This is an interesting occurrence that you might not know of when/if you are new to trading vertical spreads and that you can use to your advantage to gain a few extra dollars here and there.

In my paper-trading venture I had decided to only trade Out of the Money Credit spreads. That is, when I believe the markets are close to overbought I sell and Out of the Money Call option and buy a farther Out of the Money Call option to reduce the unlimited risk. Likewise, when the markets seem oversold to me, I sell an Out of the Money Put option combined with the purchase of a farther Out of the Money Put for protection.

However, using the technique I'm going to describe I could potentially use a Debit Spread instead of a Credit Spread in some of my plays, and keep the same bias, a similar profit picture, less margin frozen by my broker and potentially a higher Maximum Return from time to time. Let's analyze with real numbers and positions.

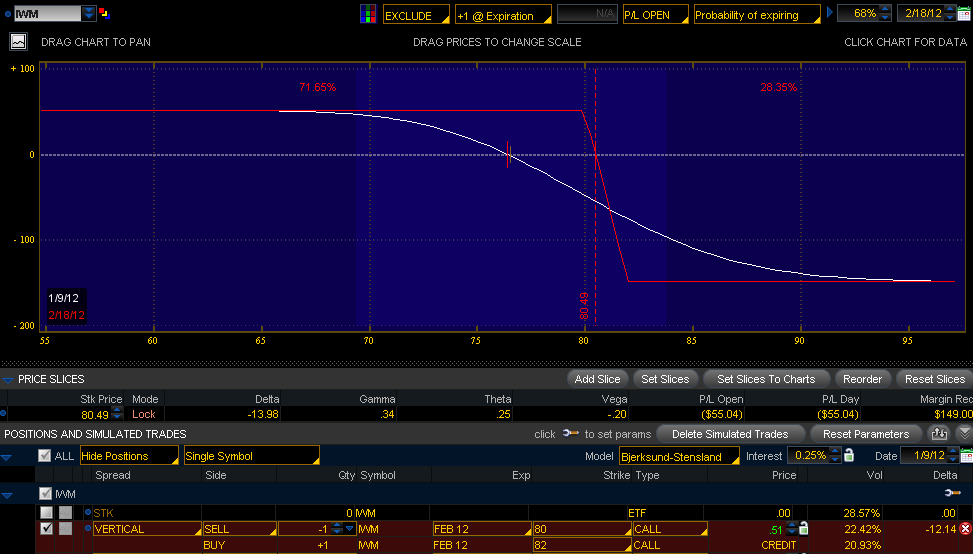

Let's say on January 11, 2012 I thought the markets were overbought and I wanted to place a bet that the IWM Etf wouldn't keep moving up. IWM ended the day at 76.57. Let's say I sold a February 80 Call, betting that IWM wouldn't go above 80, and at the same time let us assume I bought the 82 strike Call for protection. That's a Credit Transaction, more specifically a Bear Call Credit Spread. It could have been opened for a 0.51 credit. And the profit picture would have resulted something like this:

(Click on image to enlarge)

SELL 1 IWM February 80 Call (@0.95)

BUY 1 IWM February 82 Call (@0.44)

----------------------------------

Maximum Potential return = $51 (Credit received when opening the position)

Maximum Risk = $149

Given that the credit received is $51 dollars, the risk is $149 (2 points of distance between strike prices multiplied by 100 = 200. Minus 51 of credit = 149 max risk).

Now, here is the key, the same position, with the same bias and the same idea behind (IWM won't go above 80) can be obtained if instead of a Credit Call Spread you use a Debit Put Spread with the same strike prices 80 and 82. In other words you can Buy the 82 strike Put, betting that IWM will go down, and at the same time Sell an 80 strike Put to partially finance the purchase of the 82 strike Put, resulting in a debit transaction as follows:

(Click on image to enlarge)

SELL 1 IWM February 80 Put (@4.49)

BUY 1 IWM February 82 Put (@5.94)

----------------------------------

Maximum Potential return = $55

Maximum Risk = $145 (Debit invested when opening the position)

As you can see, both positions reflect the same bias (bearish) and the same plan: The idea that IWM won't move over the 80 price level. They both have a similar profit picture/curve except that, in this case, the Put Debit Spread is returning potentially 4 more dollars while at the same time reduces the maximum risk by 4 dollars. Isn't that cool? And this is only using one contract! It could represent $40 dollars more in profit on a 10 contract position. No need to do the maths, the savings can be huge overtime getting a few more dollars in profit here and there! As an example of this technique see my RUT trade on January 20, 2012 where I decided to use the debit Put Spread instead of the typical Credit Call spread.

