Tough year folks. Tough year for premium sellers so far. Last year at this point we were printing dead presidents left and right, swimming in a pool of easy money that led me to an almost +20% growth by August expiration. In contrast, all we've seen this year is extreme directionality with little sideways action. At some point, at some point, the market will stop going up indefinitely. It always does. And seasonally speaking, little by little we start to enter the weak part of the year. I am still confident there is enough time to pull off positive returns in 2016. We've fought the good fight, the inevitable bad period that every single strategy has to suffer from time to time, and we've fought it well.

Market Conditions

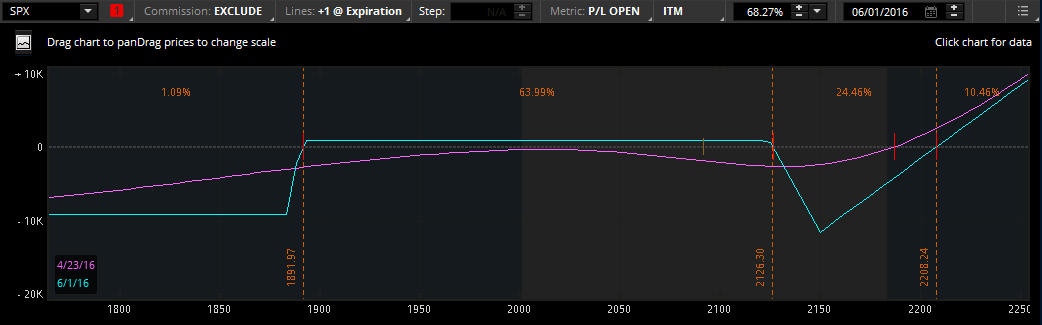

(Click on image to enlarge)

Stochastics: 72 (neutral)

Stochastics: 72 (neutral)

McClellan: +79 (neutral)

Stocks above their 20 DMA: 73% (overbought)

No man's land. The yellow lines as usual, representing the different levels and points in time where I don't want the market to be. You can see I have a lot of capital exposure at the moment. Certainly more than I would like.

Observation

I have to admit that going so far out in time doesn't totally match my personality. It is ok in that, the delta/gamma exposure is smaller, and it takes more sustained moves for the market to hurt you. The downside is, we enjoy a smaller Theta in our favor, we know that. There's always some kind of compromise. For the record, had I played everything this year using 2-month-to-expiration positions, I would have digested the same losses. So, it's not like playing closer to expiration would have served me better during this difficult period or anything. My incompatibility lies in the fact that with sustained market moves in one direction, I may need to hold positions for longer until they become profitable, and this leads to an over-concentration of risk as the new cycles come and I open new positions in order to follow my trading system. As is the case right now for example, where I have 4 Credit Call spreads on, which had absolutely never been the case before for me. This "uneasiness" is what makes this marriage not work very well.

As many of you know, tastytrade advocates the 45 days to expiration approach combined with taking winners at 50% of max-profit. Many people have emailed me asking me why I don't follow this approach. The guys at TT have their studies to back it up. However, they also advocate not adjusting credit spread positions but just letting probabilities play out, combined with trading very small positions. This smallness and the impact of commissions hurt your profitability. Also their own studies, such as this one (minute 14:30), have shown that cutting losers early is a superior approach (by far) even though you experience more losing trades.

I trade slightly differently: No naked positions and defense by adjusting the threatened side (which by the way another study from 2011 or 2012 when Al Sherbin was still in charge, proved to be a superior approach in terms of reducing draw-downs. I think that video is not available anymore but if anyone finds it, feel free to share in the comments section. It was a 4-part series exploring adjustments to the untested side vs the tested side vs letting probabilities play out. Yet somehow, they have buried this knowledge and their studies focus on their particular trading management style, and therefore not very applicable to me.

In my case, finding the sweet spot for my approach, the one that both matches my temperament as a trader and offers a long-term edge, will only be truly possible to mathematically demonstrate once I implement the Options-backtester with all sorts of adjustment options and inclusion of the impact of commissions.

Back to my original point about trading 4 months out in time....this week I also experienced something very annoying: 25 strike price intervals were unavailable, it was only 2200, 2250 and 2300, so no 2225 and no 2275. This definitely hurts maneuverability in your positions and also if we don't trade, we are not "always" following a system, but just "sometimes", depending on the willingness of market makers or God knows who. I didn't enjoy that one bit. So, little by little, I will start mixing up my traditional 8-week-to-expiration approach, looking to avoid the concentration of risk beyond my personal comfort and also looking to avoid situations like the one faced this week with the complete absence of certain strike prices when I needed them.

