Trade Details:

(It was actually entered yesterday July 31, I just didn't find the time to come blog about it)

4 September SPX 2730/2720 Credit Put spread @0.65 credit each

1 September SPX 3120/3130 Credit Call spread @1.05 credit

Net Credit: $365

Max Risk: $3,625

50 days to Exp.

Profit/Risk Profile

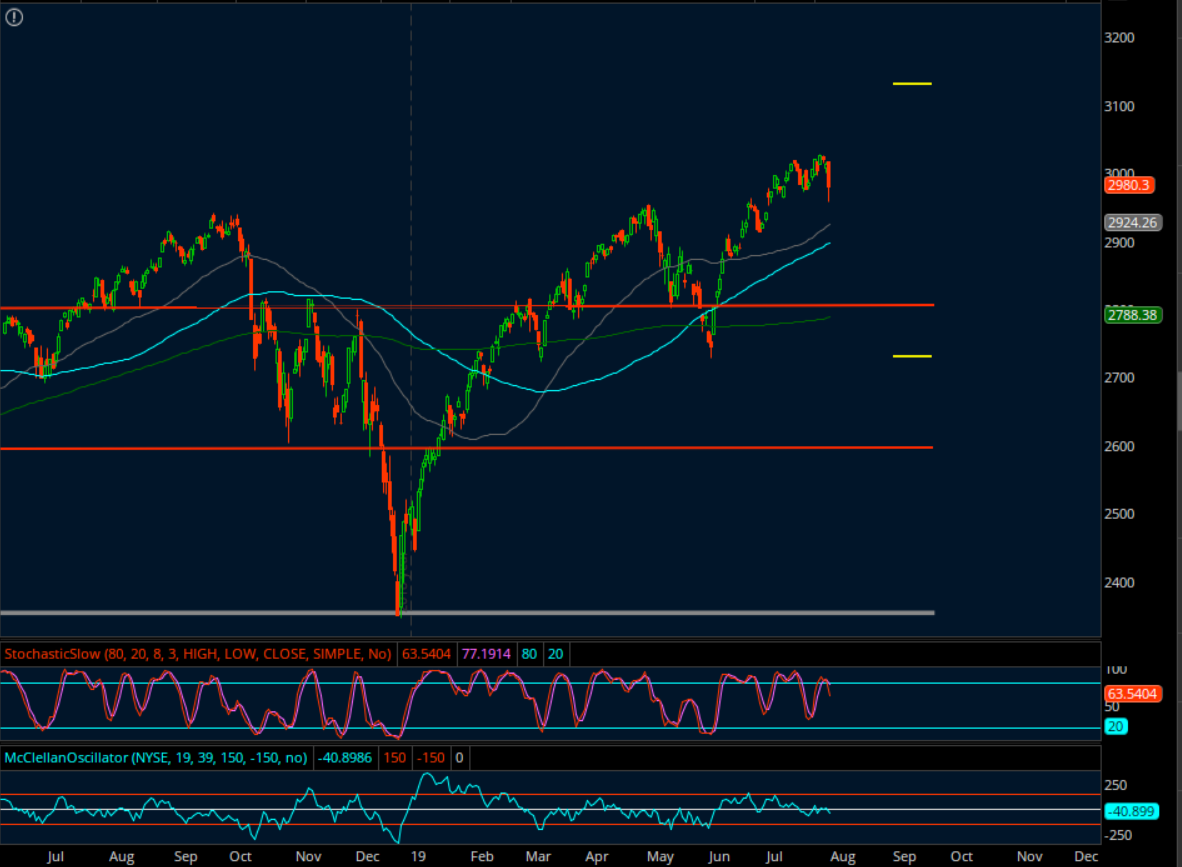

SPX Chart for future reference:

Trade Update - August 5, 2019

August Market sell-off

Adjusted the Put side

Closed 4 September SPX 2730/2720 Credit Put spread @2.35 debit each

Original Credit was 0.65 per

Net loss: 1.70 per. $680 in dollar terms for 4 spreads

Opened 4 September SPX 2500/2490 Credit Put spread @0.75 credit each

Total Credit: $300

(It was actually entered yesterday July 31, I just didn't find the time to come blog about it)

4 September SPX 2730/2720 Credit Put spread @0.65 credit each

1 September SPX 3120/3130 Credit Call spread @1.05 credit

Net Credit: $365

Max Risk: $3,625

50 days to Exp.

Profit/Risk Profile

SPX Chart for future reference:

Trade Update - August 5, 2019

August Market sell-off

Adjusted the Put side

Closed 4 September SPX 2730/2720 Credit Put spread @2.35 debit each

Original Credit was 0.65 per

Net loss: 1.70 per. $680 in dollar terms for 4 spreads

Opened 4 September SPX 2500/2490 Credit Put spread @0.75 credit each

Total Credit: $300

After this, we are now in an SPX Unbalanced Iron Condor position 2490/2500/3120/3130 with $405 credit. And there is for now a realized loss of $680.

Trade Update - August 19, 2019

With 31 days until expiration, most of the profit has been made. Closing this one off in order to deploy in the October exp cycle.

Closed 4 September SPX 2500/2490 Credit Put spread @0.15 debit each

Original credit was 0.75 per. Net profit is 0.60 per spread. $240 in dollar terms

Closed 1 September SPX 3120/3130 Credit Call spread @0.15 debit

Original credit was 1.05. Net profit is 0.90 or $90 dollars in one spread played.

Combining both sides, it is a $330 gain today.

Now, earlier on August 5, we had a $680 loss on the original Put side. Therefore, the final result for the entire position is -680 + 330 = -$350

That, on a max risk of $3,625 represents a -9.7% Return on Risk

I could have left this position to expire for max profit. But it doesn't make a lot of sense.

There were still 0.15 to make on the Put side ($60 in 4 spreads) plus $15 more to make on the Call side for a total of $75 dollars. At 31 days to expiration, that represents approximately $2.42 per day on average. Using the same capital on a brand new position where we receive roughly $400 credit for 59 days to expiration is a much more attractive way to put money to work at an average rate of $6.78 per day.

Trade Update - August 19, 2019

With 31 days until expiration, most of the profit has been made. Closing this one off in order to deploy in the October exp cycle.

Closed 4 September SPX 2500/2490 Credit Put spread @0.15 debit each

Original credit was 0.75 per. Net profit is 0.60 per spread. $240 in dollar terms

Closed 1 September SPX 3120/3130 Credit Call spread @0.15 debit

Original credit was 1.05. Net profit is 0.90 or $90 dollars in one spread played.

Combining both sides, it is a $330 gain today.

Now, earlier on August 5, we had a $680 loss on the original Put side. Therefore, the final result for the entire position is -680 + 330 = -$350

That, on a max risk of $3,625 represents a -9.7% Return on Risk

I could have left this position to expire for max profit. But it doesn't make a lot of sense.

There were still 0.15 to make on the Put side ($60 in 4 spreads) plus $15 more to make on the Call side for a total of $75 dollars. At 31 days to expiration, that represents approximately $2.42 per day on average. Using the same capital on a brand new position where we receive roughly $400 credit for 59 days to expiration is a much more attractive way to put money to work at an average rate of $6.78 per day.

Go to the bottom of this page in order to see the Legal Stuff

No comments:

Post a Comment