Summing up

Every Credit Spread can be substituted with a corresponding Debit Spread using the same strike prices. This results in the same profit curve which occasionally yields more profit while risk is reduced. Also, every Debit Spread can be played with a Credit Spread. The beauty of this is that you, as a trader, can choose either one in order to trade your same idea/bias.

From now on, whenever you are about to open either a Credit or a Debit Spread, take a few seconds, look at the corresponding Debit or Credit Spread to see if you can obtain a few more dollars of profit and reduce your maximum risk by a few dollars at the same time! It doesn't hurt.

I hope you enjoyed this tip and I hope it becomes useful in your trading.

In my paper-trading venture I had decided to only trade Out of the Money Credit spreads. That is, when I believe the markets are close to overbought I sell and Out of the Money Call option and buy a farther Out of the Money Call option to reduce the unlimited risk. Likewise, when the markets seem oversold to me, I sell an Out of the Money Put option combined with the purchase of a farther Out of the Money Put for protection.

However, using the technique I'm going to describe I could potentially use a Debit Spread instead of a Credit Spread in some of my plays, and keep the same bias, a similar profit picture, less margin frozen by my broker and potentially a higher Maximum Return from time to time. Let's analyze with real numbers and positions.

Let's say on January 11, 2012 I thought the markets were overbought and I wanted to place a bet that the IWM Etf wouldn't keep moving up. IWM ended the day at 76.57. Let's say I sold a February 80 Call, betting that IWM wouldn't go above 80, and at the same time let us assume I bought the 82 strike Call for protection. That's a Credit Transaction, more specifically a Bear Call Credit Spread. It could have been opened for a 0.51 credit. And the profit picture would have resulted something like this:

(Click on image to enlarge)

SELL 1 IWM February 80 Call (@0.95)

BUY 1 IWM February 82 Call (@0.44)

----------------------------------

Maximum Potential return = $51 (Credit received when opening the position)

Maximum Risk = $149

Given that the credit received is $51 dollars, the risk is $149 (2 points of distance between strike prices multiplied by 100 = 200. Minus 51 of credit = 149 max risk).

Now, here is the key, the same position, with the same bias and the same idea behind (IWM won't go above 80) can be obtained if instead of a Credit Call Spread you use a Debit Put Spread with the same strike prices 80 and 82. In other words you can Buy the 82 strike Put, betting that IWM will go down, and at the same time Sell an 80 strike Put to partially finance the purchase of the 82 strike Put, resulting in a debit transaction as follows:

(Click on image to enlarge)

SELL 1 IWM February 80 Put (@4.49)

BUY 1 IWM February 82 Put (@5.94)

----------------------------------

Maximum Potential return = $55

Maximum Risk = $145 (Debit invested when opening the position)

As you can see, both positions reflect the same bias (bearish) and the same plan: The idea that IWM won't move over the 80 price level. They both have a similar profit picture/curve except that, in this case, the Put Debit Spread is returning potentially 4 more dollars while at the same time reduces the maximum risk by 4 dollars. Isn't that cool? And this is only using one contract! It could represent $40 dollars more in profit on a 10 contract position. No need to do the maths, the savings can be huge overtime getting a few more dollars in profit here and there! As an example of this technique see my RUT trade on January 20, 2012 where I decided to use the debit Put Spread instead of the typical Credit Call spread.

Summing up

Every Credit Spread can be substituted with a corresponding Debit Spread using the same strike prices. This results in the same profit curve which occasionally yields more profit while risk is reduced. Also, every Debit Spread can be played with a Credit Spread. The beauty of this is that you, as a trader, can choose either one in order to trade your same idea/bias.

From now on, whenever you are about to open either a Credit or a Debit Spread, take a few seconds, look at the corresponding Debit or Credit Spread to see if you can obtain a few more dollars of profit and reduce your maximum risk by a few dollars at the same time! It doesn't hurt.

I hope you enjoyed this tip and I hope it becomes useful in your trading.

Go to the bottom of this page in order to see the Legal Stuff

No comments:

Post a Comment