Important Note 1: New material has been added to the LTOptions's library. Elephants vs Iron Condors (Full Comparison) is an eBook that details among other things: key differences between the two strategies; pros and cons; which one performs better according to the environment; evolution of the T+0 line over time, etc. This new eBook is visible on the page that comes right after logging in:

Important Note 2: Some modifications have recently been made to the 2018 Options Trading Plan. The changes are focused on efficiency and simplicity when defending Credit Call spreads. Log in to LTOptions.com and consult the 2018 Options Trading Plan ebook.

Market Conditions

(Click on image to enlarge)

Stochastics: 13 (Oversold. Down from 88, 93 and 95 the weeks before)

Stochastics: 13 (Oversold. Down from 88, 93 and 95 the weeks before)

McClellan: -272 (Oversold. Down from -11 and -11 the previous weekends)

Stocks above their 20 DMA: 25% (Oversold. Down from 65%, 70% and 74% the weeks before)

Oversold

Finally the bearish divergence played out. We are now in a short-term oversold condition. The market has more to correct in the long run if you consider that more than 60% of the stocks are trading above the 200-day average. But, short-term, we have quickly reached and overly pessimistic environment. As usual, accompanied by higher volatility with a VIX above 17, something that we hadn't seen since the days prior to the 2016 election.

Usually by the time an oversold condition is reached, the index is below its 50-day average. The SPX is, however, still higher than its 50-day. It is wise to tread carefully here. It is a good time to deploy out of the money Credit Put spreads. Unfortunately, I have more exposure than I would like, but I'll still try to take advantage of this environment, possibly with a RUT Credit Put spread around 1330 (April expiration). Speaking of RUT:

(Click on image to enlarge)

Less stretched than the SPX. The Russell is already below its 50-day average, hence the reason why I would choose this one for a Bull Put spread position.

Less stretched than the SPX. The Russell is already below its 50-day average, hence the reason why I would choose this one for a Bull Put spread position.

Action Plan for the Week

1- I want to take advantage of the current elevated volatility and oversold environment by selling a RUT Credit Put spread. The problem though, is that I have exposure in February (2 positions) and March (2 positions). Adding a fifth one would be a risk level I'm not comfortable with. So, I will most likely close the Feb RUT Position, which is the Put side of what originally was an Elephant. It can be closed at about break-even, reducing the RUT risk concentration that exists anyway when combined with the March RUT Put spreads (part of Iron Condor). Then, I'll be free to deploy capital. I will go with April in this case to add some time diversification. RUT is currently at 1,547. April Credit Put spreads around 10 deltas are in the 1330-1340 area, which is about 15% lower than current levels. It sucks to close a position (Feb Puts) at break-even after so much holding. The other alternative is to keep holding those and deploy a small April RUT Credit Put spread instead of a full position.Just half or a quarter the typical size.

2- I'll close the Call side of the SPX March Elephant for 75% of its max potential profit. I got $760 from the 2940/2950 Credit Call spreads, minus $333 debit invested in SPY 292 Calls. So, the net credit and max potential profit is $427. 75% of that is $320 and the current gain is close to $360. This gain may dissappear on a huge gap up on Monday. But if that is not the case, I will be closing it with the expectation of redeploying it if there is a market rebound from here until expiration.

3- Other than that, potential adjustments to the Put side of the March SPX Elephant if the short Puts reach 30 deltas (SPX around 2,720). The new Put spreads would be around the 2,450 strike prices. Similarly, I'd be adjusting the Put side of the March RUT Iron Condor, if the short Puts reach the 30-delta mark (RUT around 1,510). The new put spreads would be those that are around the 10-delta mark by then, which can be near the low 1300's.

4- Last week I mentioned the idea of opportunistically buying some options .... (This is a more long-term action plan, only available inside LTOptions.com).

Economic Calendar

Pretty light this time around.

Tuesday: ISM Non-Manufacturing PMI.

Thursday: ECB Economic Bulletin.

Be wise, trade safely.

LT

If you are interested in a responsible and sustainable way of trading options for consistent income with solid risk management, consider acquiring LTOptions, my options trading system to the last detail.

Check out 2018 Track Record

Important Note 2: Some modifications have recently been made to the 2018 Options Trading Plan. The changes are focused on efficiency and simplicity when defending Credit Call spreads. Log in to LTOptions.com and consult the 2018 Options Trading Plan ebook.

Recent Trading Activity

- Closed the Mar. SPX 2900/2905 Credit Call spread partially hedged with Long SPY 290 Calls

on Monday at a $1770 loss. Pretty bad timing here. Had I followed the original plan of holding until SPX 2895, well, I wouldn't have taken this loss. Psychology, psychology, psychology.

- Initiated a March SPX Unbalanced Elephant on Thursday for $1,527 credit. Also, awful timing here. Had I opened a position on Friday instead of Thursday, it would have been just Credit Put spread much lower down thanks to the oversold condition reached. Perhaps a good lesson that when we are so close to overbought, it is better to not rush an entry on Thursday and instead wait until Friday to see if the oversold condition materializes.

