Recent Trading Activity

- Purchased July SPX 249 Calls as upside hedge for existing July SPX Unbalanced Iron Condor on Tuesday. A debit was invested here that eats into the overall profitability of the Unbalanced IC, but only partially. There is still money to make here and the upside hedge allows me to sleep better at night. More on this position in a few minutes.

- Initiated a July RUT Unbalanced Lazy Elephant on Friday for a net credit of $1,417. This is the second position deployed in the July cycle, and last one unless we get an oversold condition.

- Purchased July SPX 249 Calls as upside hedge for existing July SPX Unbalanced Iron Condor on Tuesday. A debit was invested here that eats into the overall profitability of the Unbalanced IC, but only partially. There is still money to make here and the upside hedge allows me to sleep better at night. More on this position in a few minutes.

- Initiated a July RUT Unbalanced Lazy Elephant on Friday for a net credit of $1,417. This is the second position deployed in the July cycle, and last one unless we get an oversold condition.

Market Conditions

(Click on image to enlarge)

McClellan: +29 (Neutral. Down from +82 last week)

Stocks above their 20 DMA: 64% (Neutral. Up from 62% last week)

No man's land. The same condition we've seen throughout the entire year.

Interesting to see the number of stocks above their 20-Day average went up, while the other two oscillators went down. Small incipient bearish divergence there. This week is the FOMC Statement, and the entire universe is expecting a rate hike. Given that it is so expected, my expectation is that markets won't drastically correct that day. My believe is that the hike is pretty much priced in. But regardless, there are price levels I'll always respect to defend the capital at risk that make my bias irrelevant.

I added a new uptrend line that connects the December the 2nd's lows with the May 8th lows and it may be our medium term guide for now. I'll be looking at that line with interest for potential support (situated this week around SPX 2,390). As for the upside, you know the drill; the sky has been the limit this year. Hard to call a top or even dare, but the first diagonal resistance points to a max of SPX 2,475 for the week. I don't think we'll get there but a plan will be put in place anyway.

Here's the other major index I love to play. Actually, I've been liking the RUT more and more lately. RUT touched the upper diagonal resistance line and reversed like an obedient puppy. It's amazing how these lines sometimes work. As strange as it is to experience it in real time, it nailed it to the penny (I promise I haven't re-drawn anything on this chart that's been like these for months):

(Click on image to enlarge)

Current Portfolio

JUN SPX 2240/2250 Credit Put spread hedged with SPY 228 long Put

Net credit: $1042. The remainder of what originally was an Unbalanced Iron Condor. Looking great. Will expire this Friday for max profit.

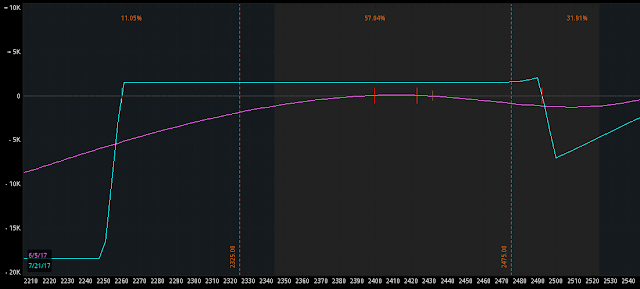

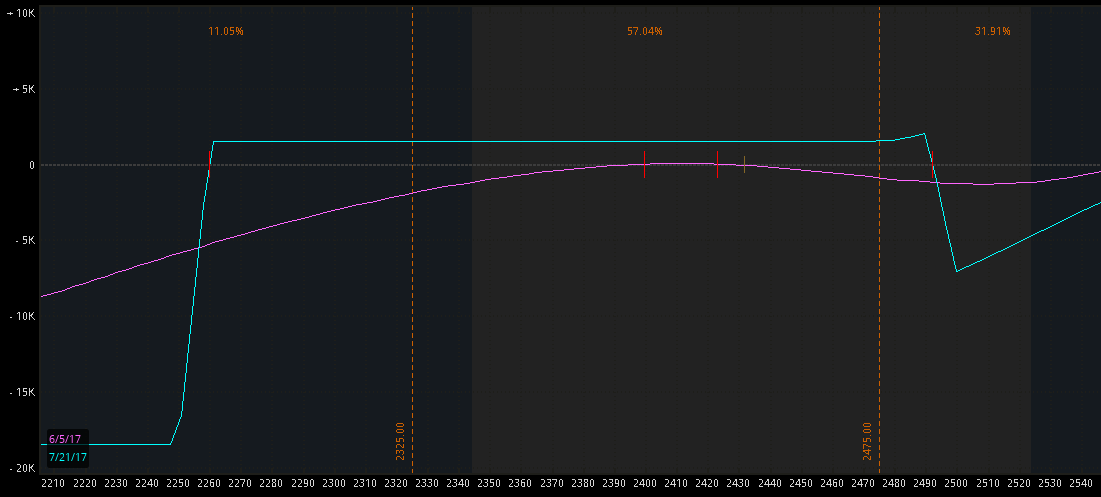

JUL SPX 2250/2260/2490/2500 Unbalanced Iron Condor

hedged to the upside with SPY 249 Calls

6 weeks to expiration. With the addition of the hedge, the net credit and maximum profit potential decreased from $2,150 to $1,540. In exchange for that, we have a smoother risk curve to the upside and a higher defense line at SPX 2,475.

