No Weekend Portfolio Analysis for today. Instead, I'm going to do something different as I think a trader should go back to the drawing board from time to time, revise what he's been doing, learn, improve.

Here's a breakdown of my trading activity by strategy. I separated the results of Iron Condors, individual Credit Put spreads and individual Credit Call spreads for the last 12 months of trading activity: from December 2013 to November 2014.

An Iron Condor position to me is not only the initial trade. To me, if I made an adjustment to one of the sides, that adjustment is part of the Iron Condor trade management. So, on the below table some individual credit spreads are included which served as adjustments (reflected in the Notes column). Logically these individual credit spreads are not reflected in the Credit spreads tables later on.

Not bad at all. Iron Condors have been responsible for 13.53% of the returns before commissions for a $10,000 model portfolio.

Not bad at all. Iron Condors have been responsible for 13.53% of the returns before commissions for a $10,000 model portfolio.

In particular the April RUT 1020/1030/1245/1255 was misplayed. When the Call side was threatened, instead of just adjusting as usual, closing the Calls and selling farther out of the money Calls, I truly believed the market was never again going to come down, so I sold Puts as well. That's why I closed that entire Iron Condor and opened an entirely new one 1080/1090/1280/1290, whose Put side was quickly threatened. That was a stupid move. I never adjust that way and never should, especially in an overbought market. Had I adjusted as usual, just selling the 1280/1290 Credit Call spread, then the loss on the Iron Condor would have only been -420 + 300 = -120. The return for the Iron Condor strategy would have been $1563, or more than 15% for the model portfolio.

My Iron Condors have an 80% probability of success at entry. Each side has a 10% probability of expiring in the money when the trade is entered. However, I make adjustments as soon as one side hits 30% probability. This means that if I have room before the 30% probability is hit on the Put side plus room before the 30% number is hit on the Call side, the real room for the market to move without me having to make any adjustment at all is 40% of the spectrum in the middle of the Iron Condor (30% + 40% + 30%). Lo and behold, 5 out of 12 Iron Condors did not need to be touched at all which is 41.5% of the Iron Condors played. Scary how those probability numbers work.

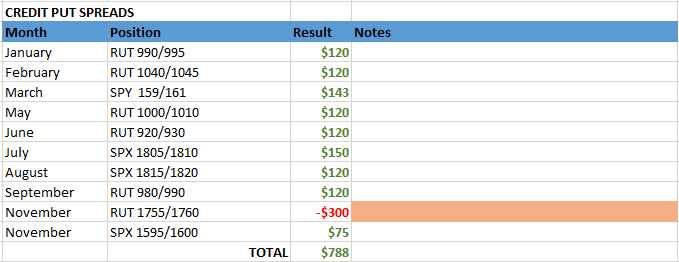

The Credit Put spread strategy has been really good. Responsible for 7.88% return on the model portfolio before commissions. Playing at the 10% probability ITM, you would expect 90% winners. That's exactly what I got, 9 winners out of 10 trades. The reason I'm profitable is simply because I don't let the losers turn into full losers. Plain and simple. To me this means that defending trades is something worth doing.

The Credit Put spread strategy has been really good. Responsible for 7.88% return on the model portfolio before commissions. Playing at the 10% probability ITM, you would expect 90% winners. That's exactly what I got, 9 winners out of 10 trades. The reason I'm profitable is simply because I don't let the losers turn into full losers. Plain and simple. To me this means that defending trades is something worth doing.

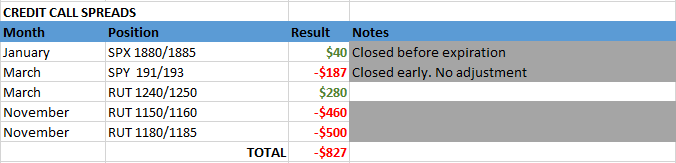

Individual Credit Call spreads are the problem. What is really interesting is that these results are pretty consistent with my 2012 and 2013 activity. I'm not just complaining about the most recent rally. In fact, by mid-October when SPX was around 1820, the markets were -1.5% for the year. A negative year and yet, up to that point I had been more tested on the Call side than on the Puts when considering both Iron Condors and Individual Credit spreads in what had been a negative year to date. So, I'm not just talking about the most recent rally of the last two weeks. I'm talking about three years of being tested on the Call side way more frequently than what probability models suggest. Why the hell do Credit Call spreads get tested more frequently than they should if it's purely a probabilities game?

