Recent Trading Activity

- Put side of May RUT Elephant expired for max profit of $1,092

- Tried to close the 2465/2475 Call side of the June SPX Unbalanced Iron Condor, but didn't get filled. I tried 0.10 debit, then 0.15 then 0.20 as the market kept rebounding until I stopped trying on Friday.

- Put side of May RUT Elephant expired for max profit of $1,092

- Tried to close the 2465/2475 Call side of the June SPX Unbalanced Iron Condor, but didn't get filled. I tried 0.10 debit, then 0.15 then 0.20 as the market kept rebounding until I stopped trying on Friday.

Market Conditions

(Click on image to enlarge)

McClellan: -16 (Neutral. Up from -68 last week)

Stocks above their 20 DMA: 38% (Neutral. Down from 44% last week)

No man's land.

We finally saw a decent down day, but lately it looks like the market is totally peaceful for 2 or 3 months, then we get these VIX spikes of one or two days only to go back to usual right after. We're currently closer to a short-term oversold extreme than to an overbought one. But with the rebound under way, we may not see the oversold condition that we were waiting. With the down day on Wednesday, I would have guessed we'd see at least another down day, if only a small one, but nop. Straight back up. The good thing is that none of the existing positions suffered any damage and the portfolio is now up almost 7% for the year.

The same horizontal channel (2320 - 2400) remains in play for SPX. The first July position will be initiated later this upcoming week, and if the index stays in No man's land condition, we'll proceed as usual with an Unbalanced Iron Condor, or Elephant if the index stays too close to its 50-day avg (less than 1% higher than it).

Let's take a look at the Russell (below its 50-day avg), which is looking a little weaker than the SPX (above its 50 day avg)

The Russell 2000:

(Click on image to enlarge)

Current Portfolio

JUN RUT 1220/1230 Credit Put spread hedged with IWM 126 Long Puts

Net credit: $1130. Four weeks to expiration. This is the Put side of what used to be a Lazy Elephant. Only 5 deltas, all good here.

Adjustment point stays the same at 1,275.

Adjustment point stays the same at 1,275.

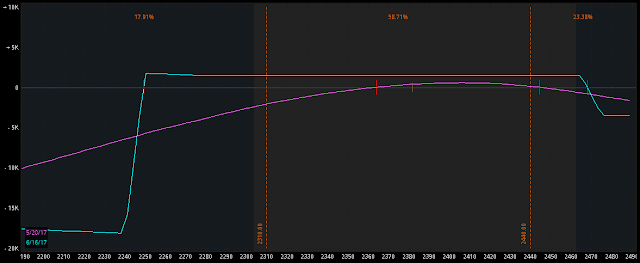

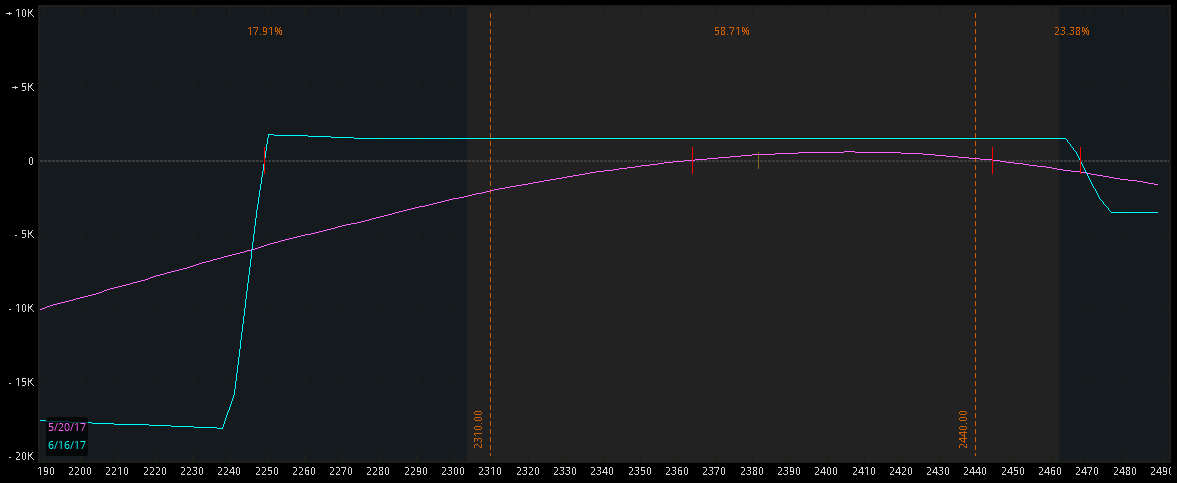

JUN SPX 2240/2250/2465/2475 Unbalanced Iron Condor with SPY 228 long Put

Net credit: $1447. Four weeks to expiration. All good here: 3 deltas on the Call side, 9 deltas on the Put side.

