A definitely weak market that went from 2126.85 down to 2079.65 is what we got (-2.27%). Year to date the market is now only up +1.01% and looks sick to everybody you talk to. But, this is not a democracy. The markets, if anything are similar to a dictatorship or a totalitarian system. One of the places where the opinion of the majority is useless, and many times just flat out wrong.

I was pretty active during the week first opening the RUT 1120/1130/1330/1340 unbalanced Iron Condor with September options then closing the August SPX 1815/1825 Credit Put spread early to lock in some profits and get ready for possibly opening another Credit Put spread in the near future.

Market Conditions

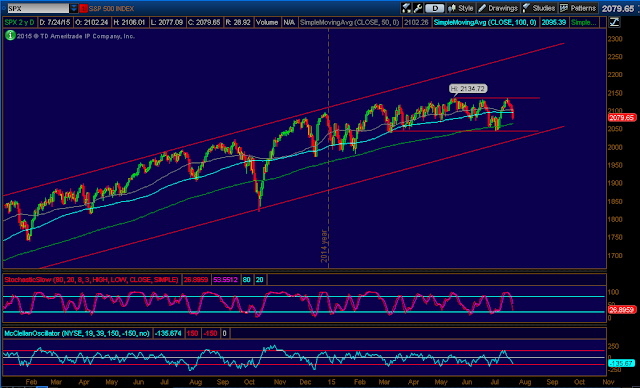

(Click on image to enlarge)

Stochastics: 27 (neutral)

Stochastics: 27 (neutral)

McClellan: -135 (neutral)

Number of Stocks above their 20 Day Moving Average: 29% (oversold)

We have 2 neutral readings and an oversold one. Overall this is no man's land to me but obviously close to a short term extreme pessimism. Notice that I always say "short term". When a market reaches an extreme, I only care about rebounds or pull backs in the next few weeks. The market can reach an extreme oversold reading and it doesn't mean that it won't go down 20% in the next two years. It just means, to me, that a move in the opposite direction (or sideways) is due in the short term, which frankly is all I care about when trading options one or two months out. Anyways, no man's land but getting close to a short term oversold extreme. Horizontal support on the SPX is in the 2040 area, or almost 2% below current levels. That would be a good level for out of the money Puts selling which I'll discuss later on.

August RUT 1150/1160/1350/1360 unbalanced Iron Condor

82% probability of success with 4 weeks to expiration. Looking decent but it may need some attention. The Call side is a winner. The Put side may need adjustments if RUT falls to around 1205 this week. RUT is priced at almost 1226, therefore 1205 is a real possibility.

September RUT 1120/1130/1330/1340 unbalanced Iron Condor

8 weeks to expiration and 75% probability of success. The Call side is comfortable. The Put side may need adjustment if RUT hits 1195 or so.

Action Plan for the week

It is no fun to have two positions with similar risk profiles. They have different probabilities, different strike prices, different expiration months which moves the probabilities numbers and adjustment points differently, one burning that theta faster,...but, it is two correlated positions nonetheless affected by the same market movement. I also have Calls in those positions working in my favor. So, it is not terrible, but I won't deny that it is not comfortable either.

If RUT falls to around 1205 (this is just an approximation, the real trigger is the Aug 1160 Put reaching 30% probability of in the money) then I will adjust the Aug 1150/1160 Credit Put spread down to the 1100 area. There will be a temporary loss there, but provided the adjustment wins it will still be a positive August when all is said and done.

If RUT falls harder than that, to around 1195 I may need to adjust the September 1120/1130 Credit Put spread side of the Iron Condor that I opened this past week. In this case, the adjustment would be made towards the September 1050 area, where I think chances are very good for a win.

I obviously don't want to see RUT falling, but if it does, risk will be managed as usual and losses will be controlled. It is always easier to defend the Put side as volatility expands and the adjustments can be placed so much further down with decent credits. The real pain happens during true market crashes where the market just keeps falling precipitously in a short period of time.

