Recent Trading Activity

- Closed Call side of March SPX Unbalanced Iron Condor on Wednesday. Net loss $2,430. Deployed a May SPX 2520/2530 Credit Call spread, receiving a new $1,350 credit.

- Closed Call side of March SPX Unbalanced Iron Condor on Wednesday. Net loss $2,430. Deployed a May SPX 2520/2530 Credit Call spread, receiving a new $1,350 credit.

Market Conditions

(Click on image to enlarge)

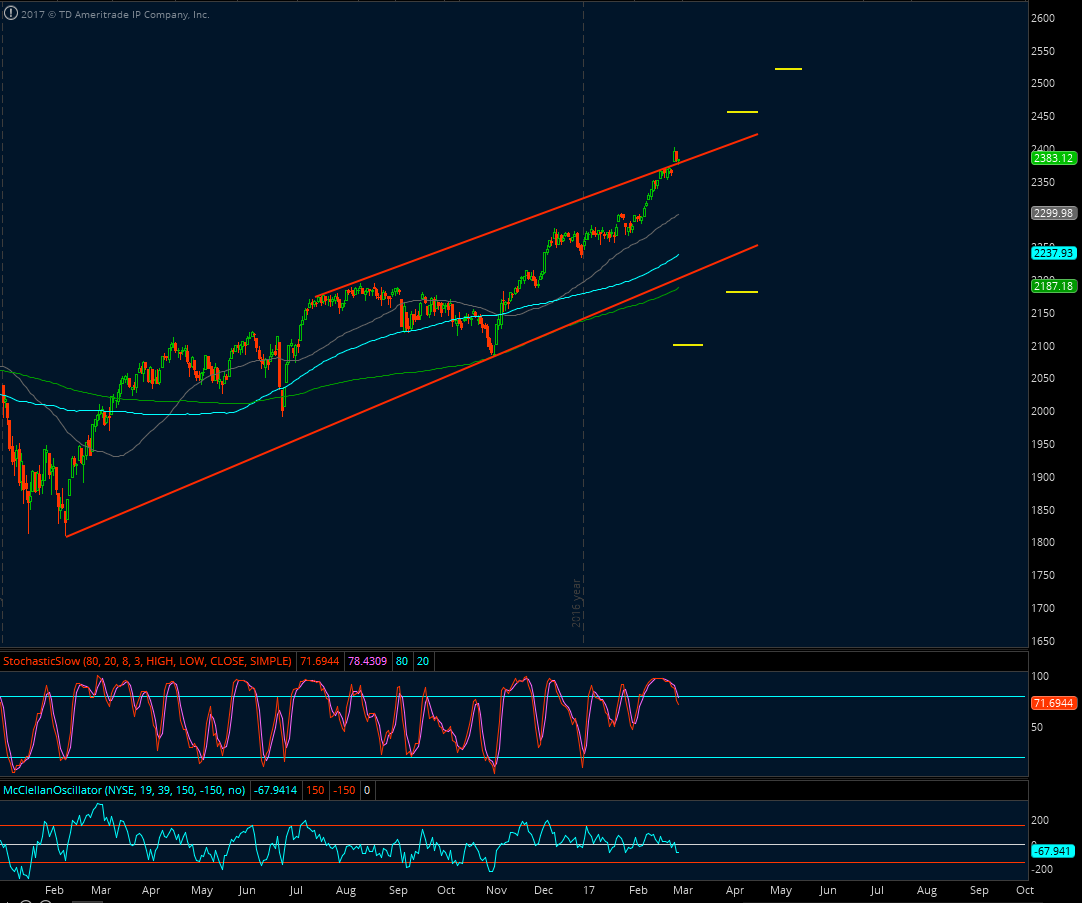

McClellan: -67 (neutral)

Stocks above their 20 DMA: 52% (neutral)

No man's land.

The S&P got to be 4.6% higher than its own 50-day average at some point on Wednesday. Such a distance is historically extreme for this index. What has been interesting about this rally, at least to me, is that the market has not achieved an overbought condition (as defined by my style anyways) throughout all this time. The McClellan oscillator has always stayed far from overbought territory. So, even in previous years where I'd allow myself to trade pure Credit Call spreads (and not just as part of Iron Condors or adjustments), I wouldn't have initiated any during all this time despite how far the rally has gone.

Just like in early December of last year, I now expect some sort of sideways action for a few days now. Of course, this is always based on historical market behavior, but it is nothing more than a probabilistic outcome. If there is some consolidation as I expect, that will facilitate the improvement of some positions via time decay. February was a challenging month and March didn't exactly start off on the right foot.