Action Plan for the Week

- If SPX rallies beyond 2,115, close all the May31 SPX options for a loss and deploy a May31 Credit Call spread above 2,200. At the same time, we would be closing the SPX 2150 Long Calls & 1885/1890 Credit Put spread to mitigate those losses.

- Sell June RUT Credit Put spreads if we reach an oversold extreme condition, a 4% or so from current levels.

- Cash gains on long SPY July Puts on an 80%-100% ROI shall the markets fall significantly.

- If SPX plummets down to 1,910 in just a week, I will close all May31 SPX Positions for an overall small loss. In that case I would be simultaneously cashing gains from June Credit Call spreads, July Credit Call spreads and July SPY Long Puts. After closing all this, I would also deploy a new SPX Credit Put spread in the 1600's. I think this scenario of SPX reaching 1,910 is unlikely for this upcoming week.

Economic Calendar

Monday: New Home Sales

Tuesday: Durable and Core Durable Goods Orders, Services PMI, CB Consumer Confidence

Wednesday: Pending Home Sales, Crude Oil Inventories, FOMC

Thursday: GDP

Friday: Europe GDP, CPI, US Personal Spending, Chicago Consumer Sentiment

Options Trading results - With closed positions and trading costs included, we are down 2.64% for 2016. The S&P is up 2.33%. The portfolio is currently 67% invested, 33% in cash. We have accumulated some good credit to overcome the losses and more, and I feel comfortable holding the current positions. No alarming threat at the moment.

Forex Trading results - Up +1.33% for the year. Four closed trades in total so far: 1 win, 1 loss in EURUSD and 1 win, 1 loss in XAUUSD. No position at the moment.

Good luck this week my friends!

LT

If you are interested in a responsible and sustainable way of trading options for consistent income with solid risk management, consider acquiring LTOptions, my options trading system to the last detail.

Check out 2016 Track Record

Recent Trading Activity

- Adjusted June30 SPX 2150/2175 Credit Call spread on Tuesday taking a $2,240 loss. Deployed a new June30 SPX 2200/2225 spread for a total new credit of $2,080. All the details here.

- Initiated an August SPX 1750/1760/2250/2260 Unbalanced Iron Condor on Thursday for a total credit of $2,560.

- Adjusted June30 SPX 2150/2175 Credit Call spread on Tuesday taking a $2,240 loss. Deployed a new June30 SPX 2200/2225 spread for a total new credit of $2,080. All the details here.

- Initiated an August SPX 1750/1760/2250/2260 Unbalanced Iron Condor on Thursday for a total credit of $2,560.

Market Conditions

(Click on image to enlarge)

McClellan: +79 (neutral)

Stocks above their 20 DMA: 73% (overbought)

No man's land. The yellow lines as usual, representing the different levels and points in time where I don't want the market to be. You can see I have a lot of capital exposure at the moment. Certainly more than I would like.

Observation

I have to admit that going so far out in time doesn't totally match my personality. It is ok in that, the delta/gamma exposure is smaller, and it takes more sustained moves for the market to hurt you. The downside is, we enjoy a smaller Theta in our favor, we know that. There's always some kind of compromise. For the record, had I played everything this year using 2-month-to-expiration positions, I would have digested the same losses. So, it's not like playing closer to expiration would have served me better during this difficult period or anything. My incompatibility lies in the fact that with sustained market moves in one direction, I may need to hold positions for longer until they become profitable, and this leads to an over-concentration of risk as the new cycles come and I open new positions in order to follow my trading system. As is the case right now for example, where I have 4 Credit Call spreads on, which had absolutely never been the case before for me. This "uneasiness" is what makes this marriage not work very well.

As many of you know, tastytrade advocates the 45 days to expiration approach combined with taking winners at 50% of max-profit. Many people have emailed me asking me why I don't follow this approach. The guys at TT have their studies to back it up. However, they also advocate not adjusting credit spread positions but just letting probabilities play out, combined with trading very small positions. This smallness and the impact of commissions hurt your profitability. Also their own studies, such as this one (minute 14:30), have shown that cutting losers early is a superior approach (by far) even though you experience more losing trades.

I trade slightly differently: No naked positions and defense by adjusting the threatened side (which by the way another study from 2011 or 2012 when Al Sherbin was still in charge, proved to be a superior approach in terms of reducing draw-downs. I think that video is not available anymore but if anyone finds it, feel free to share in the comments section. It was a 4-part series exploring adjustments to the untested side vs the tested side vs letting probabilities play out. Yet somehow, they have buried this knowledge and their studies focus on their particular trading management style, and therefore not very applicable to me.

