Folks, there wasn't much time to look at the markets this week, or tweet or anything. My presence in the social media universe was limited in the middle of a busy week at work, in an office environment for the first time in 17 months. No trades either, and the markets barely moved. For this reason, the market conditions segment is going to be almost the same, but I will take advantage of this quiet environment, where there isn't much new to say, to analyze the current positions in more depth.

Market Conditions

(Click on image to enlarge)

Stochastics: 83 (overbought)

Stochastics: 83 (overbought)

McClellan: -37 (neutral)

Stocks above their 20 DMA: 58% (neutral)

No man's land.

Even though the market has kept moving up in slow motion, it is interesting to note that the number of stocks above their 20 DMA has been consistently going down. In the last four weeks this has been the progression: 80%, 66%, 60%, and now 58%.

We also have the VIX at one of its lowest levels since sex was invented: 11.55

Of course I'm bearish. This doesn't mean I'll bet the house shorting the market. Never do it. Plus, there are concise rules to follow. It means that's just my bias. We are still 10 weeks away from October expiration. Too far for my liking. The odds of me initiating a new position this week are the same as me winning the Individual All-Around finals of the Rhythmic Gymnastics at the Olympics in Rio.

Action Plan for the Week

- Nothing to do, unless we reach an extreme. If we reach SPX 2,210 or so, we may be overbought. In that case I would initiate SPX 2260/2270 Credit Call spread (September options). If we reach SPX 2,120 or so, we may be reaching a short-term oversold extreme. At that point I would sell a Credit Put spread in whichever of the two indexes looks more oversold. Other than that, no need to be over involved with the markets this week.

Economic Calendar

Tuesday: Housing Starts, Building Permits, CPI

Recent Trading Activity

- No opening or closing trades were made. This is always a good thing.

- No opening or closing trades were made. This is always a good thing.

Market Conditions

(Click on image to enlarge)

McClellan: -37 (neutral)

Stocks above their 20 DMA: 58% (neutral)

No man's land.

Even though the market has kept moving up in slow motion, it is interesting to note that the number of stocks above their 20 DMA has been consistently going down. In the last four weeks this has been the progression: 80%, 66%, 60%, and now 58%.

We also have the VIX at one of its lowest levels since sex was invented: 11.55

Of course I'm bearish. This doesn't mean I'll bet the house shorting the market. Never do it. Plus, there are concise rules to follow. It means that's just my bias. We are still 10 weeks away from October expiration. Too far for my liking. The odds of me initiating a new position this week are the same as me winning the Individual All-Around finals of the Rhythmic Gymnastics at the Olympics in Rio.

Current Portfolio

SEP SPX 1825/1800 Debit Put Spread + 1625/1600 Credit Put Spread

Portfolio Insurance

The position will likely lose money in the end, as usual with anti-crash protection plays. But it will be a small $160 loss. The tent has been nicely going up and we have nice protection should the market plummet into the eighteen hundreds.

The position will likely lose money in the end, as usual with anti-crash protection plays. But it will be a small $160 loss. The tent has been nicely going up and we have nice protection should the market plummet into the eighteen hundreds.

OCT SPX 1825/1800 Debit Put Spread + 1625/1600 Credit Put Spread

Portfolio Insurance

The T+0 line is not too high at the moment, offering little protection, but it will start to speed up in the next few days. Unlike long Put options, decimated by the passage of time, these positions get better and better as time goes by and they get closer to expiration.

The T+0 line is not too high at the moment, offering little protection, but it will start to speed up in the next few days. Unlike long Put options, decimated by the passage of time, these positions get better and better as time goes by and they get closer to expiration.

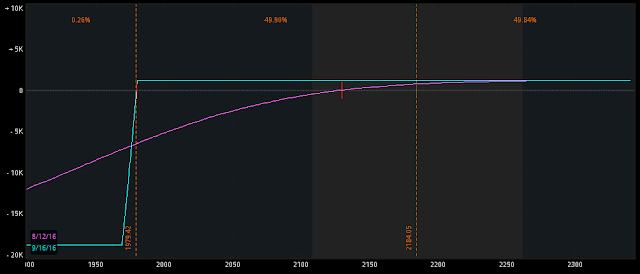

Combining both the September Space Trip trade and the October Space Trip, this is how the portfolio protection looks at the moment.

(Click on image to enlarge)

At the cost of $330 debit (which will likely be lost), and a margin of $10,330 in the account, we have decent downside protection throughout a wide range of SPX prices. I will simply keep riding this thing until expiration, as the impact in terms of performance is minimal for the portfolio, and really, the longer they are in the portfolio, the better and stronger they get with that pink line moving up consistently overtime. I haven't added November and December Space Trip trades. The initial goal was to always have 4 on at the same time. That would be really solid downside protection. Perhaps I should consider adding them.

At the cost of $330 debit (which will likely be lost), and a margin of $10,330 in the account, we have decent downside protection throughout a wide range of SPX prices. I will simply keep riding this thing until expiration, as the impact in terms of performance is minimal for the portfolio, and really, the longer they are in the portfolio, the better and stronger they get with that pink line moving up consistently overtime. I haven't added November and December Space Trip trades. The initial goal was to always have 4 on at the same time. That would be really solid downside protection. Perhaps I should consider adding them.

September SPX 1970/1980 Credit Put Spread

$1,200 credit. Just 5 deltas and 5 weeks to expiration. No concerns.

$750 of open profits but I still want to milk it a little bit more. Here's the risk profile picture:

September RUT/IWM 1090/1100/113/1280/1290 Lazy Elephant

An overall 82% probability of success, feeling comfortable at the moment.