The Russell 2000:

(Click on image to enlarge)

Current Portfolio

MAR SPX 2090/2100 Credit Put spread hedged with SPY 214 Put

Max potential profit is $1,074. Two weeks to expiration and no concerns. This is a winner at this point with a market that is trading nearly 300 SPX points higher. I'll take it all the way to expiration.

MAY SPX 2520/2530 Credit Call spread

This is the adjustment to the Call side of the old March Iron Condor. I decided to go really far out in time to not over-pollute April expiration, where an SPX Credit Call spread existed. 9 deltas at the moment and chances are I will not be holding this one to expiration. I'm not overly concerned or anything at that level, but it is just a long wait until expiration.

MAR RUT/IWM 1235/1245/1450/1460/127/146 Unbalanced Elephant

$1,480 net credit. 2 weeks to expiration. Looking good now.

(Click on image to enlarge)

There is now a $1,100 gain here, roughly. The decision point on the Put side is now lower at 1,280 whereas on the Call side is a little higher (which is good) at 1,425. At that level I would take the Call side off at a small loss and just ride the Put side to compensate for it and end up with a winner overall in the end. It may be a good idea to consider taking the position off with these gains two weeks before expiration.

There is now a $1,100 gain here, roughly. The decision point on the Put side is now lower at 1,280 whereas on the Call side is a little higher (which is good) at 1,425. At that level I would take the Call side off at a small loss and just ride the Put side to compensate for it and end up with a winner overall in the end. It may be a good idea to consider taking the position off with these gains two weeks before expiration.

APR SPX 2175/2180/2455/2460 Unbalanced Iron Condor

$2,000 credit. 7 weeks to expiration. Put side comfortable at 6 deltas. Call side taking a little heat at 17 deltas.

(Click on image to enlarge)

MAR SPX 2090/2100 Credit Put spread hedged with SPY 214 Put

Max potential profit is $1,074. Two weeks to expiration and no concerns. This is a winner at this point with a market that is trading nearly 300 SPX points higher. I'll take it all the way to expiration.

MAY SPX 2520/2530 Credit Call spread

This is the adjustment to the Call side of the old March Iron Condor. I decided to go really far out in time to not over-pollute April expiration, where an SPX Credit Call spread existed. 9 deltas at the moment and chances are I will not be holding this one to expiration. I'm not overly concerned or anything at that level, but it is just a long wait until expiration.

MAR RUT/IWM 1235/1245/1450/1460/127/146 Unbalanced Elephant

$1,480 net credit. 2 weeks to expiration. Looking good now.

(Click on image to enlarge)

APR SPX 2175/2180/2455/2460 Unbalanced Iron Condor

$2,000 credit. 7 weeks to expiration. Put side comfortable at 6 deltas. Call side taking a little heat at 17 deltas.

(Click on image to enlarge)

Action Plan for the Week

- The March RUT Elephant. I'm thinking of taking it off the table for a $1,100 net gain or better. Nothing wrong with leaving it on since it will be a winner anyways (only that it can be a smaller winner if RUT gets past 1,425 now).

- The April SPX Unbalanced Iron Condor. If SPX reaches 2,415 this week, the 2455/2460 Call side will be adjusted up to 2510/2520 or something similar (2510/2515, or short Call at 2505).

- If I can get 50% of max gain from the May SPX 2520/2530 Credit Call spread or the April 2455/2460 Credit Call spread, I will be taking them off the table.

- In addition to this, I will be entering an April Unbalanced Lazy Elephant by the end of the week following the usual guidelines described here. Actually the addition of the position is another point reinforcing the idea of removing the March Elephant already as there is a lot of capital in use now that the March SPX Iron Condor adjustment was made using May options, it is extra margin consumed that was not being frozen before when both sides of the SPX Iron Condor were being played with March options. The only way this Elephant is not initiated is if we suddenly reach an oversold environment, in which case I would sell an April RUT Credit Put spread, but it is a scenario that which seems unlikely.

Economic Calendar

Tuesday: US Trade Balance

Wednesday: US Crude Oil Inventories. ADP Non-farm Employment change. China's CPI

Thursday: European Central Bank press conference

Friday: Non-farm Payrolls. Unemployment Rate

Good luck this week folks,

LT

If you are interested in a responsible and sustainable way of trading options for consistent income with solid risk management, consider acquiring LTOptions, my options trading system to the last detail.

Check out 2017 Track Record

Go to the bottom of this page in order to see the Legal Stuff

No comments:

Post a Comment