March expiration is finally in the past and although it wasn't what I wanted in terms of results, I can't say I did bad. Considering the low volatility and the cheap prices of options plus the fact that the market has been going up non stop, the only fact of surviving the month and not having a negative return is in my humble opinion quite an achievement. More importantly, I got to finally stop the bleeding of January + February.

The RUT 825/830/955/960 expired for full profit on Friday and so did the SPX 1445/1450 Bull Put Spread. The return in the model portfolio was +2.33% for the month of March before considering commissions costs.

Market Conditions

SPX went from 1551.15 to 1560.70 this week, for a small gain of +0.62%. Pretty in line with my analysis last week where I mentioned that the upside room should be limited and if we kept going up it would probably be less than +1%.

This is how the SPX index looks as of March 15, 2013.

(Click on image to enlarge)

The yellow horizontal lines represent the short strikes of current April positions. More on that later.

The yellow horizontal lines represent the short strikes of current April positions. More on that later.

Stochastics at 94 overbought

McClellan at -7, not overbought, showing plenty of upside

72.13% of stocks are above their 20 SMA

71.88% of stocks are above their 50 SMA

As it has been the norm lately, we are trading at the top of the range, with some overbought conditions, but still room for breadth on the upside. I think the same way as last week. There is limited upside room, and if we keep going up it should be in slow motion. This party will eventually be over. SPX is up +9.43% this year in 75 days so far. If it were to keep this pace it would be up +45.89% by year end which doesn't make much sense.

Positions and Action Plan

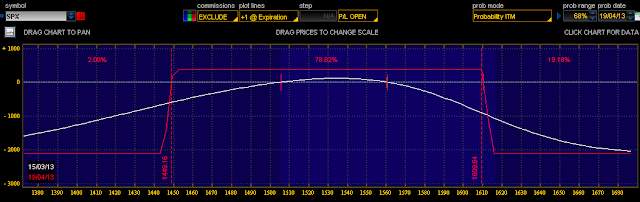

SPX 1445/1450/1610/1615 Iron Condor

(Click on image to enlarge)

78.82% probability of success. This one looks good so far, and I won't be touching it this week.

78.82% probability of success. This one looks good so far, and I won't be touching it this week.

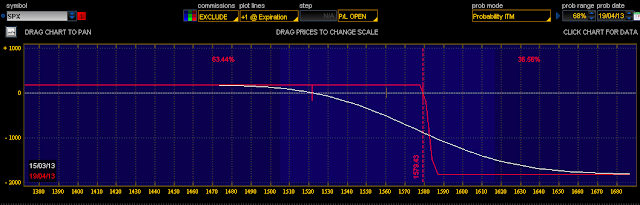

SPX 1580/1585 Bear Call Spread

(Click on image to enlarge)

With a 63.44% probability of success this one's getting some heat and might need special attention this week. I've been waiting for a retracement for a while in order to close this position for a small loss. I prefer that over an adjustment but the market just hasn't given any chance at all. At this point I'm considering a few ideas:

With a 63.44% probability of success this one's getting some heat and might need special attention this week. I've been waiting for a retracement for a while in order to close this position for a small loss. I prefer that over an adjustment but the market just hasn't given any chance at all. At this point I'm considering a few ideas:

1 - Roll to the 1610/1615 strikes (still in April expiration) and wait for a pull back to add a Bull Put spread around 1450/1445. The advantage is I could get a better premium in the Bull Put spread if the market pulls back, but obviously if it doesn't I will simply have lost the opportunity to make a few bucks on a Put side.

2 - Close the spread and open an April Iron Condor with strikes 1465/1470/1610/1615. The advantage is I get more credit up front but the downside risk doesn't look attractive. And 1470 now looks far, but with a small an normal 3% decline it will start too look very close and extremely nerve racking.

3 - Third option is close the spread and open an Iron Condor in May using strikes 1415/1420/1630/1635. The advantage is that there's way more downside room. The disadvantage is that it will take longer for time decay to play a roll here, and it will look like forever.

We'll see. I haven't made up my mind yet.

On a final note, I've made a decision about this trading exercise with the model portfolio and sharing trades with the world etc. If the model portfolio goes to a -20% draw-down for the year I will stop. Probably for a few months or maybe the rest of 2013 (doesn't mean I will stop blogging) It would be time to focus on learning all the lessons, re-design the strategy, do some serious back test of new ideas and then come back later, hopefully stronger. But it wouldn't make sense to keep doing the same thing over and over again without results.

If there's something I've learned this year is the fact that when implied volatility is low (Let's say VIX bellow 15) it is very difficult to make money by selling credit spreads and Iron Condors. Options' premiums are too low, returns on margin suck and the distance to your short strike prices is just too small if you want to obtain any decent return. You're set up for failure from the beginning.