Individual Credit Call spreads are the problem. What is really interesting is that these results are pretty consistent with my 2012 and 2013 activity. I'm not just complaining about the most recent rally. In fact, by mid-October when SPX was around 1820, the markets were -1.5% for the year. A negative year and yet, up to that point I had been more tested on the Call side than on the Puts when considering both Iron Condors and Individual Credit spreads in what had been a negative year to date. So, I'm not just talking about the most recent rally of the last two weeks. I'm talking about three years of being tested on the Call side way more frequently than what probability models suggest. Why the hell do Credit Call spreads get tested more frequently than they should if it's purely a probabilities game?

To me this only has one explanation and I know this could be a bit controversial, but criticizing without offering real solutions adds no value to me. So here it goes: The probability models on the TOS platform DO consistently underestimate upside moves in the markets. There, I said it.

Even assuming I'm wrong, and that probability models on the ThinkOrSwim platform reflect correct numbers for Out of the Money Calls, the simple fact that volatility decreases on the way up making adjustments unbelievably unattractive implies that something must be done differently when trading Calls in this life if you want to be more profitable in the long run.

On the way down, volatility expands and it is not uncommon to be able to place your adjustments 10% - 15% below the market. Meaning, if you sold Puts during an oversold environment, the market had already corrected probably 5% - 10%. If you are tested and place the adjustment 10% below the original point, you are now challenging the market to a total 20% or 25% fall. So, even though we fear a market crash every day, they are very infrequent. 4 times since 1950 (1974, 1987, 2000, 2008). Even in those instances, after two adjustments on the Put side you would probably be OK. Three adjustments on the Put side would Put you really far below and with a very very high probability of surviving a severe market crash. So, folks, Credit Spread traders of the world! Unite! The danger is on the Call side. Stop the obsession with market crashes. Your real hidden enemy is the upside where your adjustments are barely 2% - 3% above and the market can keep fucking you at will indefinitely.

How to neutralize this issue?

Once you jump to a conclusion you have to design a plan of attack. Otherwise this would just be a futile exercise. There is a problem. To me it is clear it exists. Now, how do we deal with it?

Option 1. Stop selling Calls altogether

This could be your way out. Frankly, it is not my favorite and I won't do this. I enjoy playing Iron Condors and they have a Call side. Iron Condors allow me to mitigate losses in the case of Call side adjustments and I don't suffer that much with them. So, I won't stop selling Calls altogether.

Option 2. Sell smaller Credit Call spread positions

This could be a very viable alternative. What do I mean by this?

It's very simple.

Instead of using your typical portfolio allocation per position, you cut it in half for the Calls. This is applied to both Individual Credit Call spreads and Iron Condors, which would turn into Unbalanced Iron Condors. In the case of an adjustment, you go to your normal position. For example:

Right now I would normally sell the 2110/2120 SPX December Credit Call spread. I would sell 2 contracts. The credit is 1.00 per contract which is typical for a 10% probability ITM 10 point wide Credit Call spread. My risk would be 9.00 or $1800 in dollar terms. This spread would be worth 3.50 at the 30% probability level.

Sell 2 SPX December 2110/2120 Credit Call spread.

Credit: 1.00

Max risk: 9.00

If the spread is threatened, I pay 3.50 debit * 2 = $700 to close it. And deploy a new spread further up for another 1.00 credit. Assuming the adjustment wins: 1.00 credit - 3.50 debit + 1.00 credit = -1.50 or a $300 loss.