(Click on image to enlarge)

Adjustment point to the downside: 2,325 (Close Put spread for a loss, deploy new spread at the 10 delta mark).

Adjustment point to the downside: 2,325 (Close Put spread for a loss, deploy new spread at the 10 delta mark).

Defense point to the upside: 2,475 (Close Credit Call spreads at a loss, close SPY long 249 Calls for gains and deploy new farther out of the money Credit Call spreads, at the new 10-delta mark).

RUT/IWM - Jul 1310/1320/1500/1510/134/151 Unbalanced Elephant

Net Credit: $1,417. Six weeks to expiration.

(Click on image to enlarge)

Defense lines: 1,370 to the downside (adjust the Credit Put spread to the new 10-delta strike price), 1,465 to the upside (close all the Call options for a loss, no adjustments, just keep riding the Credit PUT spreads side)

Defense lines: 1,370 to the downside (adjust the Credit Put spread to the new 10-delta strike price), 1,465 to the upside (close all the Call options for a loss, no adjustments, just keep riding the Credit PUT spreads side)

JUN SPX 2240/2250 Credit Put spread hedged with SPY 228 long Put

Net credit: $1042. The remainder of what originally was an Unbalanced Iron Condor. Looking great. Will expire this Friday for max profit.

JUL SPX 2250/2260/2490/2500 Unbalanced Iron Condor

hedged to the upside with SPY 249 Calls

6 weeks to expiration. With the addition of the hedge, the net credit and maximum profit potential decreased from $2,150 to $1,540. In exchange for that, we have a smoother risk curve to the upside and a higher defense line at SPX 2,475.

(Click on image to enlarge)

Defense point to the upside: 2,475 (Close Credit Call spreads at a loss, close SPY long 249 Calls for gains and deploy new farther out of the money Credit Call spreads, at the new 10-delta mark).

RUT/IWM - Jul 1310/1320/1500/1510/134/151 Unbalanced Elephant

Net Credit: $1,417. Six weeks to expiration.

(Click on image to enlarge)

Action Plan for the Week

- Let the June SPX Credit Put spreads expire for max.

- Close Call side of July SPX Unbalanced Iron Condor if SPX reaches 2,475. Also take the gains from the SPY 249 long Call hedges. Deploy new Credit Call spreads in the SPX 2,540 area, without doubling the number of contracts. Just playing the same number as in the original position, or if anything, just a couple more. To the downside, SPX 2,325 triggers a Credit Put spread adjustment and it would be down to the low SPX 2,100's.

- Adjust Put side of July RUT Unbalanced Elephant if the index falls down to 1,370. I'd be taking the 1320/1310 Credit Put spreads off the table at a loss and deploying new ones around 1,250 or lower (the presumed new 10-delta mark). To the upside, close all the Call options of the Elephant on a RUT trip to 1,465. No adjustments. The loss would be smaller than the Credit collected from the Put side. I believe RUT 1,465 will not be easily seen this week, but we have to lay out a plan anyways.

- As for new positions: nothing to add except if we reach an oversold scenario. I'd probably go with an SPX Credit Put spread in that case and if the strike prices at 10 deltas end up being within 1% distance form the existing Credit Put spreads that make up the July SPX Unbalanced Iron Condor, then I'd be deploying them in August expiration instead of July. Not seeing an oversold environment will simply keep us waiting until August regular expiration is 8 weeks away to establish our next position (currently 10 weeks away).

Forex

The long EURUSD position by the LT Trend Sniper system will finally be closed on Sunday at the open for a little less than a +3% return for the account.

More details about this robot here.

Sniper's results tracked here.

Economic Calendar

Tuesday: Europe Economic Sentiment. US PPI. China's Industrial Production.

Wednesday: US Core CPI. Retail Sales. FOMC Statement and Interest Rate decision.

Thursday: Philly Fed Index. Industrial Production.

Friday: Europe CPI. US Building Permits.

Trade with confidence my friends,

LT

If you are interested in a responsible and sustainable way of trading options for consistent income with solid risk management, consider acquiring LTOptions, my options trading system to the last detail.

Check out 2017 Track Record

Go to the bottom of this page in order to see the Legal Stuff

No comments:

Post a Comment