If SPX moves down to the 2040 horizontal support area the market will probably be in extreme pessimism mode. At that point selling the August SPX 1900/1895 Credit Put spread for 0.30 credit or better would be an attractive play where I would put my money. Alternatively you can use September options and then go even lower into the 1800 zone. I would personally still go with August options.

Finally, if we stay sideways or move up, I will stay put. If RUT moves up decently, I may close the RUT August Iron Condor for 80% of its max profit if that number is ever reached.

Forex

The Euro had a strong week and the Sniper ended up with a losing trade. I had an issue with my MetaTrader station where I had to uninstall/reinstall. When it was all fixed, I logged into the New York server (GMT-5) instead of the recommended GMT+2 server. I didn't realize it until yesterday. Due to this, my daily bars were different and the rules to exit just materialized. But for those playing on a GMT+2 server, the trade should still be open. The performance of the Sniper is now +11.72% year to date and there should be two more trades left in the year. So far there have been 4 trades, the first two were winners, the last two have been losers but the winners have been much bigger in comparison.

Economic Calendar

Monday: Core Durable Goods Orders

Tuesday: CB Consumer Confidence

Wednesday: US Pending Home Sales and FOMC Statement.

Thursday: US GDP

Friday: China's Manufacturing PMI

Good luck this week folks!

Check out 2015 Track record

I was pretty active during the week first opening the RUT 1120/1130/1330/1340 unbalanced Iron Condor with September options then closing the August SPX 1815/1825 Credit Put spread early to lock in some profits and get ready for possibly opening another Credit Put spread in the near future.

Market Conditions

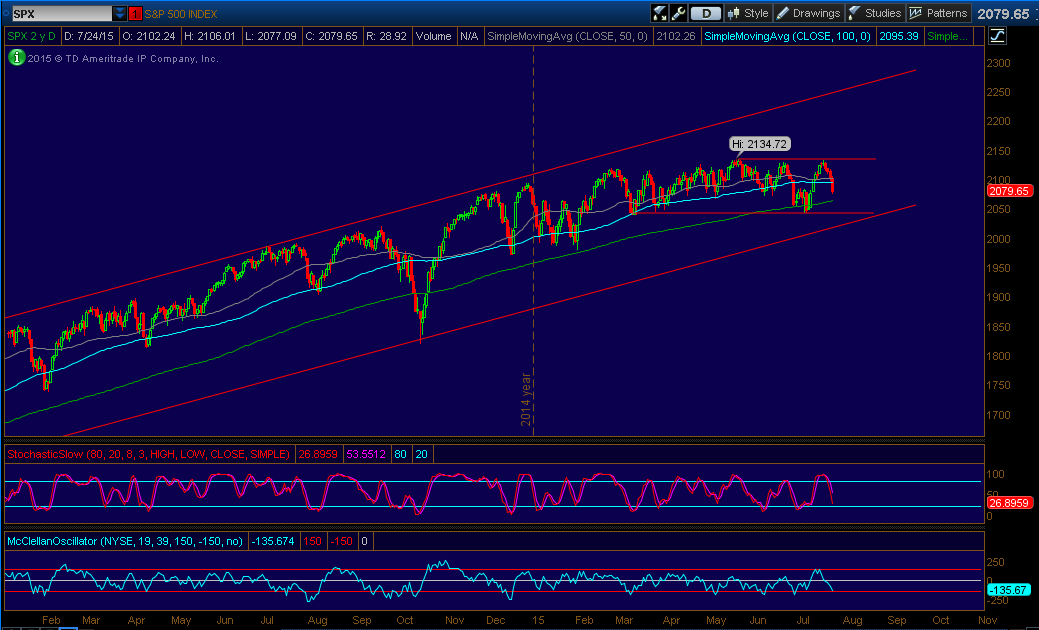

(Click on image to enlarge)

McClellan: -135 (neutral)

Number of Stocks above their 20 Day Moving Average: 29% (oversold)

We have 2 neutral readings and an oversold one. Overall this is no man's land to me but obviously close to a short term extreme pessimism. Notice that I always say "short term". When a market reaches an extreme, I only care about rebounds or pull backs in the next few weeks. The market can reach an extreme oversold reading and it doesn't mean that it won't go down 20% in the next two years. It just means, to me, that a move in the opposite direction (or sideways) is due in the short term, which frankly is all I care about when trading options one or two months out. Anyways, no man's land but getting close to a short term oversold extreme. Horizontal support on the SPX is in the 2040 area, or almost 2% below current levels. That would be a good level for out of the money Puts selling which I'll discuss later on.