Instead of the above scenario, I would start playing just one contract and if an adjustment was needed I would go to my normal position. So I would receive 1.00 ($100 bucks), I pay 3.50 to close it ($350) bucks, then I receive $200 of new credit playing 2 contracts with the adjustment. Final result 1.00 credit - 3.50 debit + 2.00 credit = -0.50 or a $50 loss. This could severely mitigate Credit Call spread losses in the long run.

Many of you would argue that I'm doubling down, and oh what a sin that is. And yes, it's true! But I am starting at a smaller position size now. With the adjustment I'm simply going to what used to be my normal position. If the adjustment is threatened, I would open the second adjustment using normal position size and would eat a normal loss.

This principle would also be applied to an Unbalanced Iron Condor. You typically receive 0.60 credit plus 1.00 credit respectively for the Put and Call side of a 10 point wide Iron Condor, 10% prob. ITM on each side. My play would be:

Sell 2 Credit Put spreads 0.60 credit ($120)

Sell 1 Credit Call spread 1.00 credit ($100)

Call side hits 30% probability and I pay 3.50 debit to close it, immediately deploying a normal position: 2 Credit Call spreads for 1.00 credit ($200). Final result +$120 + $100 - $350 + $200 = +$70. Your Iron Condor would be profitable even after one adjustment to the Call side. You would start suffering losses only after a second adjustment to the Call side.

Option 3. Collect same premium on both sides and exit based on price levels.

This one is really interesting and has me seriously considering it. For example the typical 5 point wide Iron Condor, 10% prob. in the money on both side gives you 0.80 credit. 0.30 on the Put side and 0.50 on the Call side. With this variation you would sell Puts at around 12%-13% probability and collect 0.40 instead of 0.30. You would sell Calls around the 8% probability collecting 0.40 credit instead of 0.50. Then for your exit, you would make an adjustment as soon as the price of a spread triples. That is as soon as it is worth 1.20. That would be a Credit Put spread with around 32% probability instead of 30% and a Credit Call spread with around 25% probability instead of 30%. You would deploy the new spread again trying to obtain 0.40 credit. This approach allows you to keep both sides the same size, and be indifferent about which one gets tested. Either on the upside or the downside, your adjustment would give you the possibility of having a scratch trade even without increasing your position size.

Sell 4 Credit Put spreads 0.40 credit ($160)

Sell 4 Credit Call spreads 0.40 credit ($160)

Close the Call side when it is worth around 1.20 (approximately 25 deltas) or close the Put side when it is worth around 1.20 (approximately 32 deltas). Open a new credit spread farther out for 0.40 credit, same position size. Final result: 0.40 + 0.40 - 1.20 + 0.40 = 0.00. Your Iron Condors will start losing money only after a second adjustment, and this is all without doubling up on any bet.

In these cases, an individual credit spread would give you a loss: 0.40 credit, 1.20 debit, 0.40 new credit = 0.40 debit. The beautiful thing is that the size of your losers after one adjustment would be the same as the size of your winners. If you simply have more winners than losers, you would be profitable overall. Which I think is fairly achievable especially on the Put side. This is assuming you never double down on the adjustment. You simply keep the same position size.

Option 4. Stop being such a little bitch. Stop complaining. You are still profitable overall and losses are simply inevitable from time to time.

I could do that and keep my current methods. But I wouldn't be a normal human being. I would be entering robot territory. I truly believe there is underestimation of market moves to the upside and not doing anything would be dumb if I'm truly convinced that to be the case. Which I am.

So, what will I do going forward? How will my trading change?

To tell you the truth I'm still not sure, but I think it will be a combination of things. I think I will combine method 2 and method 3 depending on how bullish I feel. (Method 3 would lead me to close Calls earlier than I do now).

I hope you enjoyed this article, and as always, feedback is appreciated. A huge part of my success is the feedback I get from fellow traders on here, or via email or Twitter. So, I'm always open to considering other alternatives.

Take it easy, but take it anyways.

I'm off to Florida on Wednesday so, there won't be a Portfolio Analysis next weekend. That's good. Miss me a little.

