In light of recent events, not that Pokémon fad, but actual market price action of recent months, I feel like I've been taken to an obscure hole... filled with frustration. It is clear that no single trading strategy can perform well under any market condition, but lately, especially lately, it has looked like selling Call options has been deemed the ultimate sin by the Options Gods.

The market has been doing the seemingly impossible over and over again. It looks like every short position you put on, is being looked at by a powerful force from the shadows, waiting to punish you mercilessly EVERY SINGLE TIME. Of course, at one point confidence starts to become a factor and you start second guessing your abilities: afraid to pull the trigger every time before entering a new position, as you can't totally get away from recent sour experiences. The repeated pain is just too fresh in your memory.

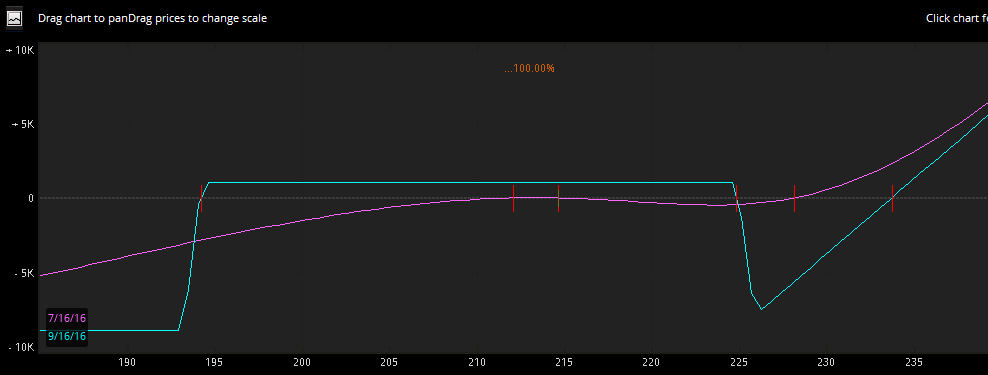

Just the other day the 2175/2185 July Call spread was showing 1 delta. That was June 27. One delta: a 1% probability, or 99% chance in my favor as the seller. Yet, I had to close it for a loss one day before expiration due to the danger of a gap up overnight. It hasn't been my worst loss. Far from it. But it was certainly the most frustrating one as it makes you feel raped by the illusion of probabilities.

A 1 delta Call should bother you 1% of the time, or once in a hundred times. And because I trade usually only one Iron Condor per month, the "hundred times" would be one hundred months, or more than 8 years! A Call that you are short and reaches 1 delta, should back fire only once every 8 years. But that my friends, is total BS! Probabilities are not probabilities anymore.

In the past 3 years this super comfortable 1 delta calls have back fired against me 3 or 4 times. Way more than those probabilities would indicate. Way more than once in eight years. This leads me to question the validity of selling Calls at all.

I haven't completely stopped trading Calls because, year after year, even though less profitably than Puts, I have made money from them. Aware and recognizing the greater challenge they represent, I have argued for a long time that the Call side is the real danger. People are always afraid of a crash. You know, the major calamity that takes place 3 times in a century, when the real danger takes place way more frequently and it is to the upside. We all know probabilities are exaggerated to the downside, but we tend to believe they are fairly well estimated to the upside. I don't think so anymore. I think probabilities are constantly underestimated to the upside and those Call options are frequently under-priced. Academicians can start killing me now.

Not so long ago I decided to start trading Unbalanced Iron Condors. Despite some profits lost here and there due to collecting less credit, it was a wise decision that has allowed me to totally mitigate major damage to my capital. Even in this super challenging year for a non-directional trader, the account has never been down more than 3%. So that's good, and it is an evolution I wouldn't have made if I hadn't constantly questioned my approach looking for improvements. Well, this is one of those moments where new revisions and improvements are mandatory.

For the rest of the year my trading activity will slightly change as follows:

- Take profits earlier on the Call side (2 or 1 deltas no matter what). This is obviously, more necessary if the Iron Condor is a traditional fully balanced one.

- I have considered waiting longer to initiate Credit Call spread positions. For example, a greater value in the McClellan Oscillator or a greater value in the number of stocks above their 20 Day Moving Average, or both conditions combined. This will obviously lead to fewer opportunities, but likely clearer ones where the market reversal is more imminent. I may consider waiting for McClellan at/above +200, and 80% of stocks above their 20 DMA, or +175 and 75%. It's just an idea I'm toying with.

- Delay adjustments on the Call side without necessarily incurring more losses, by applying this technique I used on April 4 of this year that flattens the T+0 line to a great degree, making positions less susceptible to delta and gamma variations.

- Invest more via an additional RUT position every month. Given the fact that I tend to be under-invested, and that I still want to make this year count, I have thought of adding both the typical SPX position and also a RUT one with less capital every month. I am on average 40% invested. I can easily bump that up to 60%, looking to obtain better account returns during the second half of the year.

- Start trading a new variation of Iron Condors where the number of short Calls on the Credit Call spread side is smaller than the number of Long Calls in the spread. For example, instead of a 10/10/10/10 contracts Iron Condor, it would be 10/10/9/10:

10 long Puts

10 short Puts

9 short Calls

10 long Calls

or

10 long Puts

10 short Puts

10 short Calls

12 long Calls

The point is: fewer short Calls than long Calls.

The more I study this idea, the more I fall in love with it.

Depending on your strikes and number of contracts you can still get acceptable credit vs capital at risk and the T+0 line is pretty flat to the upside. I have searched for this variation on the Internet and I've found nobody talking about this. Who knows? I may be introducing a novelty after all. If so, it will deserve to be properly baptized, including a special nickname and everything.

So, to start experimenting with this variation, I will choose the additional RUT position mentioned in the previous point. That will be the initial battle ground. LTOptions members have already received a new package describing all my thoughts about this type of position, Pros and Cons, plus all the details on how to manage these type of position.

Conclusions

It is clear, more than ever, that no single strategy can deliver alpha and perfectly fit every market condition. However, it is our duty, if we want to grow as traders, to constantly question our approach and be open-minded. The less ego, the more openness, the better equipped you will eventually become. I'll be more active managing the winning Bear Call spreads, and will delay adjusting them without incurring larger losses.

More capital will be used with an additional RUT trade per month where I will be experimenting with a different type of Iron Condors which may deserve a new name for easier identification.

As always, thanks for dropping by,

LT

Go to the bottom of this page in order to see the Legal Stuff

No comments:

Post a Comment