Recent Trading Activity

- No Activity. Despite the small price decline, we almost reached an oversold condition, which would have triggered a December RUT Credit Put spread. The McClellan oscillator reached oversold territory on Wednesday and the Stochastics indicator was almost there. However, the % of stocks trading above their 20-day Moving Average remained in the 40's. Seems like a lost opportunity in retrospective but time has taught me to follow the rules and be disciplined.

- No Activity. Despite the small price decline, we almost reached an oversold condition, which would have triggered a December RUT Credit Put spread. The McClellan oscillator reached oversold territory on Wednesday and the Stochastics indicator was almost there. However, the % of stocks trading above their 20-day Moving Average remained in the 40's. Seems like a lost opportunity in retrospective but time has taught me to follow the rules and be disciplined.

Market Conditions

(Click on image to enlarge)

McClellan: -84 (Neutral. Down from -15 last week)

Stocks above their 20 DMA: 49% (Neutral. Down from 59% last week)

No man's land.

Once again, price is higher than last week, and this time all three oscillators went lower. We could argue that the bearish divergence mentioned last week was materialized already with the bearish action we recently saw. But, the fact remains that with the readings this week, that bearish divergence looks more accentuated now.

The index is +2.9% higher than its own 50-day average. Although not a stretch, it suggests that further gains should be slow. Current SPX price is also approaching the first layer of resistance in the uptrend channel, which points to somewhere between 2,596 to 2,602 this upcoming week.

Earnings season is in full force and there have been some spectacular results. Year-end seasonality has also taught me to not aggressively short the market into year end.

The Russell:

(Click on image to enlarge)

Current Portfolio

NOV SPX 2315/2325 Credit Put spread

Net Credit of $1,000. Three weeks to expiration. The remainder of what used to be an Unbalanced Iron Condor. Looking great. No concerns.

(Click on image to enlarge)

Defense lines: 2,375 (adjust Put side). Very far down. nothing to do. More conservative traders can close it and take the gains here. Personally, I'll just keep holding it.

Defense lines: 2,375 (adjust Put side). Very far down. nothing to do. More conservative traders can close it and take the gains here. Personally, I'll just keep holding it.

NOV SPX 2425/2420 Credit Put spread

Net Credit $250. Three weeks to expiration. Small position of ten 5-point wide spreads.

(Click on image to enlarge)

Because of the small size (only one fourth the typical size), we can afford to delay the adjustment until SPX 2,430. With SPX at 2,575 I have no concerns here.

Because of the small size (only one fourth the typical size), we can afford to delay the adjustment until SPX 2,430. With SPX at 2,575 I have no concerns here.

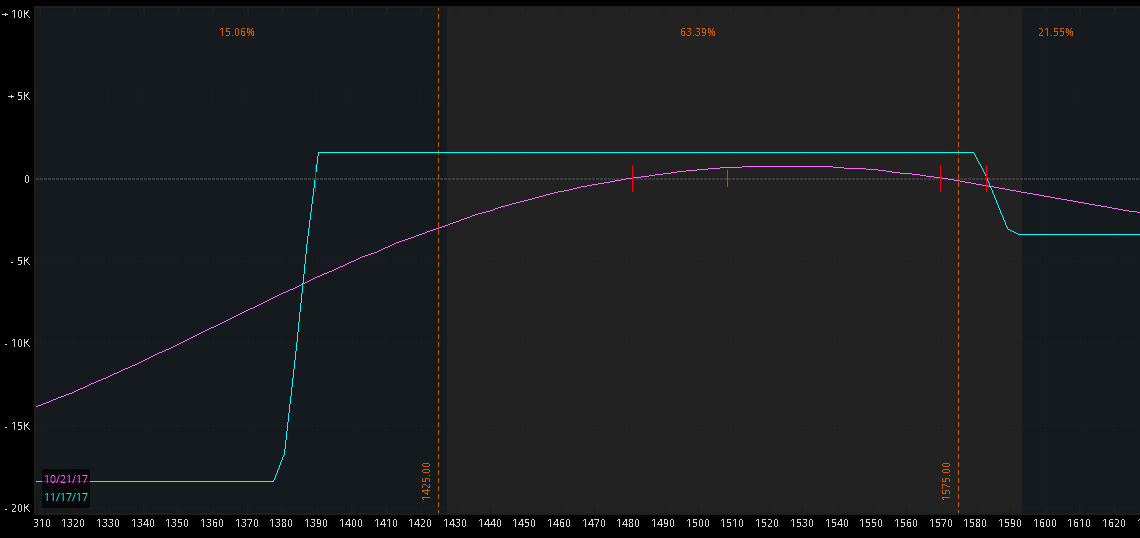

NOV RUT 1380/1390/1580/1590 Unbalanced Iron Condor

Net credit: $1,555. Three weeks to expiration. No concerns for now.

(Click on image to enlarge)

Defense lines: 1,425 to the downside (adjust Put spread) and 1,575 to the upside (adjust Call spread). Both price points are unlikely for the upcoming week. Still a very healthy position that has enjoyed RUT's sideways price action.

Defense lines: 1,425 to the downside (adjust Put spread) and 1,575 to the upside (adjust Call spread). Both price points are unlikely for the upcoming week. Still a very healthy position that has enjoyed RUT's sideways price action.

DEC SPX 2390/2400/2635/2640 Unbalanced Iron Condor

Net credit: $1,555. Seven weeks to expiration. Not looking great. Especially the Call side is taking a little heat although the threat is not imminent.

(Click on image to enlarge)

Defense lines: 2,470 to the downside (adjust Put side) and 2,630 to the upside (adjust Call side).