August RUT 1150/1160/1350/1360 unbalanced Iron Condor

82% probability of success with 4 weeks to expiration. Looking decent but it may need some attention. The Call side is a winner. The Put side may need adjustments if RUT falls to around 1205 this week. RUT is priced at almost 1226, therefore 1205 is a real possibility.

September RUT 1120/1130/1330/1340 unbalanced Iron Condor

8 weeks to expiration and 75% probability of success. The Call side is comfortable. The Put side may need adjustment if RUT hits 1195 or so.

Action Plan for the week

It is no fun to have two positions with similar risk profiles. They have different probabilities, different strike prices, different expiration months which moves the probabilities numbers and adjustment points differently, one burning that theta faster,...but, it is two correlated positions nonetheless affected by the same market movement. I also have Calls in those positions working in my favor. So, it is not terrible, but I won't deny that it is not comfortable either.

If RUT falls to around 1205 (this is just an approximation, the real trigger is the Aug 1160 Put reaching 30% probability of in the money) then I will adjust the Aug 1150/1160 Credit Put spread down to the 1100 area. There will be a temporary loss there, but provided the adjustment wins it will still be a positive August when all is said and done.

If RUT falls harder than that, to around 1195 I may need to adjust the September 1120/1130 Credit Put spread side of the Iron Condor that I opened this past week. In this case, the adjustment would be made towards the September 1050 area, where I think chances are very good for a win.

I obviously don't want to see RUT falling, but if it does, risk will be managed as usual and losses will be controlled. It is always easier to defend the Put side as volatility expands and the adjustments can be placed so much further down with decent credits. The real pain happens during true market crashes where the market just keeps falling precipitously in a short period of time.

If SPX moves down to the 2040 horizontal support area the market will probably be in extreme pessimism mode. At that point selling the August SPX 1900/1895 Credit Put spread for 0.30 credit or better would be an attractive play where I would put my money. Alternatively you can use September options and then go even lower into the 1800 zone. I would personally still go with August options.

Finally, if we stay sideways or move up, I will stay put. If RUT moves up decently, I may close the RUT August Iron Condor for 80% of its max profit if that number is ever reached.

Forex

The Euro had a strong week and the Sniper ended up with a losing trade. I had an issue with my MetaTrader station where I had to uninstall/reinstall. When it was all fixed, I logged into the New York server (GMT-5) instead of the recommended GMT+2 server. I didn't realize it until yesterday. Due to this, my daily bars were different and the rules to exit just materialized. But for those playing on a GMT+2 server, the trade should still be open. The performance of the Sniper is now +11.72% year to date and there should be two more trades left in the year. So far there have been 4 trades, the first two were winners, the last two have been losers but the winners have been much bigger in comparison.

Economic Calendar

Monday: Core Durable Goods Orders

Tuesday: CB Consumer Confidence

Wednesday: US Pending Home Sales and FOMC Statement.

Thursday: US GDP

Friday: China's Manufacturing PMI

Good luck this week folks!

Check out 2015 Track record

Go to the bottom of this page in order to see the Legal Stuff

It was pretty smart of you for closing the August SPX credit put spread early. I also agree with you that we are fast approaching oversold conditions. We might get it next week. I am ready to sell some more credit put spreads even though already have a bunch.