Your pal,

LT

Check out 2014 Track Record

Related Articles:

Weekend Portfolio Analysis (November 22, 2014)

Options Trading reflections (2016 Edition)

Here's a breakdown of my trading activity by strategy. I separated the results of Iron Condors, individual Credit Put spreads and individual Credit Call spreads for the last 12 months of trading activity: from December 2013 to November 2014.

An Iron Condor position to me is not only the initial trade. To me, if I made an adjustment to one of the sides, that adjustment is part of the Iron Condor trade management. So, on the below table some individual credit spreads are included which served as adjustments (reflected in the Notes column). Logically these individual credit spreads are not reflected in the Credit spreads tables later on.

In particular the April RUT 1020/1030/1245/1255 was misplayed. When the Call side was threatened, instead of just adjusting as usual, closing the Calls and selling farther out of the money Calls, I truly believed the market was never again going to come down, so I sold Puts as well. That's why I closed that entire Iron Condor and opened an entirely new one 1080/1090/1280/1290, whose Put side was quickly threatened. That was a stupid move. I never adjust that way and never should, especially in an overbought market. Had I adjusted as usual, just selling the 1280/1290 Credit Call spread, then the loss on the Iron Condor would have only been -420 + 300 = -120. The return for the Iron Condor strategy would have been $1563, or more than 15% for the model portfolio.

My Iron Condors have an 80% probability of success at entry. Each side has a 10% probability of expiring in the money when the trade is entered. However, I make adjustments as soon as one side hits 30% probability. This means that if I have room before the 30% probability is hit on the Put side plus room before the 30% number is hit on the Call side, the real room for the market to move without me having to make any adjustment at all is 40% of the spectrum in the middle of the Iron Condor (30% + 40% + 30%). Lo and behold, 5 out of 12 Iron Condors did not need to be touched at all which is 41.5% of the Iron Condors played. Scary how those probability numbers work.

To me this only has one explanation and I know this could be a bit controversial, but criticizing without offering real solutions adds no value to me. So here it goes: The probability models on the TOS platform DO consistently underestimate upside moves in the markets. There, I said it.

Even assuming I'm wrong, and that probability models on the ThinkOrSwim platform reflect correct numbers for Out of the Money Calls, the simple fact that volatility decreases on the way up making adjustments unbelievably unattractive implies that something must be done differently when trading Calls in this life if you want to be more profitable in the long run.

On the way down, volatility expands and it is not uncommon to be able to place your adjustments 10% - 15% below the market. Meaning, if you sold Puts during an oversold environment, the market had already corrected probably 5% - 10%. If you are tested and place the adjustment 10% below the original point, you are now challenging the market to a total 20% or 25% fall. So, even though we fear a market crash every day, they are very infrequent. 4 times since 1950 (1974, 1987, 2000, 2008). Even in those instances, after two adjustments on the Put side you would probably be OK. Three adjustments on the Put side would Put you really far below and with a very very high probability of surviving a severe market crash. So, folks, Credit Spread traders of the world! Unite! The danger is on the Call side. Stop the obsession with market crashes. Your real hidden enemy is the upside where your adjustments are barely 2% - 3% above and the market can keep fucking you at will indefinitely.

How to neutralize this issue?

Once you jump to a conclusion you have to design a plan of attack. Otherwise this would just be a futile exercise. There is a problem. To me it is clear it exists. Now, how do we deal with it?

Option 1. Stop selling Calls altogether

This could be your way out. Frankly, it is not my favorite and I won't do this. I enjoy playing Iron Condors and they have a Call side. Iron Condors allow me to mitigate losses in the case of Call side adjustments and I don't suffer that much with them. So, I won't stop selling Calls altogether.

Option 2. Sell smaller Credit Call spread positions

This could be a very viable alternative. What do I mean by this?

It's very simple.