Defense lines: 2,470 to the downside (adjust Put side) and 2,630 to the upside (adjust Call side).

NOV SPX 2315/2325 Credit Put spread

Net Credit of $1,000. Three weeks to expiration. The remainder of what used to be an Unbalanced Iron Condor. Looking great. No concerns.

(Click on image to enlarge)

NOV SPX 2425/2420 Credit Put spread

Net Credit $250. Three weeks to expiration. Small position of ten 5-point wide spreads.

(Click on image to enlarge)

NOV RUT 1380/1390/1580/1590 Unbalanced Iron Condor

Net credit: $1,555. Three weeks to expiration. No concerns for now.

(Click on image to enlarge)

DEC SPX 2390/2400/2635/2640 Unbalanced Iron Condor

Net credit: $1,555. Seven weeks to expiration. Not looking great. Especially the Call side is taking a little heat although the threat is not imminent.

(Click on image to enlarge)

Action Plan for the Week

- November positions should give us no problems this upcoming week. So, I'll just keep riding them.

- The focus of my attention is the December SPX Unbalanced Iron Condor, in particular its Call side.

The Call spread is at the 20-delta mark. With a 20-point SPX rally, it will reach 30 deltas. If you are tired of suffering this year with the Call side, you can simply close the 2635/2640 spreads for 1.70 debit or so at that point. With an initial credit of 0.50, that would be a 1.20 loss per spread or $600 bucks in my case. That loss is more than compensated by the credit from Put side. So, in the end, the position would be a winner anyways and no more Call side headaches.

Given that the Call side is small (only a 4 to 1 ratio of Puts to Calls), I am willing to wait longer before taking a loss on the 2635/2640 Call spread. My plan for now: if the 2635 strike Calls reach 31 or 32 deltas, I will go ahead and sell a Credit Put spread, probably around SPX 2,450. It will be one fourth the usual capital deployed on Put spreads. So, in my case of a $100,000 portfolio, I would be playing five 10-point wide spreads (0.50 credit or better per spread), or ten 5-point wide spreads (0.25 credit or better). In addition to this move, I'll also be seriously considering a December SPX 2680/2685 Credit Call spread or 2680/2690. Also a small size (10 five-point wide spreads or five 10-point side spreads). This new Call spread would only be adjusted if SPX reaches 2,675 which looks safe enough. With these new credits, I would be willing to close the existing 2635/2640 spread at a loss right then and there, or at a smaller loss on a quick/small market decline.

- Finally, we are getting close to eight weeks to the December monthly options expiration date. Time to enter the second income position of the December cycle. As usual we'll go with RUT and the decision between Unbalanced Iron Condor or Elephant is similar in this situation, although I'm personally leaning more towards the Unbalanced Iron Condor. Let's look at the differences:

1380/1390/1590/1600 Unbalanced Iron Condor

Collecting 0.60 credit per Put spread and 0.75 per Call spread and using 20 Put spreads vs 5 Call spreads. Total credit : $1,575 and defense point on the Call side at RUT 1,585.

1380/1390/1590/1600/160 Unbalanced Elephant

Collecting 0.60 credit per Put spread and 0.75 per Call spread and using 20 Put spreads vs 8 Call spreads. Long 16 of the IWM 160 Calls @0.21 debit each. No downside IWM hedge. Total net credit: $1,464.

The usual initial defense point would be RUT 1,555. If that happens, the entire Call side can be closed at a loss and the Credit from the Put side, which will be much safer then, will more than compensate for the Call side loss, resulting in a net winning trade. But to compare apples to apples, let's say we would defend this Elephant in a similar way, by taking a loss on the Call side only when RUT reaches 1,585.

Let's analyze the evolution of the T+0 lines in both cases and how the hypothetical losses (of the Call side) would look with RUT eventually reaching 1,585 on different dates.

1380/1390/1590/1600 Unbalanced Iron Condor

(Click on image to enlarge)

1380/1390/1590/1600/160 Unbalanced Elephant

(Click on image to enlarge)

In almost all the cases, the Unbalanced Elephant suffers a smaller loss than the Unbalanced Iron Condor. Except if RUT takes a longer time to reach 1,585. The magnitude of the loss on the Elephant is also less predictable, whereas the loss on the Unbalanced Iron Condor is similar regardless of the time it takes for RUT to reach 1,585. Finally, the last observation is that the Elephant losses at 1,585 increase over time. On the other hand, Unbalanced Iron Condor losses decrease the longer it takes for RUT to reach 1,585.

We have no idea how long it will take for RUT to reach 1,585 or even if it will reach that number at all. But if it were to reach it, my guess is that it would take some time to get there, rather than it being something likely to immediately happen. Although this is obviously total speculation.

I will go with a RUT Unbalanced Iron Condor position.

Forex

The LT Trend Sniper system will go short EURUSD at the open on Sunday afternoon. This will be the eight Euro trade in 2017.

FX Results tracked here.

Economic Calendar

Monday: China's Manufacturing and Non-Manufacturing PMI.

Tuesday: Europe's CPI & GDP. US Consumer Confidence.

Wednesday: ADP Nonfarm Employment change. ISM Manufacturing. FOMC Statement.

Friday: US Nonfarm Payrolls & Unemployment rate.

Good luck this week my friends,

LT

If you are interested in a responsible and sustainable way of trading options for consistent income with solid risk management, consider acquiring LTOptions, my options trading system to the last detail.

Check out 2017 Track Record

Go to the bottom of this page in order to see the Legal Stuff

No comments:

Post a Comment