(Click on image to enlarge)

Small open profit of +$239 out of a maximum possible of $1,114.

Small open profit of +$239 out of a maximum possible of $1,114.

Time decay $23.34 dollars per day, a number that will keep improving.

5 deltas on the Put side, 12 deltas on the Call side. Not too bad.

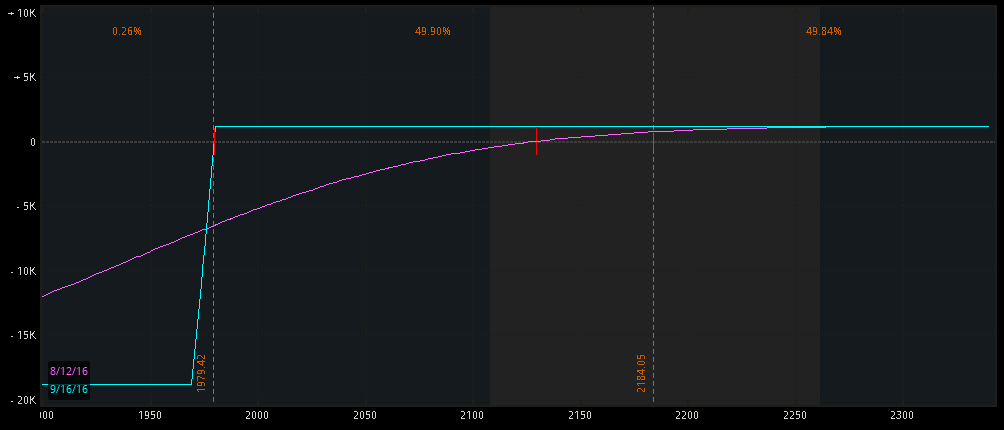

Combining both September income positions, the SPX 1980/1970 CPS with the RUT Lazy Elephant, and Beta-weighting it all against SPX, this is how we're looking:

An overall 82% probability of success and it should all be good as long as SPX doesn't move beyond 2,258 by September expiration. Comfortable T+0 line to the upside, so I am not too concerned on that end of the spectrum. Obviously more risk to the downside, which would be slightly mitigated by the Portfolio Insurance Space Trip positions visualized earlier. The Max combined risk of $27,600 is just theoretical, I would never let the market hit me down there without doing something first with plenty of time to react.

An overall 82% probability of success and it should all be good as long as SPX doesn't move beyond 2,258 by September expiration. Comfortable T+0 line to the upside, so I am not too concerned on that end of the spectrum. Obviously more risk to the downside, which would be slightly mitigated by the Portfolio Insurance Space Trip positions visualized earlier. The Max combined risk of $27,600 is just theoretical, I would never let the market hit me down there without doing something first with plenty of time to react.

Combined Theta of $43.18 and Open profits of $989. A +2% portfolio return in the September cycle is looking more and more likely. Only time will tell. At least the positions feel really comfortable as of this writing.

SEP SPX 1825/1800 Debit Put Spread + 1625/1600 Credit Put Spread

Portfolio Insurance

OCT SPX 1825/1800 Debit Put Spread + 1625/1600 Credit Put Spread

Portfolio Insurance

Combining both the September Space Trip trade and the October Space Trip, this is how the portfolio protection looks at the moment.

(Click on image to enlarge)

September SPX 1970/1980 Credit Put Spread

$1,200 credit. Just 5 deltas and 5 weeks to expiration. No concerns.

$750 of open profits but I still want to milk it a little bit more. Here's the risk profile picture:

September RUT/IWM 1090/1100/113/1280/1290 Lazy Elephant

An overall 82% probability of success, feeling comfortable at the moment.

(Click on image to enlarge)

Time decay $23.34 dollars per day, a number that will keep improving.

5 deltas on the Put side, 12 deltas on the Call side. Not too bad.

Combining both September income positions, the SPX 1980/1970 CPS with the RUT Lazy Elephant, and Beta-weighting it all against SPX, this is how we're looking:

Combined Theta of $43.18 and Open profits of $989. A +2% portfolio return in the September cycle is looking more and more likely. Only time will tell. At least the positions feel really comfortable as of this writing.

Action Plan for the Week

- Nothing to do, unless we reach an extreme. If we reach SPX 2,210 or so, we may be overbought. In that case I would initiate SPX 2260/2270 Credit Call spread (September options). If we reach SPX 2,120 or so, we may be reaching a short-term oversold extreme. At that point I would sell a Credit Put spread in whichever of the two indexes looks more oversold. Other than that, no need to be over involved with the markets this week.

Economic Calendar

Tuesday: Housing Starts, Building Permits, CPI

Wednesday: Crude Oil Inventories, FOMC Minutes

Thursday: Europe CPI. US Philly Fed Index

Options Trading results: Up +2.94% YTD vs S&P up +6.85%. Portfolio 37% invested, 63% cash.

Forex Trading results: Down 4.16% for the year. No Position at the moment.

Take it easy, but take it anyways!

LT

If you are interested in a responsible and sustainable way of trading options for consistent income with solid risk management, consider acquiring LTOptions, my options trading system to the last detail.

Check out 2016 Track Record

Thursday: Europe CPI. US Philly Fed Index

Options Trading results: Up +2.94% YTD vs S&P up +6.85%. Portfolio 37% invested, 63% cash.

Forex Trading results: Down 4.16% for the year. No Position at the moment.

Take it easy, but take it anyways!

LT

If you are interested in a responsible and sustainable way of trading options for consistent income with solid risk management, consider acquiring LTOptions, my options trading system to the last detail.

Check out 2016 Track Record

Go to the bottom of this page in order to see the Legal Stuff

No comments:

Post a Comment