Recent Trading Activity

- Closed SPX June 2050/2025 Credit Put spread on Tuesday morning for a $1000 gain.

- Closed SPX June 2050/2025 Credit Put spread on Tuesday morning for a $1000 gain.

Market Conditions

(Click on image to enlarge)

McClellan: -7 (Neutral. Down from +103)

Stocks above their 20 DMA: 49% (Neutral. Down from 53%)

No man's land.

The upper red diagonal line seems to be behaving like resistance again, and for this reason it's staying on my chart for now, even though. as you know it was penetrated during that blow off top at the beginning of the year. The SPX is now close to 2% below its 50-day average, plenty of upside room until the 2780-2800 zone. We're seeing a pretty volatile market, that just can't seem to hold onto its gains for too long. How times change. To the downside, I think the previous lows around 2540 in early February are unlikely to be taken. So, that's my range, above 2800 and below 2540 should be decent areas to deploy credit spreads.

VIX almost at 20 now, combined with a no man's land territory is a good time for deploying Iron Condors and/or Elephants. Which I intend to do this week.

The Russell Index:

(Click on image to enlarge)

Current Portfolio:

The SPY Calls and SVXY Calls expire in December and January of next year. Same as the Synthetic stock position, which is equivalent to being long 200 shares of SPY, but needing much less buying power. The goal with all of them is to hold them for as long as possible. They may fail, of course, but they are calculated risks. All the SPY and SVXY Calls barely add up to seven thousand dollars. Or 7% of the original 100K portfolio.

The SPY Calls and SVXY Calls expire in December and January of next year. Same as the Synthetic stock position, which is equivalent to being long 200 shares of SPY, but needing much less buying power. The goal with all of them is to hold them for as long as possible. They may fail, of course, but they are calculated risks. All the SPY and SVXY Calls barely add up to seven thousand dollars. Or 7% of the original 100K portfolio.

The synthetic SPY stock position occupies decent room (13.8K), but since it is the same as being long stocks, there is no way to lose all that money. For example if SPX finishes the year at 2500 (SPY 250), it would be a 14 point loss (from artificially long stock at 264). So, 14 points multiplied by 200 synthetic shares would be a $2800 loss. A similar calculation can be done assuming SPY finishes the year at 240, 230 etc.

Something unexpected happened this week when ProShares (the provider of SVXY) decided to, out of the blue and without previous warning, cut the target daily move goal of the instrument in half. More details here. By reducing the daily move of SVXY they are providing investors a "smoother" ride with less wild swings. However, options traders got totally screwed. The expected move is automatically reduced, and therefore the deltas (or probabilities of any Out of the Money strike to eventually be In the Money drastically) decreased, evaporating the premium of the options contracts.

Losing money when I make bad trade decisions is one thing.

Losing when the nature of an instrument provided by an institution is changed, that gets me mad and frustrated.

In my opinion it is highly unethical. They should have created a separate instrument to provide the 0.5x behaviour. Instead they altered the existing one, and hundreds of investors get screwed, mainly those trading options as the implied move is now much smaller. Surprisingly the regulators approved this change !

For me, it is a painful lesson to never ever again invest in absolutely any product created by ProShares.

Let's now look at the income plays.

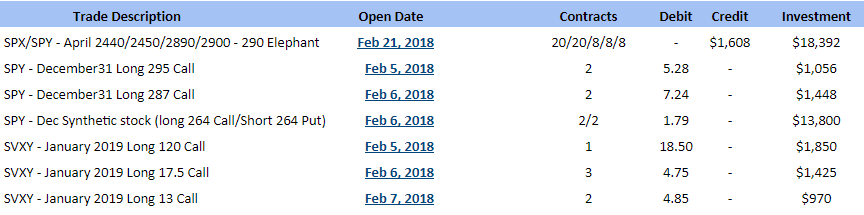

Apr. SPX/SPY 2440/2450/2890/2900 - 290 Elephant

Net Credit: $1,608 and eight weeks to expiration(Click on image to enlarge)

Defense line: 2550 (adjust the Put side). 2830 on the Call side (close for a small loss. Keep riding Put side, whose credit is greater than whatever loss the Call side suffers.

Defense line: 2550 (adjust the Put side). 2830 on the Call side (close for a small loss. Keep riding Put side, whose credit is greater than whatever loss the Call side suffers.

The synthetic SPY stock position occupies decent room (13.8K), but since it is the same as being long stocks, there is no way to lose all that money. For example if SPX finishes the year at 2500 (SPY 250), it would be a 14 point loss (from artificially long stock at 264). So, 14 points multiplied by 200 synthetic shares would be a $2800 loss. A similar calculation can be done assuming SPY finishes the year at 240, 230 etc.

Something unexpected happened this week when ProShares (the provider of SVXY) decided to, out of the blue and without previous warning, cut the target daily move goal of the instrument in half. More details here. By reducing the daily move of SVXY they are providing investors a "smoother" ride with less wild swings. However, options traders got totally screwed. The expected move is automatically reduced, and therefore the deltas (or probabilities of any Out of the Money strike to eventually be In the Money drastically) decreased, evaporating the premium of the options contracts.

Losing money when I make bad trade decisions is one thing.

Losing when the nature of an instrument provided by an institution is changed, that gets me mad and frustrated.

In my opinion it is highly unethical. They should have created a separate instrument to provide the 0.5x behaviour. Instead they altered the existing one, and hundreds of investors get screwed, mainly those trading options as the implied move is now much smaller. Surprisingly the regulators approved this change !

For me, it is a painful lesson to never ever again invest in absolutely any product created by ProShares.

Let's now look at the income plays.

Apr. SPX/SPY 2440/2450/2890/2900 - 290 Elephant

Net Credit: $1,608 and eight weeks to expiration(Click on image to enlarge)

Action Plan for the Week

1- My plan is to deploy a RUT position using April options. If we reach an oversold condition throughout the week, then I will go with a Credit Put spread. If we stay in no man's land, I will go with an Elephant as it suffers much less on the Call side and with RUT being below its 50-day average I feel the Call side will be more likely to be threatened. So, instead of an Iron Condor, Elephant again.

Economic Calendar

A little heavy this week.

Monday: ISM Non-Manufacturing PMI.

Tuesday: A couple of FOMC members speak.

Wednesday: Europe GDP. US ADP Non-Farm Employment change.

Thursday: European Central Bank press conference. China's CPI and PPI.

Friday: US Non-Farm Payrolls. Unemployment Rate.

Good luck this week my friends.

LT

If you are interested in a responsible and sustainable way of trading options for consistent income with solid risk management, consider acquiring LTOptions, my options trading system to the last detail.

Check out 2018 Track Record

Go to the bottom of this page in order to see the Legal Stuff

No comments:

Post a Comment