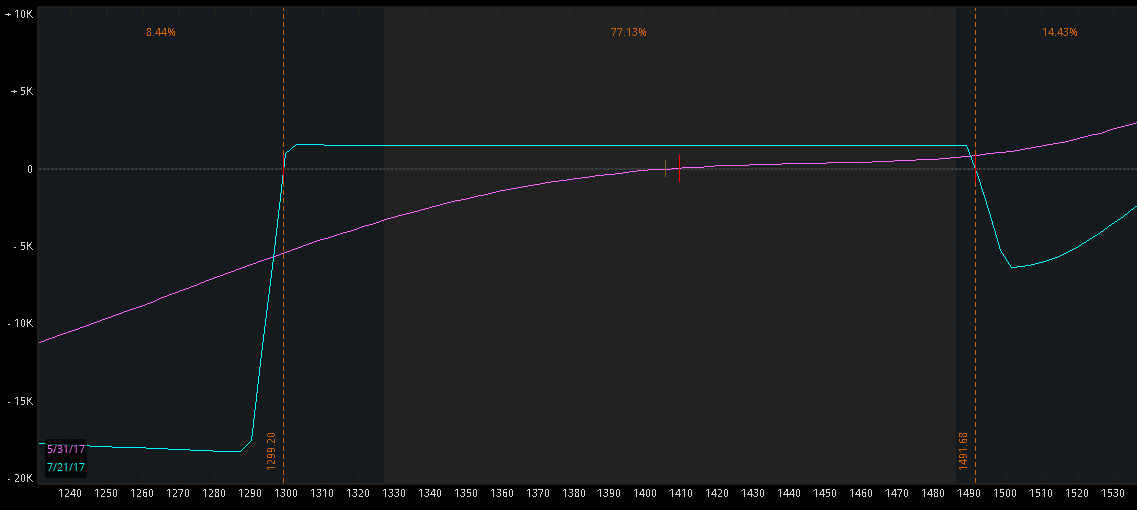

- Initiate a RUT Unbalanced Elephant in the July expiration cycle (mid to late in the week). Right now it's looking like 1290/1300/1490/1500, number of contracts 20/20/8/8. Hedged with long IWM 131/150 unbalanced Strangle, 1 and 19 contracts respectively:

Forex

Decent progress for the long EURUSD position by the LT Trend Sniper system

Stop loss continues at the break-even level. More than 4% account growth with the open profits accumulated so far.

More details about this robot here.

Sniper's results tracked here.

Economic Calendar

Monday: US Non-Manufacturing PMI.

Thursday: China's CPI & PPI.

Friday: US Non-Farm Payrolls. Unemployment Rate.

Good luck this week folks,

LT

If you are interested in a responsible and sustainable way of trading options for consistent income with solid risk management, consider acquiring LTOptions, my options trading system to the last detail.

Check out 2017 Track Record

Go to the bottom of this page in order to see the Legal Stuff

No comments:

Post a Comment