The best lesson to me was on February 25. That day, SPX went down by almost 2%. Obviously the 1445/1450 March Put spread at that point was losing money as the market was going against it, that's fine. But here's the interesting part: you would expect the Call Spread (1560/1565) should be making a huge profit as the market was getting away from it. But that was not the case! the Call Spread was also losing money that day even though the market was now 30 points farther from it. All because of the VIX exploding and with it, all the options premiums go up, both calls and puts. And as a premium seller, you simply lose money if you sold small premiums which grow after that. So, in that particular day I learned more than in 2 years. Opening credit spreads or Iron Condors in periods of low volatility is almost a recipe for disaster. You can hardly ever make money regardless of where the market moves because chances are you will lose on both sides at the same time if the VIX suddenly spikes 3 or 5 points one day, something completely normal for the VIX to do. Credit Spreads and Iron Condors ARE NOT strategies to use all the time.

I hope this lesson is also valuable for someone out there.

Happy trading this week folks. Be well, and good luck! I'm off to Cuba in a few days so there won't be a Weekend Portfolio Analysis article next week.

Check out Track Record for 2013

The RUT 825/830/955/960 expired for full profit on Friday and so did the SPX 1445/1450 Bull Put Spread. The return in the model portfolio was +2.33% for the month of March before considering commissions costs.

Market Conditions

SPX went from 1551.15 to 1560.70 this week, for a small gain of +0.62%. Pretty in line with my analysis last week where I mentioned that the upside room should be limited and if we kept going up it would probably be less than +1%.

This is how the SPX index looks as of March 15, 2013.

(Click on image to enlarge)

Stochastics at 94 overbought

McClellan at -7, not overbought, showing plenty of upside

72.13% of stocks are above their 20 SMA

71.88% of stocks are above their 50 SMA

As it has been the norm lately, we are trading at the top of the range, with some overbought conditions, but still room for breadth on the upside. I think the same way as last week. There is limited upside room, and if we keep going up it should be in slow motion. This party will eventually be over. SPX is up +9.43% this year in 75 days so far. If it were to keep this pace it would be up +45.89% by year end which doesn't make much sense.

Positions and Action Plan

SPX 1445/1450/1610/1615 Iron Condor

(Click on image to enlarge)

SPX 1580/1585 Bear Call Spread

(Click on image to enlarge)

1 - Roll to the 1610/1615 strikes (still in April expiration) and wait for a pull back to add a Bull Put spread around 1450/1445. The advantage is I could get a better premium in the Bull Put spread if the market pulls back, but obviously if it doesn't I will simply have lost the opportunity to make a few bucks on a Put side.

2 - Close the spread and open an April Iron Condor with strikes 1465/1470/1610/1615. The advantage is I get more credit up front but the downside risk doesn't look attractive. And 1470 now looks far, but with a small an normal 3% decline it will start too look very close and extremely nerve racking.

3 - Third option is close the spread and open an Iron Condor in May using strikes 1415/1420/1630/1635. The advantage is that there's way more downside room. The disadvantage is that it will take longer for time decay to play a roll here, and it will look like forever.

We'll see. I haven't made up my mind yet.

On a final note, I've made a decision about this trading exercise with the model portfolio and sharing trades with the world etc. If the model portfolio goes to a -20% draw-down for the year I will stop. Probably for a few months or maybe the rest of 2013 (doesn't mean I will stop blogging) It would be time to focus on learning all the lessons, re-design the strategy, do some serious back test of new ideas and then come back later, hopefully stronger. But it wouldn't make sense to keep doing the same thing over and over again without results.

If there's something I've learned this year is the fact that when implied volatility is low (Let's say VIX bellow 15) it is very difficult to make money by selling credit spreads and Iron Condors. Options' premiums are too low, returns on margin suck and the distance to your short strike prices is just too small if you want to obtain any decent return. You're set up for failure from the beginning.

The best lesson to me was on February 25. That day, SPX went down by almost 2%. Obviously the 1445/1450 March Put spread at that point was losing money as the market was going against it, that's fine. But here's the interesting part: you would expect the Call Spread (1560/1565) should be making a huge profit as the market was getting away from it. But that was not the case! the Call Spread was also losing money that day even though the market was now 30 points farther from it. All because of the VIX exploding and with it, all the options premiums go up, both calls and puts. And as a premium seller, you simply lose money if you sold small premiums which grow after that. So, in that particular day I learned more than in 2 years. Opening credit spreads or Iron Condors in periods of low volatility is almost a recipe for disaster. You can hardly ever make money regardless of where the market moves because chances are you will lose on both sides at the same time if the VIX suddenly spikes 3 or 5 points one day, something completely normal for the VIX to do. Credit Spreads and Iron Condors ARE NOT strategies to use all the time.

I hope this lesson is also valuable for someone out there.

Happy trading this week folks. Be well, and good luck! I'm off to Cuba in a few days so there won't be a Weekend Portfolio Analysis article next week.

Check out Track Record for 2013

Go to the bottom of this page in order to see the Legal Stuff

No comments:

Post a Comment