The 4 to 1 ratio of Puts to Calls Unbalanced Iron Condor is not looking bad at all in the above picture. I intended to close the Call side early for gains to open the possibility of redeploying at the same strikes on a market rebound. The mid price of that Call spread (2465/2475) is 0.175. It was initially sold at 0.81 and we have 5 of them, so the open gain at the moment there is $318. I'd be fine with those gains, but then SPX would need to rally to about 2,410 in order to redeploy this same spread for a similar credit. I'll see if the market makers give me the fill this time. I won't close for more than 0.20 debit. So, if the fill is not possible I'll just keep holding it. Adjustment points for the week are SPX 2,310 and SPX 2,440. On the Call side we can wait until SPX 2,455 given how small it is and move it up to SPX 2,500 if an adjustment is necessary, which is my plan with this position.

The 4 to 1 ratio of Puts to Calls Unbalanced Iron Condor is not looking bad at all in the above picture. I intended to close the Call side early for gains to open the possibility of redeploying at the same strikes on a market rebound. The mid price of that Call spread (2465/2475) is 0.175. It was initially sold at 0.81 and we have 5 of them, so the open gain at the moment there is $318. I'd be fine with those gains, but then SPX would need to rally to about 2,410 in order to redeploy this same spread for a similar credit. I'll see if the market makers give me the fill this time. I won't close for more than 0.20 debit. So, if the fill is not possible I'll just keep holding it. Adjustment points for the week are SPX 2,310 and SPX 2,440. On the Call side we can wait until SPX 2,455 given how small it is and move it up to SPX 2,500 if an adjustment is necessary, which is my plan with this position.

JUN RUT 1220/1230 Credit Put spread hedged with IWM 126 Long Puts

Net credit: $1130. Four weeks to expiration. This is the Put side of what used to be a Lazy Elephant. Only 5 deltas, all good here.

JUN SPX 2240/2250/2465/2475 Unbalanced Iron Condor with SPY 228 long Put

Net credit: $1447. Four weeks to expiration. All good here: 3 deltas on the Call side, 9 deltas on the Put side.

Action Plan for the Week

- Defend the June RUT Credit Put spread if RUT falls to 1,275. Unlikely given how far from that RUT is. With RUT at 1,367 that would be a 6.7% fall in a week.

- Take Call side of the June SPX Unbalanced IC off at 0.20 debit or better.....if the market makers want to fill the order. Re-establish the same Credit Call spread on an SPX rally to 2,410. I'll try to close it on Monday, if I'm unable to, then I think I'll just hold it closer to expiration and forget about the idea of the redeployment. Defend Put side of this same position at SPX 2310, by closing it for a loss and redeploying at the new 10 delta level.

- Upon reaching an oversold extreme, initiate a July RUT Credit Put spread position at the 10 delta level in the July monthly expiration cycle.

- If no oversold condition is reached during the week, then on Friday, establish the first July expiration position. I'll go with the instrument that is less weak, the one that is higher than its 50-day average by a greater %. Currently that is the SPX index. Once the symbol is decided, I will look at whether to trade an Unbalanced Iron Condor (SPX price higher than its 50-day average by more than 1% [23 points or so], or an Unbalanced Lazy Elephant is SPX price is not 1% higher than its own 50-day average. I would go, as usual, with 10 deltas on each side. In the case of the Elephant, always following these guidelines to decide how many Calls vs Puts.

Forex

The EURUSD rebounded and the LT Trend Sniper system got back in. SL has been already moved three times and it is almost at the break even level.

Sniper's results tracked here.

Economic Calendar

Monday: Canadian Markets closed. US Markets open. No special economical releases.

Tuesday: German GDP. Europe Business Climate Index. US New Home Sales.

Wednesday: US Existing Home Sales. FOMC Meeting Minutes.

Friday: US Core Durable Goods Orders and GDP.

Take it easy, but take it like a champ,

LT

If you are interested in a responsible and sustainable way of trading options for consistent income with solid risk management, consider acquiring LTOptions, my options trading system to the last detail.

Check out 2017 Track Record

Go to the bottom of this page in order to see the Legal Stuff

No comments:

Post a Comment