Instead of using your typical portfolio allocation per position, you cut it in half for the Calls. This is applied to both Individual Credit Call spreads and Iron Condors, which would turn into Unbalanced Iron Condors. In the case of an adjustment, you go to your normal position. For example:

Right now I would normally sell the 2110/2120 SPX December Credit Call spread. I would sell 2 contracts. The credit is 1.00 per contract which is typical for a 10% probability ITM 10 point wide Credit Call spread. My risk would be 9.00 or $1800 in dollar terms. This spread would be worth 3.50 at the 30% probability level.

Sell 2 SPX December 2110/2120 Credit Call spread.

Credit: 1.00

Max risk: 9.00

If the spread is threatened, I pay 3.50 debit * 2 = $700 to close it. And deploy a new spread further up for another 1.00 credit. Assuming the adjustment wins: 1.00 credit - 3.50 debit + 1.00 credit = -1.50 or a $300 loss.

Instead of the above scenario, I would start playing just one contract and if an adjustment was needed I would go to my normal position. So I would receive 1.00 ($100 bucks), I pay 3.50 to close it ($350) bucks, then I receive $200 of new credit playing 2 contracts with the adjustment. Final result 1.00 credit - 3.50 debit + 2.00 credit = -0.50 or a $50 loss. This could severely mitigate Credit Call spread losses in the long run.

Many of you would argue that I'm doubling down, and oh what a sin that is. And yes, it's true! But I am starting at a smaller position size now. With the adjustment I'm simply going to what used to be my normal position. If the adjustment is threatened, I would open the second adjustment using normal position size and would eat a normal loss.

This principle would also be applied to an Unbalanced Iron Condor. You typically receive 0.60 credit plus 1.00 credit respectively for the Put and Call side of a 10 point wide Iron Condor, 10% prob. ITM on each side. My play would be:

Sell 2 Credit Put spreads 0.60 credit ($120)

Sell 1 Credit Call spread 1.00 credit ($100)

Call side hits 30% probability and I pay 3.50 debit to close it, immediately deploying a normal position: 2 Credit Call spreads for 1.00 credit ($200). Final result +$120 + $100 - $350 + $200 = +$70. Your Iron Condor would be profitable even after one adjustment to the Call side. You would start suffering losses only after a second adjustment to the Call side.

Option 3. Collect same premium on both sides and exit based on price levels.

This one is really interesting and has me seriously considering it. For example the typical 5 point wide Iron Condor, 10% prob. in the money on both side gives you 0.80 credit. 0.30 on the Put side and 0.50 on the Call side. With this variation you would sell Puts at around 12%-13% probability and collect 0.40 instead of 0.30. You would sell Calls around the 8% probability collecting 0.40 credit instead of 0.50. Then for your exit, you would make an adjustment as soon as the price of a spread triples. That is as soon as it is worth 1.20. That would be a Credit Put spread with around 32% probability instead of 30% and a Credit Call spread with around 25% probability instead of 30%. You would deploy the new spread again trying to obtain 0.40 credit. This approach allows you to keep both sides the same size, and be indifferent about which one gets tested. Either on the upside or the downside, your adjustment would give you the possibility of having a scratch trade even without increasing your position size.

Sell 4 Credit Put spreads 0.40 credit ($160)

Sell 4 Credit Call spreads 0.40 credit ($160)

Close the Call side when it is worth around 1.20 (approximately 25 deltas) or close the Put side when it is worth around 1.20 (approximately 32 deltas). Open a new credit spread farther out for 0.40 credit, same position size. Final result: 0.40 + 0.40 - 1.20 + 0.40 = 0.00. Your Iron Condors will start losing money only after a second adjustment, and this is all without doubling up on any bet.

In these cases, an individual credit spread would give you a loss: 0.40 credit, 1.20 debit, 0.40 new credit = 0.40 debit. The beautiful thing is that the size of your losers after one adjustment would be the same as the size of your winners. If you simply have more winners than losers, you would be profitable overall. Which I think is fairly achievable especially on the Put side. This is assuming you never double down on the adjustment. You simply keep the same position size.

Option 4. Stop being such a little bitch. Stop complaining. You are still profitable overall and losses are simply inevitable from time to time.