- Closed the Mar. SPX 2900/2905 Credit Call spread partially hedged with Long SPY 290 Calls

on Monday at a $1770 loss. Pretty bad timing here. Had I followed the original plan of holding until SPX 2895, well, I wouldn't have taken this loss. Psychology, psychology, psychology.

- Initiated a March SPX Unbalanced Elephant on Thursday for $1,527 credit. Also, awful timing here. Had I opened a position on Friday instead of Thursday, it would have been just Credit Put spread much lower down thanks to the oversold condition reached. Perhaps a good lesson that when we are so close to overbought, it is better to not rush an entry on Thursday and instead wait until Friday to see if the oversold condition materializes.

Market Conditions

(Click on image to enlarge)

McClellan: -272 (Oversold. Down from -11 and -11 the previous weekends)

Stocks above their 20 DMA: 25% (Oversold. Down from 65%, 70% and 74% the weeks before)

Oversold

Finally the bearish divergence played out. We are now in a short-term oversold condition. The market has more to correct in the long run if you consider that more than 60% of the stocks are trading above the 200-day average. But, short-term, we have quickly reached and overly pessimistic environment. As usual, accompanied by higher volatility with a VIX above 17, something that we hadn't seen since the days prior to the 2016 election.

Usually by the time an oversold condition is reached, the index is below its 50-day average. The SPX is, however, still higher than its 50-day. It is wise to tread carefully here. It is a good time to deploy out of the money Credit Put spreads. Unfortunately, I have more exposure than I would like, but I'll still try to take advantage of this environment, possibly with a RUT Credit Put spread around 1330 (April expiration). Speaking of RUT:

(Click on image to enlarge)

Current Portfolio

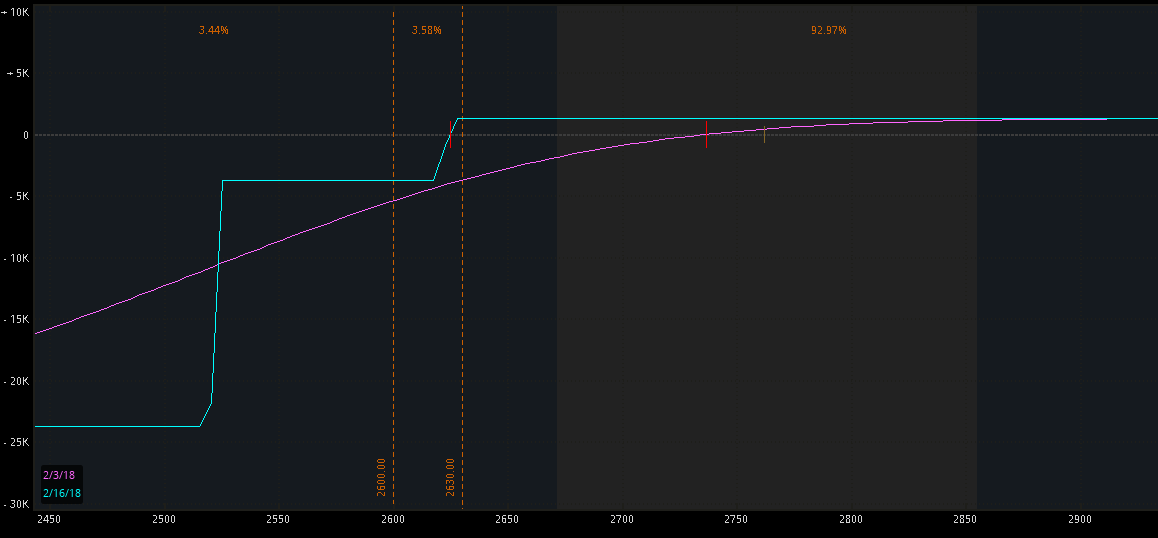

Feb. SPX 2520/2525 Credit Put spread

with additional 2625/2630 Credit Put spread

Net credit: $1,300. Two weeks to expiration.

(Click on image to enlarge)

Defense

line: 2,630 (adjust the small 2625/2620 Credit Put spread) and then 2600 is the trigger for adjusting the 2525/2520 Credit Put spread. I think those positions are both safe and that we are unlikely to see SPX 2630 (currently at 2762) in the next two weeks. So, I am willing to keep holding these.

Defense

line: 2,630 (adjust the small 2625/2620 Credit Put spread) and then 2600 is the trigger for adjusting the 2525/2520 Credit Put spread. I think those positions are both safe and that we are unlikely to see SPX 2630 (currently at 2762) in the next two weeks. So, I am willing to keep holding these.

Feb. RUT/IWM - 1455/1460 - 147 Elephant Put side

Net Credit: $1,060. Two weeks to expiration.

(Click on image to enlarge)

Defense line: 1,495 (adjust Put side). It was looking much safer before. Right now we can't say it is in deep trouble or anything. It is about break-even and at the 11-delta mark.

Defense line: 1,495 (adjust Put side). It was looking much safer before. Right now we can't say it is in deep trouble or anything. It is about break-even and at the 11-delta mark.

Mar. RUT 1440/1450/1680/1690 Unbalanced Iron Condor

Net Credit: $1,680. Six weeks to expiration.