In my case, finding the sweet spot for my approach, the one that both matches my temperament as a trader and offers a long-term edge, will only be truly possible to mathematically demonstrate once I implement the Options-backtester with all sorts of adjustment options and inclusion of the impact of commissions.

Back to my original point about trading 4 months out in time....this week I also experienced something very annoying: 25 strike price intervals were unavailable, it was only 2200, 2250 and 2300, so no 2225 and no 2275. This definitely hurts maneuverability in your positions and also if we don't trade, we are not "always" following a system, but just "sometimes", depending on the willingness of market makers or God knows who. I didn't enjoy that one bit. So, little by little, I will start mixing up my traditional 8-week-to-expiration approach, looking to avoid the concentration of risk beyond my personal comfort and also looking to avoid situations like the one faced this week with the complete absence of certain strike prices when I needed them.

Current Portfolio

May31 SPX 2125/2150 Credit Call Spread

+

SPX 2150 Long Calls & 1885/1890 Credit Put spread

Same plan, I can afford to wait until SPX 2115 or even SPX 2120 without having to absorb a much larger loss. This position will stay in the portfolio until about

the first week of May, where I project to close it all for break-even.

Same plan, I can afford to wait until SPX 2115 or even SPX 2120 without having to absorb a much larger loss. This position will stay in the portfolio until about

the first week of May, where I project to close it all for break-even.

June30 SPX 2200/2225 Credit Call Spread

The adjustment made on Tuesday. Obviously comfortable to ride at the moment.

July29 SPX 1650/1675/2200/2225 Unbalanced Iron Condor

No concern. Still looking decently healthy.

July SPY Long 169 Puts

Portfolio Insurance.

August SPX 1750/1760/2250/2260 Unbalanced Iron Condor

New position with lots of baby-sitting ahead. Nothing new to add.

May31 SPX 2125/2150 Credit Call Spread

+

SPX 2150 Long Calls & 1885/1890 Credit Put spread

June30 SPX 2200/2225 Credit Call Spread

The adjustment made on Tuesday. Obviously comfortable to ride at the moment.

July29 SPX 1650/1675/2200/2225 Unbalanced Iron Condor

No concern. Still looking decently healthy.

July SPY Long 169 Puts

Portfolio Insurance.

August SPX 1750/1760/2250/2260 Unbalanced Iron Condor

New position with lots of baby-sitting ahead. Nothing new to add.

Action Plan for the Week

- If SPX rallies beyond 2,115, close all the May31 SPX options for a loss and deploy a May31 Credit Call spread above 2,200. At the same time, we would be closing the SPX 2150 Long Calls & 1885/1890 Credit Put spread to mitigate those losses.

- Sell June RUT Credit Put spreads if we reach an oversold extreme condition, a 4% or so from current levels.

- Cash gains on long SPY July Puts on an 80%-100% ROI shall the markets fall significantly.

- If SPX plummets down to 1,910 in just a week, I will close all May31 SPX Positions for an overall small loss. In that case I would be simultaneously cashing gains from June Credit Call spreads, July Credit Call spreads and July SPY Long Puts. After closing all this, I would also deploy a new SPX Credit Put spread in the 1600's. I think this scenario of SPX reaching 1,910 is unlikely for this upcoming week.

Economic Calendar

Monday: New Home Sales

Tuesday: Durable and Core Durable Goods Orders, Services PMI, CB Consumer Confidence

Wednesday: Pending Home Sales, Crude Oil Inventories, FOMC

Thursday: GDP

Friday: Europe GDP, CPI, US Personal Spending, Chicago Consumer Sentiment

Options Trading results - With closed positions and trading costs included, we are down 2.64% for 2016. The S&P is up 2.33%. The portfolio is currently 67% invested, 33% in cash. We have accumulated some good credit to overcome the losses and more, and I feel comfortable holding the current positions. No alarming threat at the moment.

Forex Trading results - Up +1.33% for the year. Four closed trades in total so far: 1 win, 1 loss in EURUSD and 1 win, 1 loss in XAUUSD. No position at the moment.

Good luck this week my friends!

LT

If you are interested in a responsible and sustainable way of trading options for consistent income with solid risk management, consider acquiring LTOptions, my options trading system to the last detail.

Check out 2016 Track Record

Go to the bottom of this page in order to see the Legal Stuff

No comments:

Post a Comment