I could do that and keep my current methods. But I wouldn't be a normal human being. I would be entering robot territory. I truly believe there is underestimation of market moves to the upside and not doing anything would be dumb if I'm truly convinced that to be the case. Which I am.

So, what will I do going forward? How will my trading change?

To tell you the truth I'm still not sure, but I think it will be a combination of things. I think I will combine method 2 and method 3 depending on how bullish I feel. (Method 3 would lead me to close Calls earlier than I do now).

I hope you enjoyed this article, and as always, feedback is appreciated. A huge part of my success is the feedback I get from fellow traders on here, or via email or Twitter. So, I'm always open to considering other alternatives.

Take it easy, but take it anyways.

I'm off to Florida on Wednesday so, there won't be a Portfolio Analysis next weekend. That's good. Miss me a little.

Your pal,

LT

Check out 2014 Track Record

Related Articles:

Weekend Portfolio Analysis (November 22, 2014)

Options Trading reflections (2016 Edition)

Go to the bottom of this page in order to see the Legal Stuff

Nice analysis. I came to the same conclusion after suffering some big losses on my credit call spreads in 2012 and 2013. I even toyed with the idea of just selling credit put spreads like someone we both know. But at the same time, I feel that having some credit call spreads can mitigate losses when the market starts going down like early in October.

ReplyDeleteMy strategy is to wait for the market to become overbought before selling credit call spreads. I would only sell a small credit call spread position. I don't want to be a hero and sell too much because the risk/reward is just not that great for credit call spreads.

My credit call spreads are always hedged with credit put spreads. I would have 3 to 5 credit put spread positions for every credit call spread position. It is unbalanced for the same reasons you have clearly expressed in this article.

If my credit call spreads become threatened (30% delta or triple the credit received) then I would close the position and redeployed a new further out of the money credit call spreads with a delta around 15.

One thing that I do which can be risky is that I will roll up the safe credit put spread side too so that I can receive even more credit. I know this is not a good idea when the market is super overbought. But I also know that if I need to adjust the credit put spread later on, the VIX will be very high and I can double the number of contracts on the way down with confidence.

Here are 3 things I have learned about credit call spreads:

1. Only sell when markets are overbought

2. Keep the credit call spread positions small

3. Always hedge with more credit put spread positions

Good luck with your new revised strategy. I will be watching with interest.

You can follow me on Twitter @lienjonathan where I tweet my 90% probability credit spread trades in real-time for free.

Thanks for the feedback Jonathan. I think your takeaways, clearly summarized, are of great value for any reader of your comment. Which to be fair, were points you had already mentioned to me in the past.

DeleteGood luck this week.

LT

Thanks for the great analysis!

ReplyDeleteThanks Andrew

DeleteLT

First of all, thank you for this great article!

ReplyDeleteIn the last years the markets have been a bullish bias, so I was wondering if your conclusions on the call spreads depends on this. Selling call spread is a a bearish strategy, so it is not surprising that it had a negative performance last year. But we cannot predict the market. What if, after the last 5 year rally, the market bias will change?

Hey Thomas,

DeleteThe problem is that it is true the market can go down, but the drawdowns although deeper tend to be shorter in duration. Up moves on the other hand, although not as steep generally speaking, can and will be sustained generally longer.

Notice how I mentioned that even when the market was negative for the year, I had been tested on the Call side more frequently.

On a persistent bear market, Calls will help, that's why I won't stop selling them altogether. But like I said, Put adjustments are very healthy and very far from the market. How many months of -20% will we see? Probably 1 or 2, maybe 3 during our trading careers. I'm not too concerned about a -40% correction if it happens throughout an entire year. My concern really is a month or two.

In 2011, people forget there was a bearish environment for quite a while (even in the middle of the 2009-2014 bullish cycle). 2011 was pretty challenging with all the US Debt ceiling issues, yet, I would have been tested on the Call side more frequently. Again confirming my assumptions that market upside moves are generally underestimated by probability models, at the same time that downside moves are consistently overestimated.

Regards,

LT