ReplyDeleteI did not make any trades last week. Here are the current positions:

RUT September 30th 1000/990 & 1380/1390 iron condor - currently profitable; will close in the next couple of weeks

RUT September 30th 1050/1040 cps - currently profitable; will close in the next couple of weeks

SPX September 30th 1725/1700 cps - currently profitable; will close in the next couple of weeks

SPX September 30th 1800/1790 cps - currently profitable; will close in the next couple of weeks

SPX October 30th 1750/1725 & 2275/2300 iron condor - currently profitable

SPX November 30th 1750/1725 & 2275/2300 iron condor - cps position shows a tiny loss

Last Week:

ReplyDeleteOn Monday, I opened a new position in RUT with September expiration. I sold slighly unbalanced iron condor spreads: 6x RUT Sep 1120/1140 cps for 1.32 and 5x RUT Sep 1340/1360 ccs for 1.23. I received total credit $1407 (margin is $10593).

On Monday, I closed the entire August RUT iron condor spreads (including the hedging debit put spread), because it reached my profit target (3/4 of maximum profit at expiration $678). These closing transactions cost me $238. So the total profit on this position was $440 (or 4.6% on margin of $9510).

On Friday, I partially closed the August SPX iron condor spreads that were near my profit target. I managed to close all credit call spreads, the hedging debit credit spread and 2 out of 5 credit put spreads for $90 debit. I was not able to close all credit put spreads so I am currenly biding the remaining 3 SPX Aug 1830/1850 cps at 0.10.

Open Positions:

3x SPX Aug 1830/1850 cps

6x SPX Sep 1850/1870 cps + 5x SPX Sep 2210/2230 ccs

6x RUT Sep 1120/1140 cps + 5x RUT Sep 1340/1360 ccs

Next Week:

I have two relatively new credit spreads in September expiration. I am not planning to open new positions unless the market makes a significant move up or down. I will just monitor the open positions.

August SPX credit put spreads: I would adjust them when SPX falls below 1980.

September SPX iron condor spreads: I would adjust them with a debit spred when SPX is below 2000 or above 2140. This position is reasonable safe at the moment.

September RUT iron condor spreads: There is some room to the upside up to 1290. However, the downside adjustment point of 1220 is not very far from RUT Friday close 1226. When RUT hits 1220, the delta of my short RUT Sep 1140 puts will be around 20 and the overall position will show open loss of -4%. I planning to cut the position delta by buying either 1x RUT Sep 1140/1170 dps at projected price 5.80 or by buying 2x RUT Sep 1140/1160 dps at projected price 6.90.

Good trading,

Martin

Hi Martin,

DeleteRUT fell below your adjustment point today. I know you are planning to buy 1x RUT Sept 1140/1170 dps. Have you consider buying August instead to lower the cost?

Hello Jonathan,

DeleteAs you correctly guessed, on Monday morning, when RUT opened with a gap below 1220, I bought one protective RUT Sep 1140/1170 dps for 6.51.

There are two reasons why I prefer to have debit spreads in the same expiration month as the credit spreads (even though debit spreads in the front month are cheaper):

(1) I want my credit speads to be hedged until their expiration. If I bought August debit spread and RUT tanks at the end of August or at the beginning of September, I would have to buy another debit spread.

(2) August debit spreads have higher theta compared to September debits spreads. Consequently, August debit spreads lose money and hedging effect faster than September debit spreads.

But I agree that it would make sense to buy a near term debit spread (August) if you want a short term hedge and you think that the market will reverse in a couple of days.

Thanks for your comments.

Martin

Hello chaps

ReplyDeleteI did not manage to get fill either this week. I was looking to trade September CCS both SPX and RUT. But will change strategy and try to get CPS due to the oversold condition.

My current positions are:

RUT Sep15 CPS 1040/50 @ 0.6

RUT Aug15 CCS 1360/70 @ 0.52

SPX Aug CPS 1815/25 @ 0.45

The 3 positios look preatty secure, lets see how this week markets behave.

Happy Trading

Your positions do look solid. I like your discipline in waiting for an oversold condition before selling only credit put spreads.

DeleteIs it true that credit put spread more profitable based on IV than credit call? Because price usually decrease when price gets higher

ReplyDeleteThe short answer is yes. The credit put spreads you sell during a high VIX environment will lose value quickly when the market bounces back and VIX shrinks. I have seen this occur over and over again to come to the conclusion that the best time to sell is when the market is falling very hard.

Delete