(Click on image to enlarge)

Defense lines: 1510 (adjust Put spreads). 1640 Close Call side at a loss. So, there is some risk concentration between this position (to defend at RUT 1510) and the previous one (to be defended around RUT 1495). It would be more uncomfortable if the estimated adjustment points were both 1510, a risk I would stay away from by immediately closing one of them. With 1510 and 1495, there is some room though. I'm willing to hold, but short leash. More details in the Action Plan section.

Defense lines: 1510 (adjust Put spreads). 1640 Close Call side at a loss. So, there is some risk concentration between this position (to defend at RUT 1510) and the previous one (to be defended around RUT 1495). It would be more uncomfortable if the estimated adjustment points were both 1510, a risk I would stay away from by immediately closing one of them. With 1510 and 1495, there is some room though. I'm willing to hold, but short leash. More details in the Action Plan section.

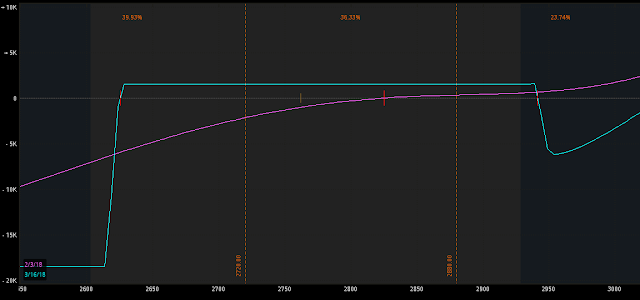

Mar. SPX/SPY 2615/2625/2940/2950-295 Elephant

Net Credit: $1,527 and six weeks to expiration

The position entered 48 hours ago, quickly got under water. Yep, it hasn't been kind.

(Click on image to enlarge)

Defense line: 2720 (adjust the Put side). Could be lower, perhaps 2,715 or 2,710. To the upside, SPX 2880 triggers a closure of the Call side of the Elephant.

Defense line: 2720 (adjust the Put side). Could be lower, perhaps 2,715 or 2,710. To the upside, SPX 2880 triggers a closure of the Call side of the Elephant.

Feb. SPX 2520/2525 Credit Put spread

with additional 2625/2630 Credit Put spread

Net credit: $1,300. Two weeks to expiration.

(Click on image to enlarge)

Feb. RUT/IWM - 1455/1460 - 147 Elephant Put side

Net Credit: $1,060. Two weeks to expiration.

(Click on image to enlarge)

Mar. RUT 1440/1450/1680/1690 Unbalanced Iron Condor

Net Credit: $1,680. Six weeks to expiration.

(Click on image to enlarge)

Mar. SPX/SPY 2615/2625/2940/2950-295 Elephant

Net Credit: $1,527 and six weeks to expiration

The position entered 48 hours ago, quickly got under water. Yep, it hasn't been kind.

(Click on image to enlarge)

Action Plan for the Week

1- I want to take advantage of the current elevated volatility and oversold environment by selling a RUT Credit Put spread. The problem though, is that I have exposure in February (2 positions) and March (2 positions). Adding a fifth one would be a risk level I'm not comfortable with. So, I will most likely close the Feb RUT Position, which is the Put side of what originally was an Elephant. It can be closed at about break-even, reducing the RUT risk concentration that exists anyway when combined with the March RUT Put spreads (part of Iron Condor). Then, I'll be free to deploy capital. I will go with April in this case to add some time diversification. RUT is currently at 1,547. April Credit Put spreads around 10 deltas are in the 1330-1340 area, which is about 15% lower than current levels. It sucks to close a position (Feb Puts) at break-even after so much holding. The other alternative is to keep holding those and deploy a small April RUT Credit Put spread instead of a full position.Just half or a quarter the typical size.

2- I'll close the Call side of the SPX March Elephant for 75% of its max potential profit. I got $760 from the 2940/2950 Credit Call spreads, minus $333 debit invested in SPY 292 Calls. So, the net credit and max potential profit is $427. 75% of that is $320 and the current gain is close to $360. This gain may dissappear on a huge gap up on Monday. But if that is not the case, I will be closing it with the expectation of redeploying it if there is a market rebound from here until expiration.

3- Other than that, potential adjustments to the Put side of the March SPX Elephant if the short Puts reach 30 deltas (SPX around 2,720). The new Put spreads would be around the 2,450 strike prices. Similarly, I'd be adjusting the Put side of the March RUT Iron Condor, if the short Puts reach the 30-delta mark (RUT around 1,510). The new put spreads would be those that are around the 10-delta mark by then, which can be near the low 1300's.

4- Last week I mentioned the idea of opportunistically buying some options .... (This is a more long-term action plan, only available inside LTOptions.com).

Economic Calendar

Pretty light this time around.

Tuesday: ISM Non-Manufacturing PMI.

Thursday: ECB Economic Bulletin.

Be wise, trade safely.

LT

If you are interested in a responsible and sustainable way of trading options for consistent income with solid risk management, consider acquiring LTOptions, my options trading system to the last detail.

Check out 2018 Track Record

Go to the bottom of this page in order to see the Legal Stuff

No comments:

Post a Comment